As from 1 January 2020, the MLI started to modify a large number of existing bilateral tax treaties with anti-tax avoidance measures developed in the OECD BEPS project. The impact of these bilateral choices on a specific tax treaty also depends on the choices made by the other treaty jurisdiction of that specific tax treaty.

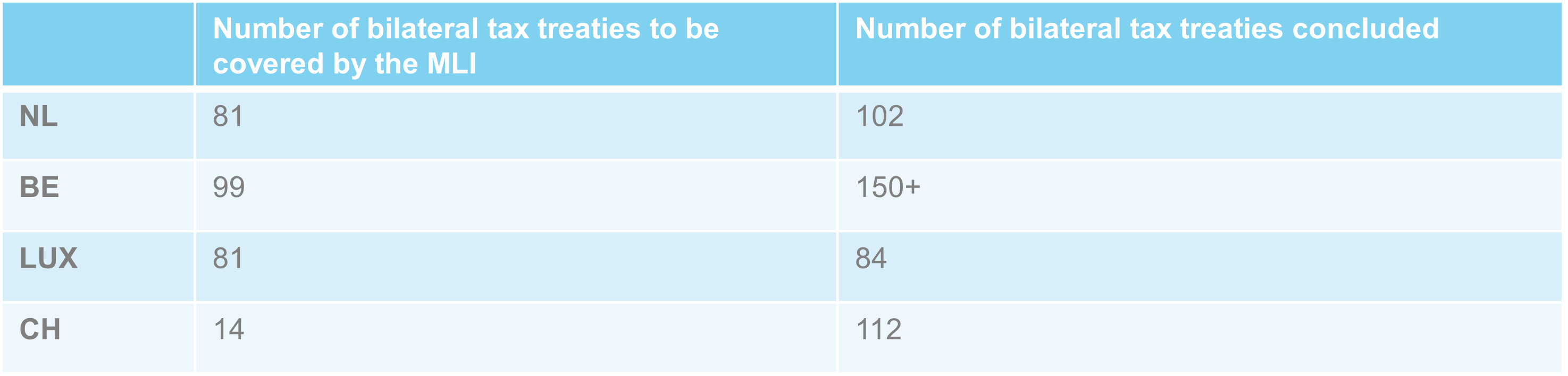

Number of tax treaties notified

The Netherlands has not notified the following bilateral tax treaties to the OECD: Belgium, Brazil, Bulgaria, Denmark, Ireland, Kosovo, Kyrgyzstan, Poland, Spain, Switzerland, Taiwan and Ukraine.

Belgium has not notified the following bilateral tax treaties to the OECD: Germany, Japan, Norway Taiwan, and Switzerland.

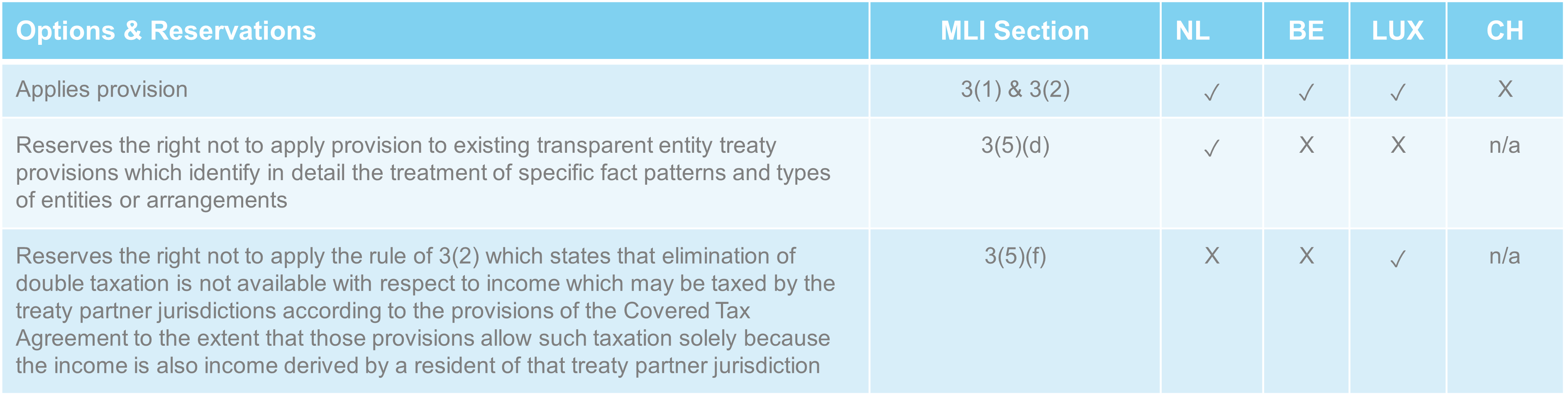

MLI Measure 3: Transparent Entities

Income derived by or through a transparent entity is only to be considered income of a resident of a treaty jurisdiction (and thus eligible for treaty benefits) to the extent that income is treated as income of a (another) resident by that treaty jurisdiction.

