Introduction

The Corporate Sustainability Reporting Directive (CSRD) is a European directive that requires companies within its scope to generate a sustainability report and that mandates an audit of this report. This sustainability report must contain information necessary to understand the impact of their business on sustainability matters, and how sustainability matters affect the development, performance and position of their business. This information must be published by means of said report on which a (limited) assurance must be provided by external party. The primary goal of the CSRD is to guarantee that companies and investors are provided with consistent and trustworthy sustainability information. This objective is pursued through the enforcement of a framework of regulations specifically crafted to harmonize sustainability reporting with established financial reporting standards.

The CSRD entered into force on 5 January 2023, but being a European directive it needs to be implemented by the EU Member States. This article offers insights into the progress of implementing the CSRD in the Netherlands and highlights our key takeaways.

More publications on the CSRD, and other sustainability legislation, can be found on our dedicated ESG webpage.

Dutch implementation process

To facilitate the integration of the CSRD into the Dutch legal system, the Dutch legislator has proposed the following implementation instruments:

- On 1 July 2022, the Dutch government published a Bill implementing directive (EU) 2021/2101 on disclosure of income tax information, which also introduces a new provision (Section 2:391a of the Dutch Civil Code (DCC). This provision provides a basis for establishing rules by governmental decree (Algemene Maatregel van Bestuur) to implement binding EU legal acts covering certain undertakings' obligations to include information in the management report. The Bill has been adopted by the Dutch House of Parliament, however adoption by the Dutch Senate is pending. The directive must be implemented into national legislation by 22 June 2024.

- On 17 July 2023, the Dutch government published a draft implementing Bill covering the rules on assurance of CSRD reports and the applicability of the CSRD to listed companies and other public interest companies as per the matrix set out below. The public consultation period ended on 10 September 2023, following which the Dutch legislator is expected to prepare a formal draft Bill which will then have to be submitted to the Dutch House of Parliament and the Dutch Senate.

- On 20 November 2023, the Dutch government published a public consultation regarding the Implementation Decree for the Corporate Sustainability Reporting Directive (Implementatiebesluit richtlijn duurzaamheidsrapportering) (Draft Decree). The Draft Decree includes the sustainability reporting requirements for the companies in scope which are to be drawn up in accordance with the European sustainability reporting standards (ESRS) developed by the European Commission, rules on the assurance statement and the audit committee, and implementation timelines. The consultation period for this Draft Decree expires on 18 December 2023, during which it is possible to submit feedback to the Ministry of Justice.

Our key takeaways

Timing of application of the CSRD

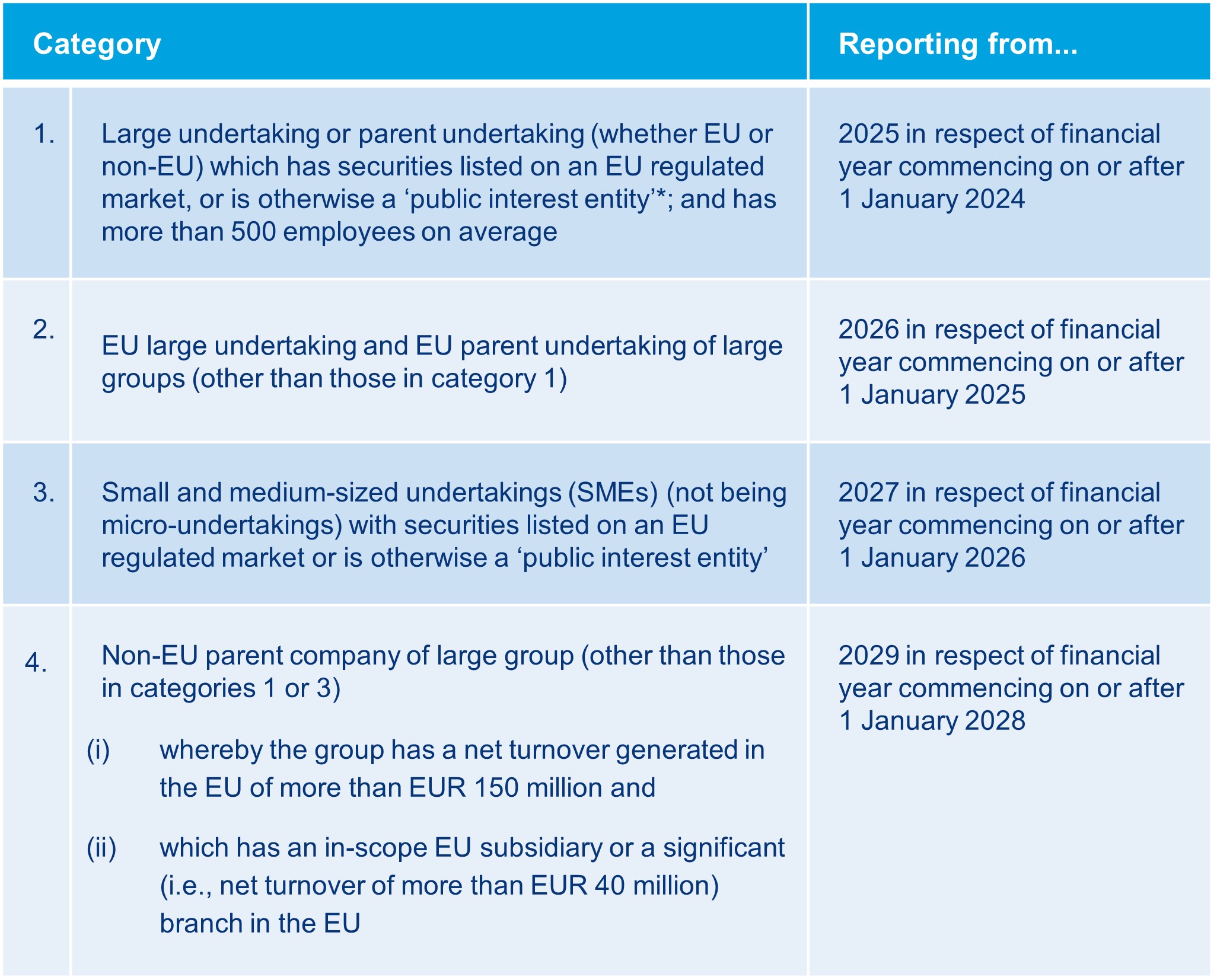

The CSRD must be implemented into national legislation by 6 July 2024, since in 2025 the first group of companies is required to publish their sustainability reports in respect of the financial year of 2024. As per the CSRD, the Draft Decree caters for a phasing in of the sustainability reporting requirements from 2024 to 2028 along for the following categories of companies:

*‘Public interest entity’ is defined under Article 2(1) of the Accounting Directive and includes EU undertakings having securities listed on a regulated market as well as certain other specific types of undertakings (such as credit institutions and insurance undertakings) and entities designated as such by the relevant Member State.

As regards the size criteria, please also see our previous publication.