Update 5 January 2024: On 21 December 2023, the Delegated Directive amending the Accounting Directive to adjust the monetary size criteria (balance sheet and net turnover) for micro, small, medium-sized and large companies by 25% was published in the Official Journal of the EU. Member States must update their local legislations in accordance with the Directive by 24 December 2024. Member States will apply the new size criteria in respect of financial years starting from 1 January 2024. However, the Delegated Directive allows Member States to allow companies to apply the adjusted size criteria already from financial year beginning on or after 1 January 2023.

General

On 17 October 2023, the European Commission (EC) adopted a Delegated Directive amending the Accounting Directive to adjust the monetary size criteria (balance sheet and net turnover) for micro, small, medium-sized and large companies by at least 25%, thereby reducing the number of companies that are in-scope.

The classification of undertakings or groups in the Accounting Directive is based on meeting at least two out of three size criteria: two monetary size criteria (balance sheet total and net turnover), and the average number of employees.

Under the Accounting Directive, the EC is required to review the monetary size criteria at least every five years to account for inflation. Considering the signification inflation trend during 2021 and 2022, the EC deemed it appropriate to increase the monetary size criteria by 25% (subject to rounding up) in order to account for inflation. The criterium for the average number of employees remains unchanged, despite some requests for an uplift during the consultation phase.

The proposal to adjust the size criteria forms part of a wider package aimed at simplifying reporting requirements in the EU aimed at reducing the reporting burden on companies by 25% which was announced in March 2023. A set of proposals to achieve this reduction is included in the Commission Work Programme 2024.

Proposed adjustments

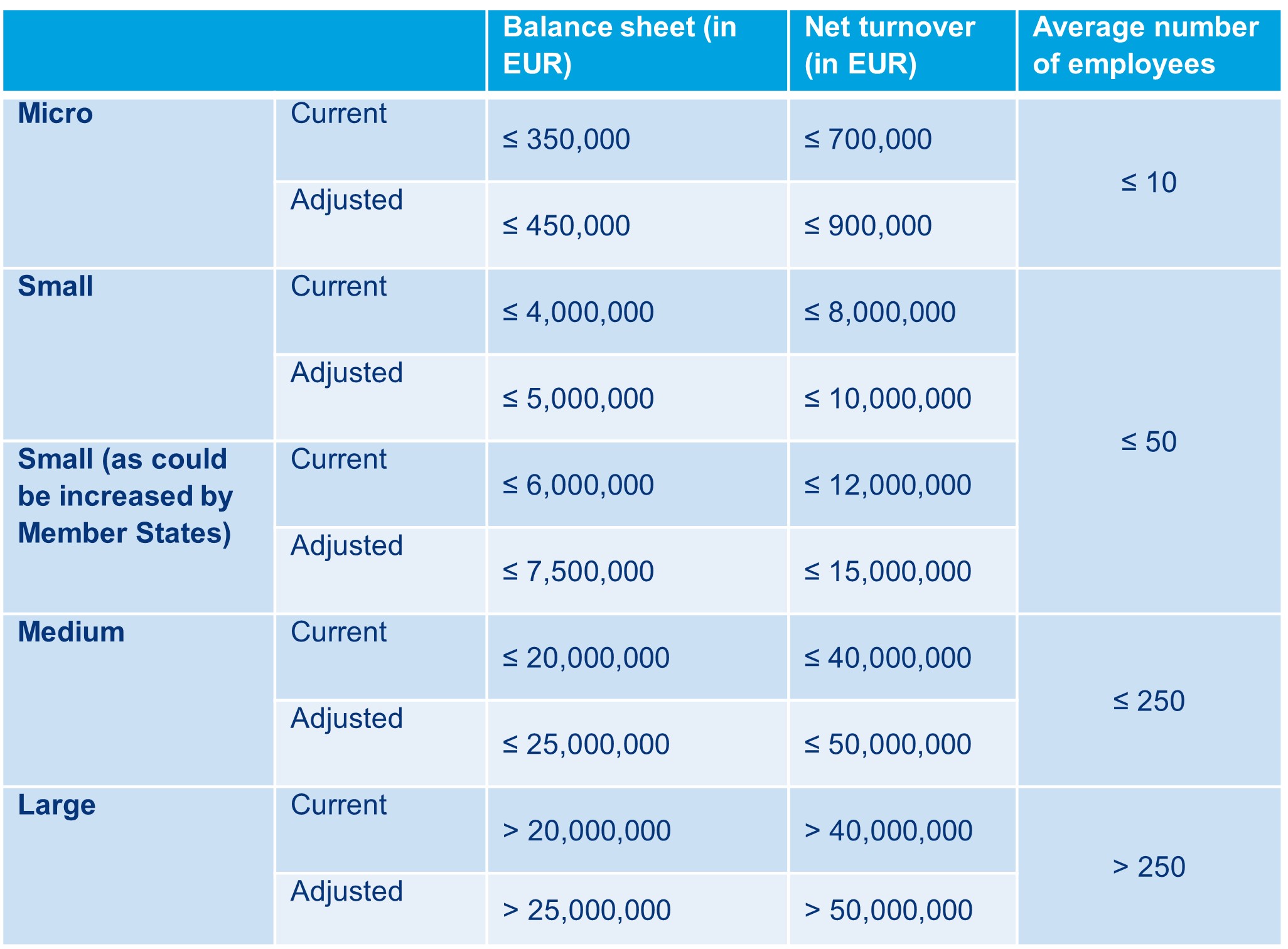

As a result the size criteria for micro, small, medium-sized and large companies will be adjusted as follows:

Impact

The EC estimates that 6% of companies in the EU will benefit from the increased size criteria as they result in an alleviation of their reporting and audit obligations.

The new size criteria will reduce the scope of application of presentation, audit, and publication requirements laid down in the Accounting Directive. Furthermore, in line herewith, the scope of application of the Corporate Sustainability Reporting Directive (CSRD) and the Taxonomy Regulation will also be reduced as those regulations are aimed at large undertakings, listed small and medium-sized undertakings, as well as large groups.

Moreover, where the application of (additional) local reporting requirements in a relevant Member State is also linked to the size of companies, fewer companies will become subject to such local reporting requirements. For example, in the Netherlands fewer companies should become subject to the reporting requirements on the gender diversity of their boards and senior management as those requirements only apply to “large” N.V.s and B.V.s. In Belgium, for instance, reporting obligations regarding the issuance of convertible bonds or subscription rights by the board of directors as well as the usage of authorised capital by the latter to increase the capital of an NV are only applicable insofar the NV does not qualify as a small company. Similarly, in Luxembourg, the option to replace the advisory vote on the remuneration report with a discussion in the general meeting on the same is anticipated to become available to a greater number of public companies, encompassing those redefined small- and medium-sized companies.

Timing

Member States will apply the new size criteria in respect of financial years starting from 1 January 2024. However, the Delegated Directive allows Member States to allow companies to apply the adjusted size criteria already from financial year beginning on or after 1 January 2023.

The Delegated Directive will be subject to a two-month scrutiny by the European Parliament and the Council of Europe. Provided there are no objections from these two bodies, it will then be published in the Official Journal of the EU and will enter into force on the third day after its publication.