MLI Measure 4: Dual Resident Entities

The treaty residency of a dual resident entity is determined by mutual agreement between the treaty jurisdictions. Treaty benefits are in principle withheld from the entity until such mutual agreement is reached.

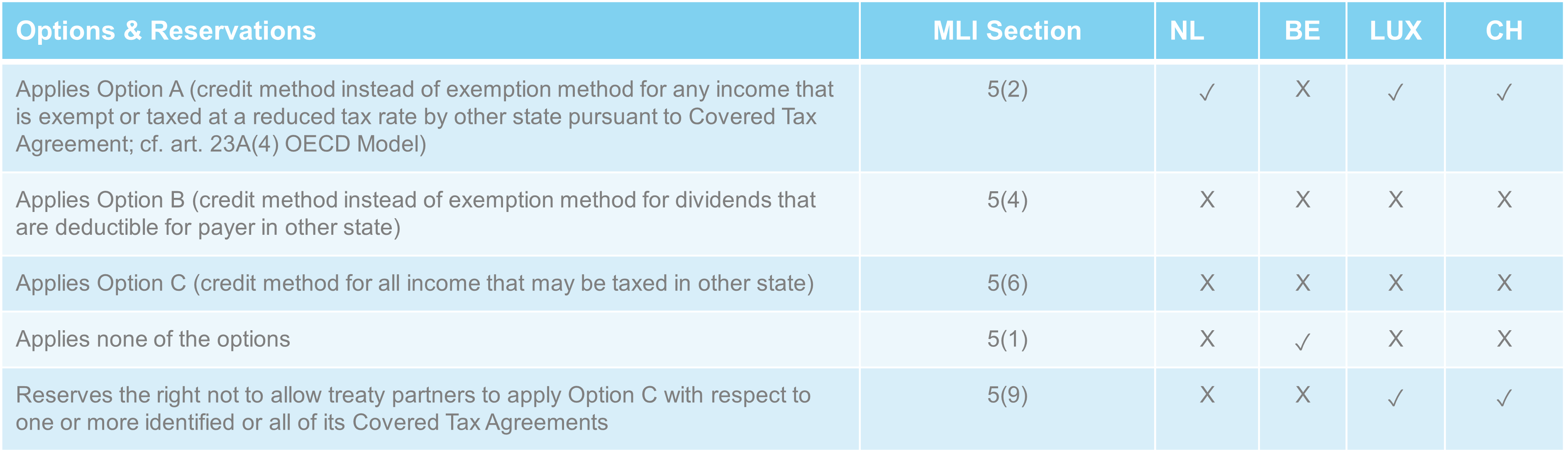

MLI Measure 5: Application of Methods for Elimination of Double Taxation

Provides three options to countries with respect to elimination of double taxation: (a) disallow the exemption method for income that is exempt or subject to a reduced treaty rate in the other jurisdiction, (b) disallow the exemption method for dividends that are deductible in the other jurisdiction and (c) solely apply the credit method.

