Some measures have already been adopted in 2025 and 2026. More structural changes are still under discussion and are expected to take effect mainly from 2027.

In this first contribution on the Belgian pension reforms, we will discuss the new requirements for early retirement and the so-called bonus / malus mechanism.

Impact on the (early) statutory retirement age

The statutory retirement age remains unchanged. It currently equals 66 years, and it will be increased to 67 from 2030. At this age, an employee can retire without having to meet specific career conditions.

For early retirement, an employee however needs to meet specific age and also seniority conditions. The current age and career conditions for early retirement remain as such in place.

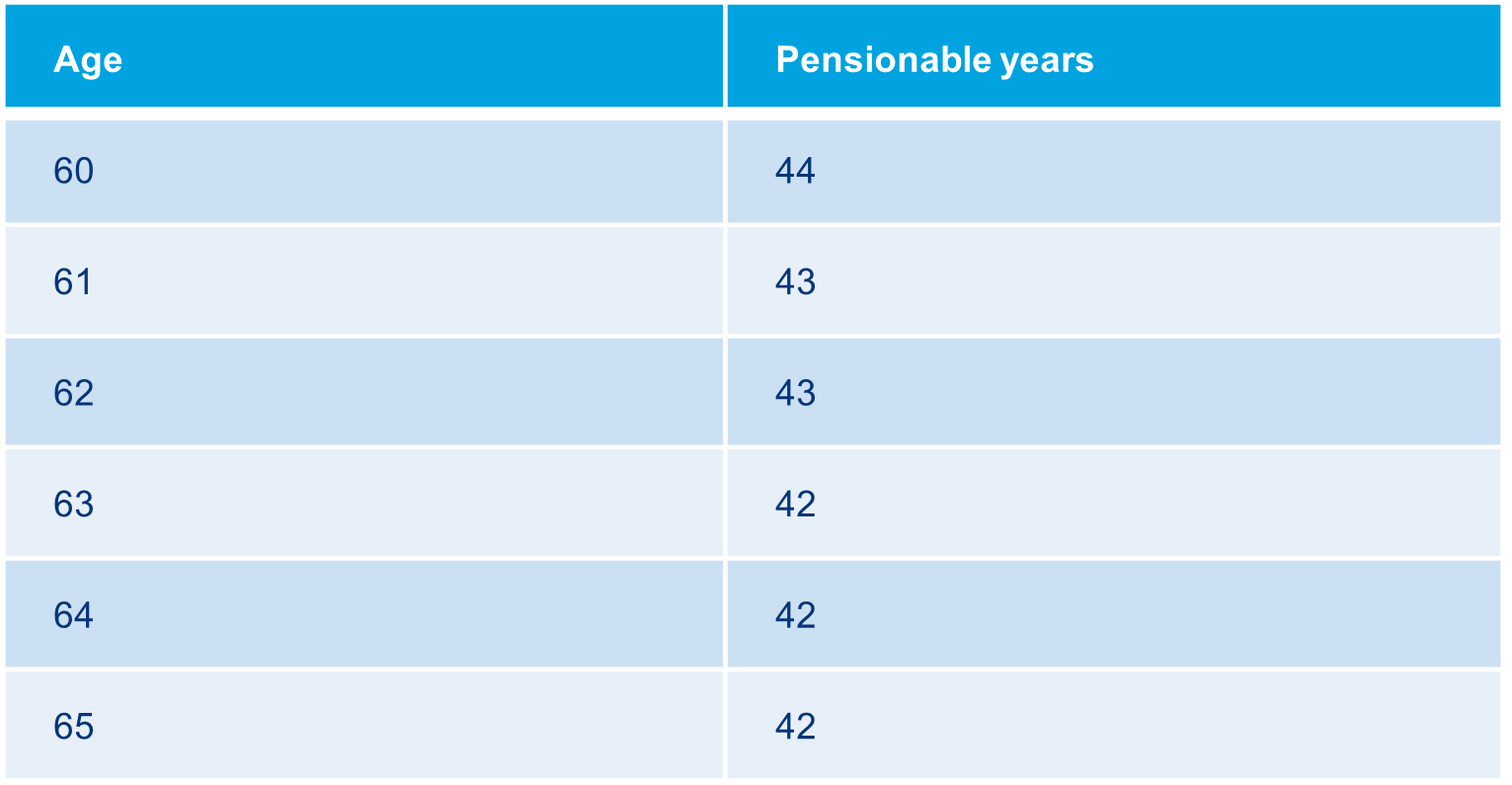

From 2027 early retirement will also be possible from age 60 (and onwards) where the person concerned can demonstrate 42 qualifying career years, each including at least 234 FTE days.

Whereas the career conditions remain unaltered, the required number of working days to qualify as a pensionable year is however increased from 104 FTE to 156 FTE days.

Note that the Belgian social security legislation departs from a six-days work week (312 FTE / calendar year). If an employee however works full time under a five-days working week he will also register 156 working days on 30 June (even though the actual number of working days is lower). If an employee works part-time (50%) he will register a pensionable year by the end of December of the relevant year.

What does this mean in practice?

- If an employee works (or worked) less than 50% during a calendar year, the relevant year will no longer qualify for early retirement.

- If an employee works full time and meets the age condition for early retirement, the current earliest retirement date (1st of May) will be postponed until the 1st of July.

The 156 FTE- requirement is also applied for past service years.

There are however a couple of transition measures:

- The first year of employment still counts in the event of 104 FTE (because many employees started working in September).

- Employees who meet the current conditions for early retirement before 2027 can still retire early.

- The earliest retirement date is extended by maximum 1 year for employees born before 1966 and 2 years for employees born in 1966.

- Each employee benefits from 5 so-called “spare days” to complete service years with a limited number of missing days to reach the 156 FTE threshold. If an employee would for example have two incomplete years of 154 FTE and 153 FTE, these two years will however qualify as pensionable years thanks to the package of 5 days.

Note that specific periods of absence (such as incapacity for work, maternity leave and periods of unemployment) still qualify as pensionable years for the 156 FTE requirement.

