Ratio and background of the legislative proposal

In April 2023, the government announced a number of plans to reform the labour market in a letter to the House of Representatives. Part of these plans concerned the intention to amend the regulations regarding the legal assessment of employment relationships. The Proposal is the result of such intention and serves to clarify when work must be performed as an employee and when work can be performed as a self-employed individual. The qualification of the legal relationship between the employer and the ‘worker’ is, amongst other things, an important item on the agenda of the Minister of Social Affairs and Employment, as the Minister is of the opinion that taxes and social security contributions are often (erroneously) not withheld, even though the relevant proclaimed self-employed individuals factually perform the same work as employees who are employed on the basis of an employment agreement. The same applies to the payment of pension contributions. In addition, the Minister believes that the protection of self-employed individuals in the lower segment of the market cannot be guaranteed and that the equal treatment of employees and self-employed individuals is at risk due to the current ambiguity on (self-)employment.

The Proposal fits into a trend of political developments aimed at combatting pseudo self-employment. In that regard, we previously wrote about the fact that the enforcement suspension (handhavingsmoratorium) will lapse on 1 January 2025 and that the model contracts for self-employment approved by the Dutch Tax Authorities will lose their validity on 1 January 2024. In addition, the timing of the Proposal also seems to be linked to the recent Deliveroo judgment of the Supreme Court on 24 March 2023.

The Proposal contains two important changes:

- three new paragraphs will be added to the article 7:610 of the Dutch Civil Code (DCC), clarifying the ‘working in the service of’ condition and introducing an assessment framework in that respect;

- a new article 7:610aa DCC will be introduced, which includes a legal presumption that an employment relationship will be deemed to exist if the remuneration for performing the work does not exceed € 32.24 per hour.

The ‘working in the service of’ condition

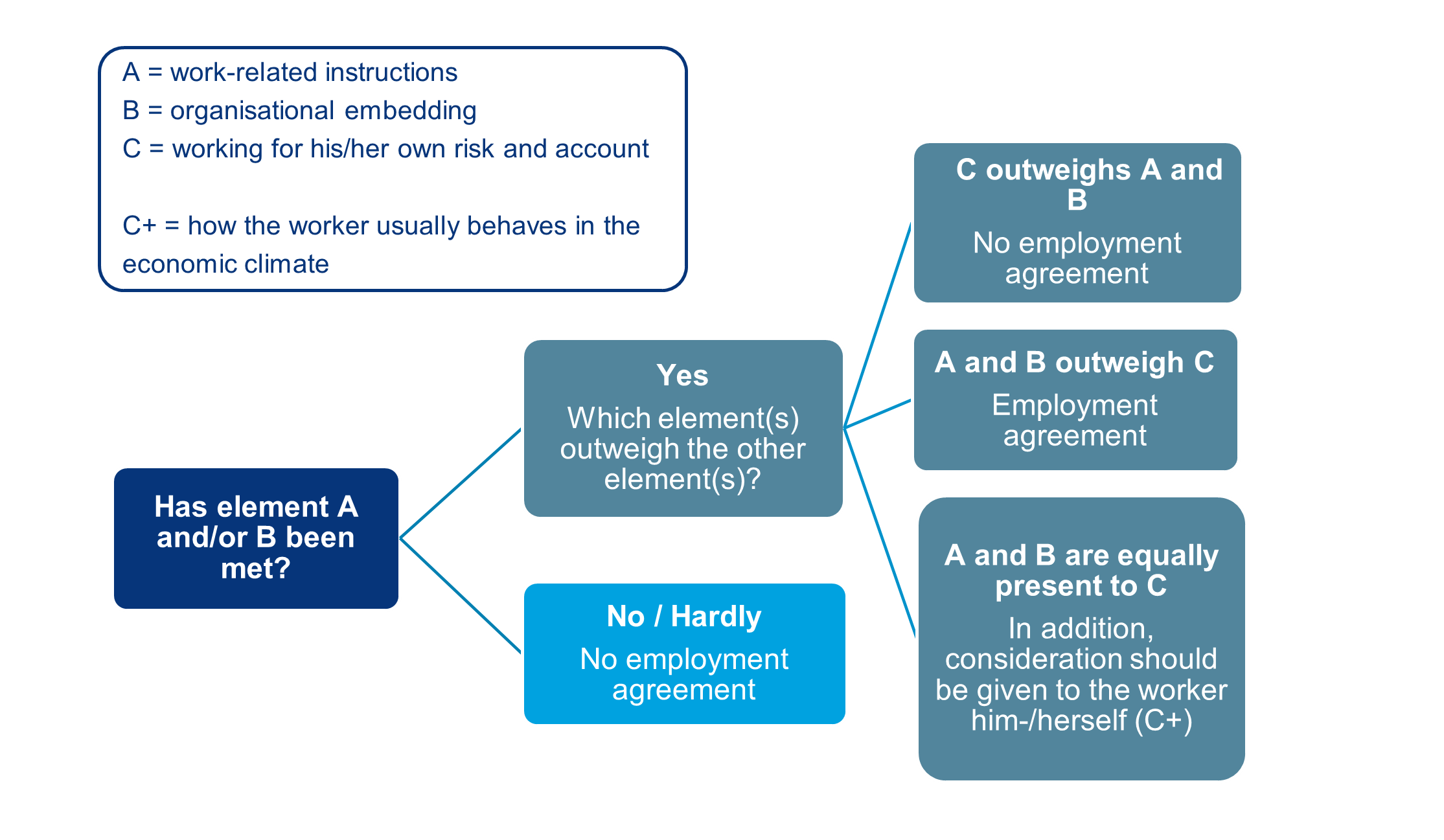

Under the current article 7:610(1) DCC, an employment relationship is deemed to exist if the conditions (i) work, (ii) wage and (iii) authority (‘working in the service of an employer’) are met. The new article 7:610(2) DCC will contain a number of ‘main elements’ on the basis of which it can be determined whether the authority condition ‘working in the service of the employer’ has been fulfilled:

- the work is performed under work-related instructions of the employer; or

- the work or the employee is organisationally embedded in the employer’s organisation; and

- the employee does not perform the work for his own risk and account.

In addition, the new article 7:610(3) DCC sets out the interrelationship between the various elements mentioned above, in the sense that elements (A) and (B) must be collectively measured against element (C). If (A) and (B) are met and, moreover, these elements outweigh (C), the legal relationship is qualified as an employment agreement. The same applies the other way around: if (C) outweighs (A) and (B) combined, the legal relationship is qualified as self-employment. If, however, (A) and (B) are equal to (C), a fourth element may provide a solution. In such case, additional consideration should be given to how the worker usually conducts his/her business (also taking into account his/her other entrepreneurial activities).

The Explanatory Memorandum to the Proposal contains an overview of the (national and EU) case law on the qualification of legal relationships as (self-)employment. On the basis of this assessment framework, the various conditions should be interpreted on the basis of certain indications, which the Minister can later elaborate on in a general administrative order (Algemene Maatregel van Bestuur). In that way, the government wants to ensure a certain future-proofness of the conditions. The indications are presented as follows.

The Explanatory Memorandum includes a schematic representation of the assessment framework (see below). It also discusses a number of practical examples. The starting point is clear: substance prevails over appearance. The examples show that the assessment is made on the basis of all circumstances of the case and that filling in the conditions is not always easy; it is, for example, unclear how many indications have to be present for a condition to be met. The qualification of the legal relationship as (self-)employment therefore remains open to interpretation.

Legal presumption employment relationship

The new article 7:610aa DCC also introduces a civil law (rebuttable) legal presumption to determine whether a legal relationship should be qualified as an employee or a self-employed individual: a rate below € 32.34 excl. VAT implies that it concerns an employment relationship.

The amount of € 32.24 does not come out of the blue. It concerns 120% of the minimum wage based on a 36-hour working week, multiplied by a factor of 1.5. The idea behind the minimum rate is that an individual who performs work for such a low wage is, by definition, considered to be performing his activities on the basis of an employment agreement, so that he/she is entitled to employment law protection and, amongst other things, accrues a mandatory pension. In principle, only the worker himself can invoke this legal presumption. The employer can try to refute such presumption by submitting evidence that shows the lack of an employment relationship. Only when the legal presumption is confirmed by a court the qualification of the employment relationship also has a third-party effect, meaning that the Dutch Tax Authorities and pension providers may also rely on the existence of an employment agreement.

Tax consequences of the Proposal

However, the implications of the qualification of an (employment) agreement are broader than employment law alone. In case a legal relationship qualifies as an employment agreement, mandatory payroll taxes will be due. This implies that a levy of wage tax, national insurance contributions, income-related healthcare insurance contributions and employee insurance contributions are due on the income (salary) arising from the employment agreement. In addition, the employee may also be entitled to pension, which means pension contributions must be paid. In the Wage Tax Manual (Handboek Loonheffingen) of the Dutch Tax Authorities, a number of case positions are discussed where, in the opinion of the Tax Authorities, an employment relationship exists.

In addition, the ‘web module employment relationships assessment’ plays an important role. This web module offers an indication (as far as possible) on how a specific legal relationship should be qualified. The government has indicated that it wants to focus on more intensive use of the web module. For this purpose, the current questionnaire will be adapted on the basis of recent amendments to laws and regulations pursuant to the Proposal, and it will be examined whether the user-friendliness of the web module can be improved. The modified web module is expected to be available when the Proposal enters into force.

Next steps

The Proposal, if adopted in its current form, is expected to have far-reaching consequences for both workers and employers. Of course, this will also depend on the extent to which the Proposal will be enforced. For the time being, however, it is questionable whether the Proposal will bring the clarity that is needed in practice. In view of the initial reactions to the Proposal, it is not inconceivable that the Proposal will have to undergo the necessary amendments after the internet consultation has been closed. In addition, the upcoming elections might have an impact on the next steps; after all, it is uncertain how the new House of Representatives will view the Proposal.

It will be possible to respond to the Proposal until 10 November 2023. Entry into force of the Proposal is currently envisaged on 1 July 2025. Of course, we will continue to closely monitor the development concerning the Proposal and the implementation thereof. Should you have any questions in light of the above or should you need assistance with the legal qualification of an employment / services agreement, please feel free to contact us. We will be happy to assist you.