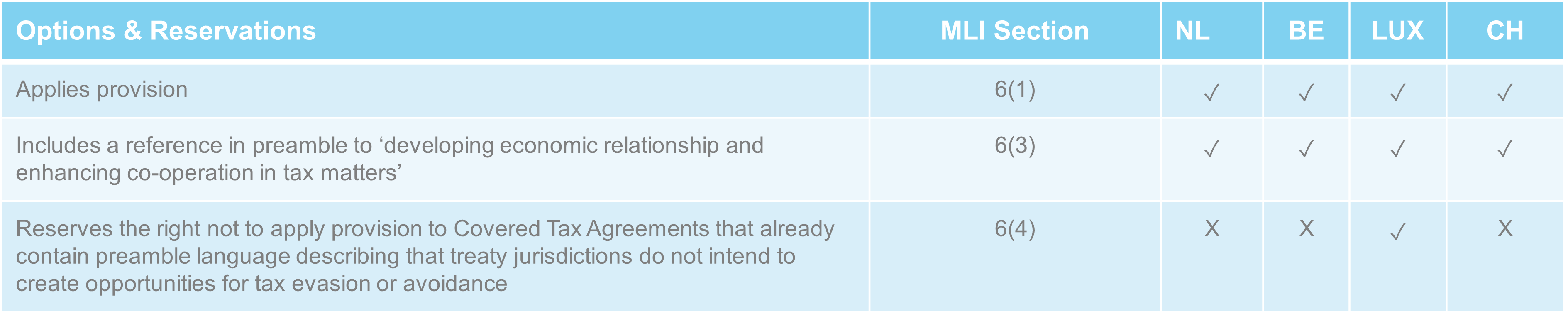

MLI Measure 6: Purpose of a Covered Tax Agreement

Includes language in the preamble of tax treaties stating that treaty jurisdictions do not intend to create opportunities for tax evasion or avoidance. As a BEPS minimum standard this provision is mandatory.

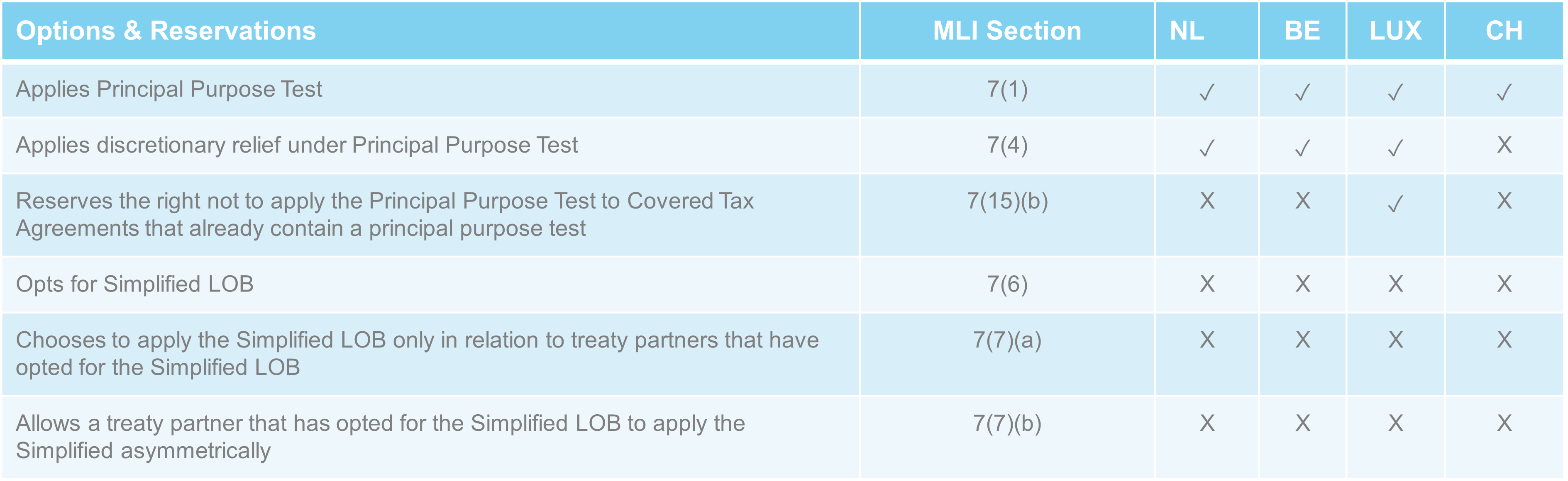

MLI Measure 7: Prevention of Treaty Abuse

As a BEPS minimum standard, countries must include one of the following in their tax treaties: (i) a principal purpose test ("PPT"), (ii) a PPT together with a simplified limited limitation on benefits ("LOB") test or (iii) an extensive LOB together with an anti-conduit provision.

MLI Measure 8: Dividend Transfer Transactions

A reduced rate of source state taxation on dividends pursuant to a tax treaty only applies if a minimum ownership threshold required by the tax treaty is met throughout a retrospective 365-day testing period.

