Work bonus system from July 2023

Employees pay 13.07% of their gross salary in social security contributions. Workers with lower wages are entitled to a reduction of these employee contributions or a (social) work bonus. The aim of this work bonus is to guarantee these workers a higher net wage without increasing the gross wage. In this way, the aim is to widen the gap between the lowest wages and unemployment benefits and thus combat unemployment traps.

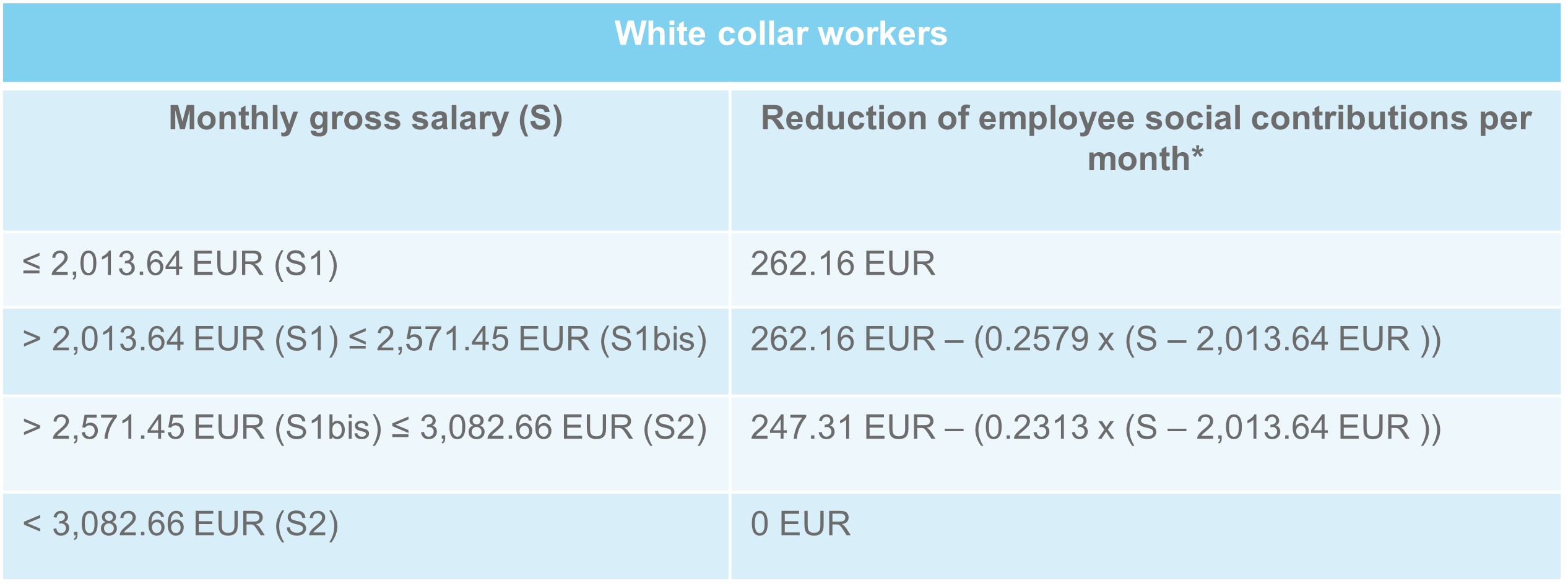

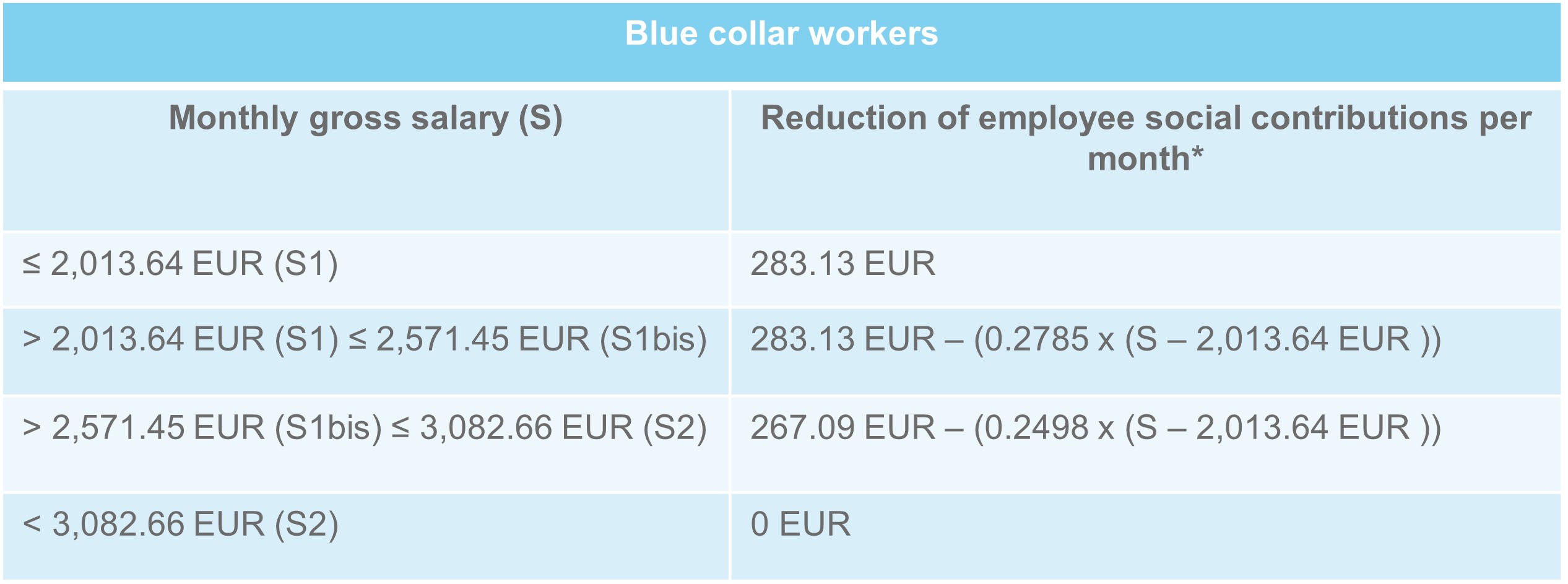

The reduction in employee contributions depends on the wage bracket the employee is in. The royal decree of 27 March 2023 increases, from 1 July 2023, the reduction amount for the lowest wage bracket and adds an intermediate threshold, namely S1bis. As a result, there will be 4 wage brackets instead of 3, as shown in the table below.

*The reduction amount is linked to the amount of the guaranteed average minimum monthly income (GMMMI/RMMG) of the National Labour Council.

For full-time employees with incomplete performances and part-time employees, the reduction in employee contributions is adjusted proportionally based on the performances. Moreover, per calendar year, the sum of all reductions is subject to certain maximum limit (EUR 2,967.72 per calendar year from 1 December 2022).

Since the taxable wage increases with a lower deduction of employee contributions, the tax legislation provides for a tax reduction, called the tax work bonus. This tax reduction is equal to 33.14% of the work bonus enjoyed during the taxable period with a maximum of EUR 910 (assessment year 2023).