The new bonus-malus scheme

The new bonus system

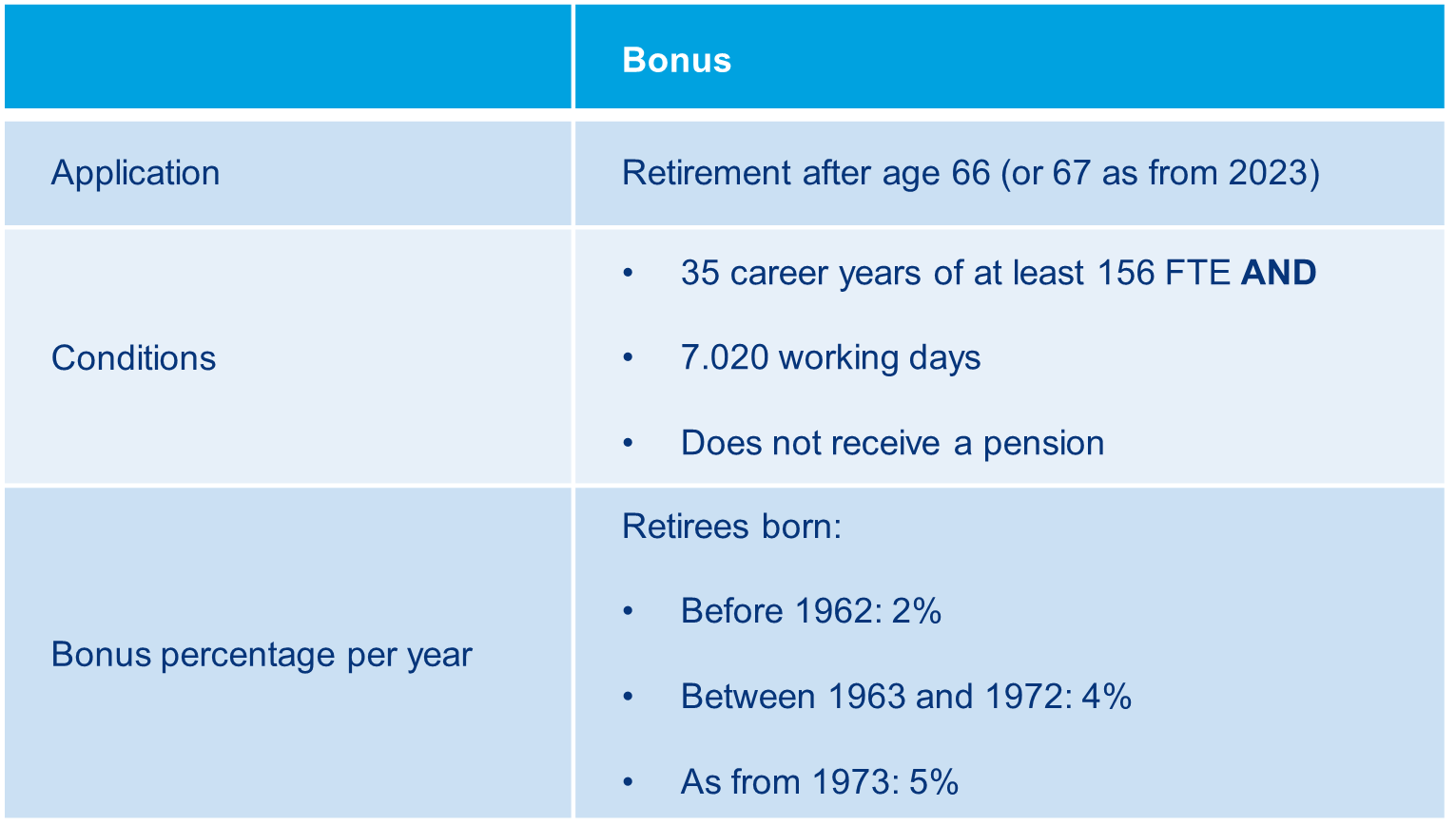

From 2027, a new bonus mechanism will be introduced. In a nutshell: employees who postpone their retirement after the statutory pension age will be entitled to an additional pension up to 5% of the base amount for each year of postponement.

The eligibility conditions for the pension bonus and the amounts can be summarised as follows:

Please note that it is not required for the employee to postpone their retirement by one full year. The bonus is expressed on an annual basis but is prorated for shorter periods of postponement of retirement beyond the statutory retirement age of 66 or 67 years.

Periods of unemployment and incapacity for work are not considered for the bonus requirement. Some other periods such as temporary unemployment and maternity leave are however considered for the career requirements.

The new malus system

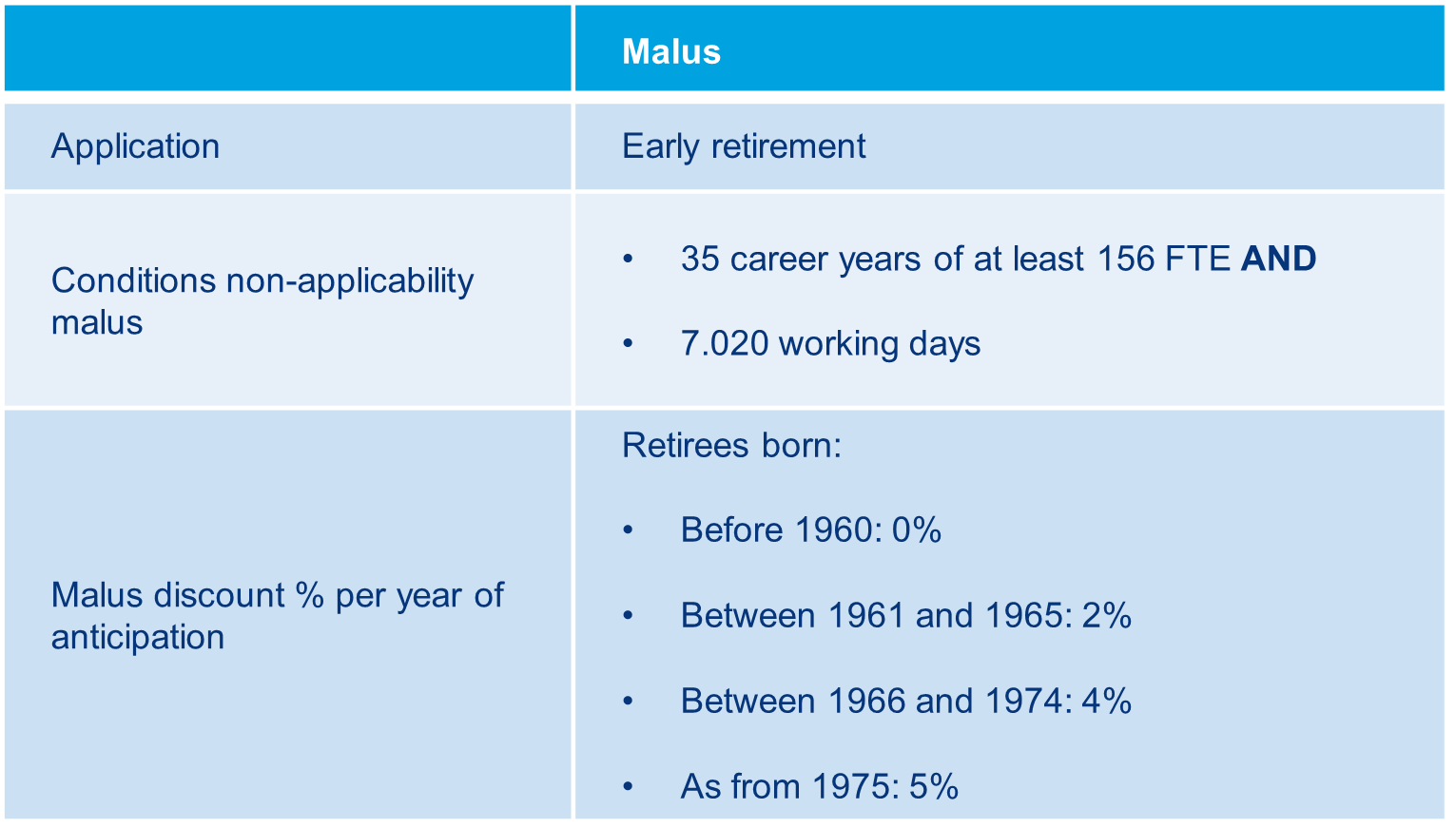

Whereas the bonus rewards working longer beyond the statutory retirement age, the entirely new pension malus is intended to discourage early retirement.

The malus system only applies in the event of early retirement and if the employee has a relatively limited number of career years or overall number of working days. The conditions for the (non-applicability) of the new malus and the pension discount can be summarised as follows:

The penalty therefore does not automatically apply in cases of early retirement. If the employee has worked for at least 35 calendar years on a half-time basis and can also demonstrate a total of 22.5 years FTE employment, the penalty does not apply. As is the case for early retirement, the employee may use five “spare days” if, in one or more years, they have just failed to accrue 156 FTE.

Also here some periods of absence are assimilated. This includes, among other things, periods of incapacity for work, temporary unemployment, and maternity leave. Ordinary periods of unemployment, however, are not considered for the purpose of avoiding the application of the malus.

The impact of the penalty can be quite substantial. For example, if a person whose statutory retirement age is 67 retires early at age 63, that person may depending on the year of birth receive up to 20% less pension. On a gross monthly pension amount of EUR 2,000, this represents a reduction of EUR 400, resulting in a monthly pension of EUR 1,600 only.

What does this mean for HR professionals?

Working part-time at less than 50% will in any event be penalised, as the current statutory minimum employment rate of 30% was sufficient to credit one pensionable year. For employees working full-time who have already reached the required age, the stricter interpretation of the career condition will only result in a postponement of the statutory retirement age by a few months.

It remains to be seen whether the pension bonus or malus will effectively incentivise employees to work longer.

Reaching the early or statutory retirement age does not automatically terminate the employment contract. Vice versa taking up the state pension does not automatically terminate the employment relationship.

Upon reaching the statutory retirement age, however, the employer may terminate the employee’s employment with a shortened notice period.

In the case of early retirement, the commencement of the state pension will generally coincide with the termination of the employment contract, because the state pension can only be combined with salary to a very limited extent. Given that the income that can be combined with a state pension is so low, it generally does not make sense for an actively working employee to opt for early retirement.

Early retirement therefore generally coincides with the termination of the employment contract.

When an employee is or becomes eligible for early retirement (the employer generally depends on information provided by the employee in this respect), a departure by mutual agreement has often been a possible exit scenario.

Until now many employees are happy to retire early without any financial compensation. Until now some other employees tend to raise the tax impact on their occupational pension or the impact on the monthly state pension only. There is a possibility that employees who are eligible for early retirement will now also take into account the effects of a missed pension bonus or the impact of a pension malus in early retirement negotiations.

Although there is no legal obligation to do so and of course depending on the employee’s retirement outlook the employer could consider:

- Using a garden leave arrangement in order to cancel the effects on the bonus / malus;

- Granting a one-off severance payment covering the required period for the application of the bonus / non-application of the malus; or

- Alternatively providing a cash compensation to mitigate the impact of the malus / forfeited bonus.

In order to facilitate an early departure arrangement before age 66 or 67.

In our next contribution we will discuss the impact of the pension reforms on occupational pension schemes.

Contact us

For further information on the impact of the Belgian pension reforms, please contact our Employment Pensions & Benefits team.