Update 15 December 2023 – The European Parliament and the European Council reached a provisional agreement on the corporate sustainable due diligence directive (CSDDD). Read more in our latest article the key points following from the latest information as presented by the two European co-legislators.

Legislative process of the CSDDD

In our earlier ESG key legal considerations, we discussed the initial proposal for the CSDDD of the European Commission (23 February 2022) and the position of the Council of the European Union on the proposed CSDDD (1 December 2022).

The CSDDD aims to foster sustainable and responsible corporate behaviour. Briefly put, the CSDDD would require large companies to undertake due diligence on their own activities and that of their suppliers, and to identify and prevent, end or mitigate any actual or potential adverse impacts of their activities on human rights and on the environment. For more information on the CSDDD, we refer to the contribution in the Dutch legal journal on corporate law (Tijdschrift Ondernemingsrecht) of our colleagues Kitty Lieverse and Menno Baks.

On 25 April 2023, the European Parliament’s committee on legal affairs (better known as JURI) adopted a draft report (JURI Report) entailing a suite of amendments to the CSDDD as proposed by the Commission. In our latest contribution, we discussed this JURI Report, hinting that it could give an indication on the position of the European Parliament. On 1 June 2023, the European Parliament has adopted its position.

As of now, interinstitutional negotiations on the CSDDD between the European Parliament, the European Council and the European Commission can commence. Once the CSDDD has been formally adopted – not expected before 2024 – Member States will have two years to implement the CSDDD into national legislation.

For the Netherlands, the CSDDD may catch up with several national ESG regulatory legislative proposals and initiatives, such as the Child Labour Duty of Care Act (which has not entered into force) and the Dutch Responsible and Sustainable International Business Act (which is still a legislative proposal). Similar to the CSDDD, the Dutch Responsible and Sustainable International Business Act provides for an obligation for all in-scope ‘large’ companies including subsidiaries to audit their supply chains and those of business relations for adverse impacts such as human rights, working conditions and the environment.

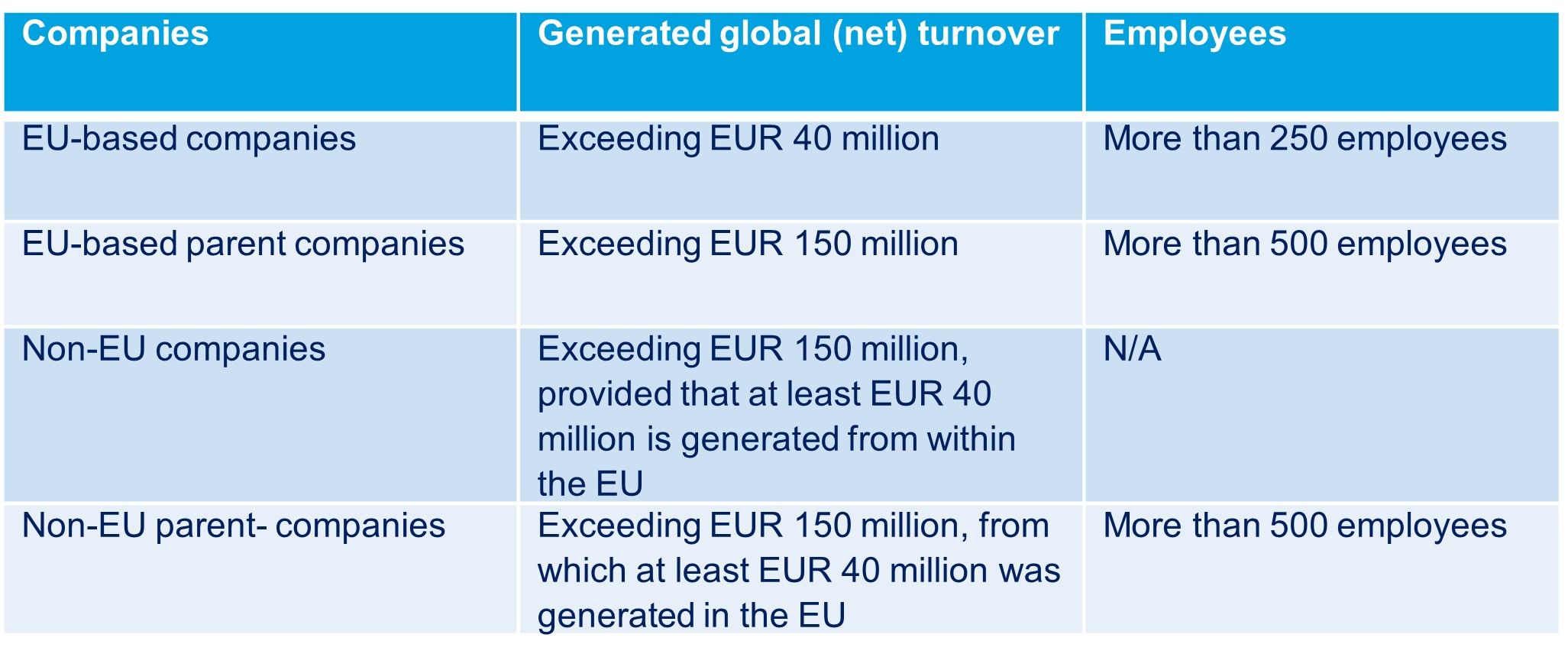

The scope of the CSDDD as prescribed by the European Parliament

One of the key amendments as presented by the European Parliament concerns the threshold criteria to fall within the scope of the CSDDD. The position of the European Parliament is to determine the scope of the CSDDD as follows: Regarding the net threshold turnover generated within the EU by non-EU companies it is relevant to mention that this also includes the turnover as generated by third-party companies with whom the company and/or its subsidiaries has entered into a vertical agreement in the EU in return for royalties.

Regarding the net threshold turnover generated within the EU by non-EU companies it is relevant to mention that this also includes the turnover as generated by third-party companies with whom the company and/or its subsidiaries has entered into a vertical agreement in the EU in return for royalties.

Based on the position of the European Parliament, in-scope companies will have the obligation to basically adopt a transition plan in accordance with Article 19a CSRD, aimed at restricting global warming to 1.5°C in accordance with the Paris climate agreement. Large companies employing more than 1000 employees should have a remuneration policy in place to ensure that the variable remuneration of directors is linked to the achievement of the plan’s objectives.

CSDDD expected negotiation points

Based on the deviating positions of the European Parliament and the Council in respect of the proposal by the European Commission, the following points are likely to be negotiation issues:

- The applicability of the CSDDD to the financial sector (i.e., whether the financial sector should be substantially excluded from the CSDDD);

- the conditions for civil liability under the CSDDD; and

- the introduction of a directors’ duty of care and its consequences.

Potential impact of the CSDDD

The CSDDD includes a system of public law supervision and enforcement (in short: the requirement for Member States to appoint a supervisory authority and grant investigative and enforcement powers to such supervisory authority). In addition, the CSDDD allows for private enforcement. The CSDDD introduces best-effort obligations for companies potentially resulting in civil liability of the company and its subsidiaries in case of infringement of any of these obligations and prescribes that national laws must provide for civil liability exposure for damages caused by breaches of the CSDDD.

Therefore, the CSDDD provides (another) civil law instrument to hold companies accountable and liable for environmental degradation and human rights abuses, both within the European Union and outside. In this regard, we also refer to our earlier trend report on ESG litigation. Following the landmark case against Shell (which is currently pending in appeal) and the introduction of the CSDDD, further class action litigation against companies on responsibility for human rights violations in the supply chain can be expected. Under the newly introduced Dutch class action regime (WAMCA), we already see various cases in which claim organizations are targeting big companies on this topic (please see our earlier blog in this regard).

Further ESG (class action) litigation may also target financial institutions and/or companies’ directors. This trend also seems to have already started: in the Netherlands, Millieudefensie (known for the landmark case against Shell) has recently announced that it considers filing a case against two national banks (ING and Rabobank). In the United Kingdom, ClientEarth initiated a case against Shell’s board of director in UK (as recently dismissed by the UK High Court).

Get in touch

Our firm is closely monitoring the developments concerning the CSDDD, ESG topics and potential liability and (class action) litigation risks in this respect. Please do not hesitate to contact one of our colleagues for more information about ESG litigation in the Netherlands.