The work bonus is a federal measure distinct from the Flemish Jobbonus. From 2023, employees domiciled in the Flemish Region will be eligible for this bonus from the Flemish government. One of the conditions is that they earned on average less than EUR 2,500 gross per month. The calculation of this limit amount is done on a quarterly basis.

Please note that, in the scope of the tax reform currently under discussion, the government is considering expanding the work bonus. At the moment, the draft texts are still subject to changes. We will keep you informed.

Reflections on the work bonus

The desire of policymakers to guarantee higher net salary to the lowest earners and curb unemployment traps is obviously legitimate.

As shown in the table above, this implies that an increase in the gross wage of the workers concerned will in any way reduce the benefit of the work bonus. More concretely, workers will receive barely, if at all, higher net wages than before the gross wage increase while employers will see their employer contributions rise.

Paid overtime will also cause an increase in monthly salary, which may result in less or no reduction in employee contributions.

For this reason, employers and unions are looking, within the legal framework, for alternatives to a wage increase that does not negatively affect work bonus while continuing to safeguard workers' purchasing power. These include, for example, the granting of non-recurring result-based benefits (CBA n° 90) or meal vouchers. The relance overtime can also be advantageous in this regard.

Do not hesitate to contact the Employment & Benefits team. We will be happy to assist you!

Related article: