Obligations under the CSDDD

Under the CSDDD, in-scope companies (including the financial sector, albeit limited at first) are required to adopt transition plans to ensure that their strategies and business plans are in line with the Paris Agreement. The CSDDD also links remuneration for directors of in-scope companies to these plans and achievements. In case an in-scope company identifies actual and potential adverse impact on human rights or the environment (CSDDD-risks) in its value chain which cannot be prevented or ended, it should end its partnerships with the companies responsible for such adverse impact. The value chain as defined in the CSDDD will cover the upstream business partners of a company and partially its downstream activities (limited to transport, storage and disposal, provided that these activities are outsourced to other companies).

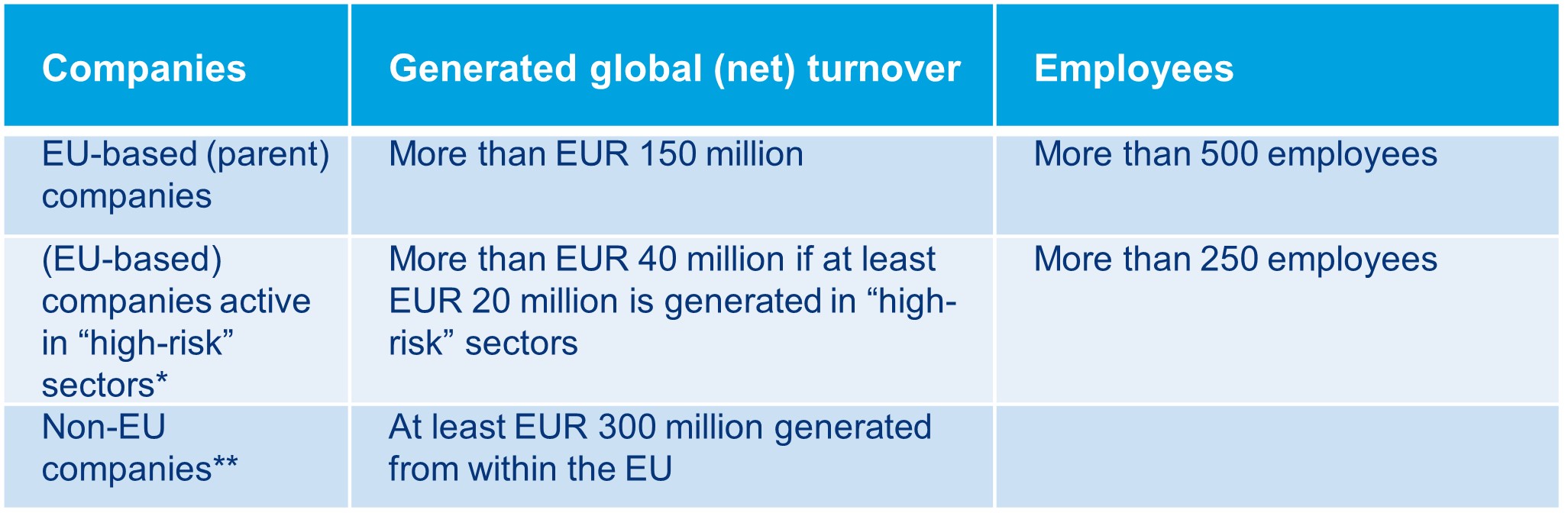

General scope of the CSDDD

The scope of the CSDDD seems to be determined as follows (subject to the text of the final draft of the CSDDD):

* The CSDDD will include the following high risk sectors: manufacture and wholesale trade of textiles, clothing and footwear, agriculture (including forestry and fisheries), manufacture of food and trade of agricultural materials, extraction and wholesale trade of mineral resources or manufacture of related products.

** The CSDDD will only apply to non-EU companies three years from the entry into force. The Commission will have to publish a list of non-EU companies that within the scope of the CSDDD.

Applicability on financial sector

The financial sector seems to be in-scope, albeit for now only to a limited extent. The financial sector will only have to apply the CSDDD in relation to their own operations and upstream supply chains. Firms in the financial sector will also have to adopt a plan ensuring their business model complies with limiting global warming to 1.5°C. There will be a review clause for a possible future expansion of the scope for this sector based on a sufficient impact assessment.

Control mechanism of the CSDDD and the scope of (civil) liability

The CSDDD includes two control systems. First, an administrative supervision and sanctions, including naming and shaming and heavy fines (maximum penalty is at least 5% of (net) turnover). Second, the CSDDD includes strong possibilities for civil enforcement, as in-scope companies will be liable for damages caused by a breach of their obligations under the CSDDD.

The adversely affected parties are given a period of five years to initiate (ESG) claims based on the CSDDD against in-scope companies. The CSDDD also enables trade unions and civil society organizations to file such claims. It appears that the CSDDD will provide similar procedural possibilities as included in the Representative Actions Directive (EU 2020/1828).

Duty of care

The CSDDD contains a risk-based approach. Therefore, in-scope companies only have the obligation to take measures if it is directly responsible for the CSDDD-risks. Otherwise, the responsibility extends to a general duty of care of the in-scope company. The duty of care of directors of in-scope companies seems to be excluded from the CSDDD.

Get in touch

Our firm is closely monitoring the developments concerning the CSDDD, ESG topics and potential liability and (class action) litigation risks in this respect. Please do not hesitate to contact one of our colleagues for more information about ESG litigation in the Netherlands.