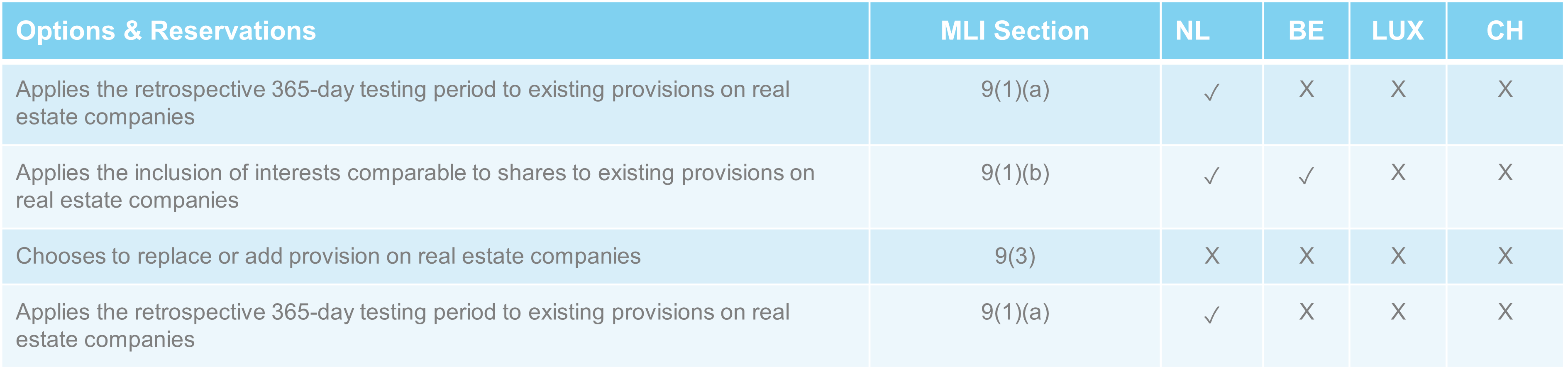

MLI Measure 9: Capital Gains on Shares in Real Estate Companies

Includes a retrospective 365-day testing period with respect to a value threshold in the definition of ‘real estate company’ in a tax treaty and/or includes ‘ownership interests comparable to shares’ in Covered Tax Agreements that already includes provisions to tax capital gains derived from shares in real estate companies, or (optionally) replaces existing Covered Tax Agreement provisions entirely with the new art. 13(4) OECD Model as per the final BEPS Action 6 report, or adds this provision to Covered Tax Agreements currently lacking a provision on real estate companies.

MLI Measure 10: Third-country PE

Denies treaty benefits for income that the state of residence of the taxpayer attributes to a low-taxed permanent establishment (PE) of the taxpayer in a third country, unless an active trade or business is carried out in that PE.

MLI Measure 11: Savings Clause

Allows a state to tax its own residents notwithstanding the provisions of a tax treaty.

MLI Measure 12: Artificial Avoidance of PE Status – Commissionaire Arrangements

Lowers the threshold for the existence of a dependent agent PE to include foreign persons acting on behalf of a taxpayer that habitually play a principal role in the conclusion of contracts on behalf or by the taxpayer.

1. At the initiative of the Dutch Lower House, the Netherlands is obliged to make a full reservation on MLI Measure 12. Before opting in to this provision, the Dutch government has to ensure that there is either sufficient clarity on profit allocation to agency PEs or that there is an effective dispute resolution mechanism in place with sufficient other MLI parties. If adequate progress is made, a legislative proposal to withdraw the Dutch reservation may be submitted by the end of 2020. Under the applicable entry into effect rules of the MLI, a withdrawal of the Dutch reservation, i.e. opting in to MLI Measure 12, will generally be effective at the earliest for tax book years beginning on or after 1 January 2022.

MLI Measure 13: Artificial Avoidance of PE Status – Specific Activity Exemption

Stipulates that: (a) the specific activity exemption in the treaty definitions of a PE applies only to activities of an auxiliary or preparatory character or (b) the specific activity exemption in the treaty definitions of a PE applies irrespective of whether an activity is of an auxiliary or preparatory character. The anti-fragmentation rule aggregates activities carried on by closely related enterprises for purposes of determining the existence of a PE.

MLI Measure 14: Splitting-up of Contracts

For the determination if a building site, or construction or installation project constitutes a PE, (i) activities carried on during one or more periods of time that, in the aggregate, exceed 30 days and (ii) connected activities carried on by closely related enterprises, are aggregated.

MLI Measure 15: Definition of ‘Closely Related Persons’

Persons are closely related if one has control of the other or both are under the control of the same person. A close relationship is deemed to exist in case a threshold of 50% of vote and value in a company is met.

MLI Measure 16: Mutual Agreement Procedure

Implements the BEPS minimum standard for mutual agreement procedures which is intended to ensure an effective and timely resolution of treaty-related disputes. The BEPS minimum standard is complemented by optional best practices.

MLI Measure 17: Corresponding Adjustments

Requires jurisdictions to make an adjustment to the profits of a taxpayer in its jurisdiction if the other contracting jurisdiction makes an at arm’s length pricing adjustment to the profits of a taxpayer in that other contracting jurisdiction. Any increase or decrease in that other jurisdiction would be mirrored by a corresponding adjustment to the profits of the taxpayer in the first jurisdiction.

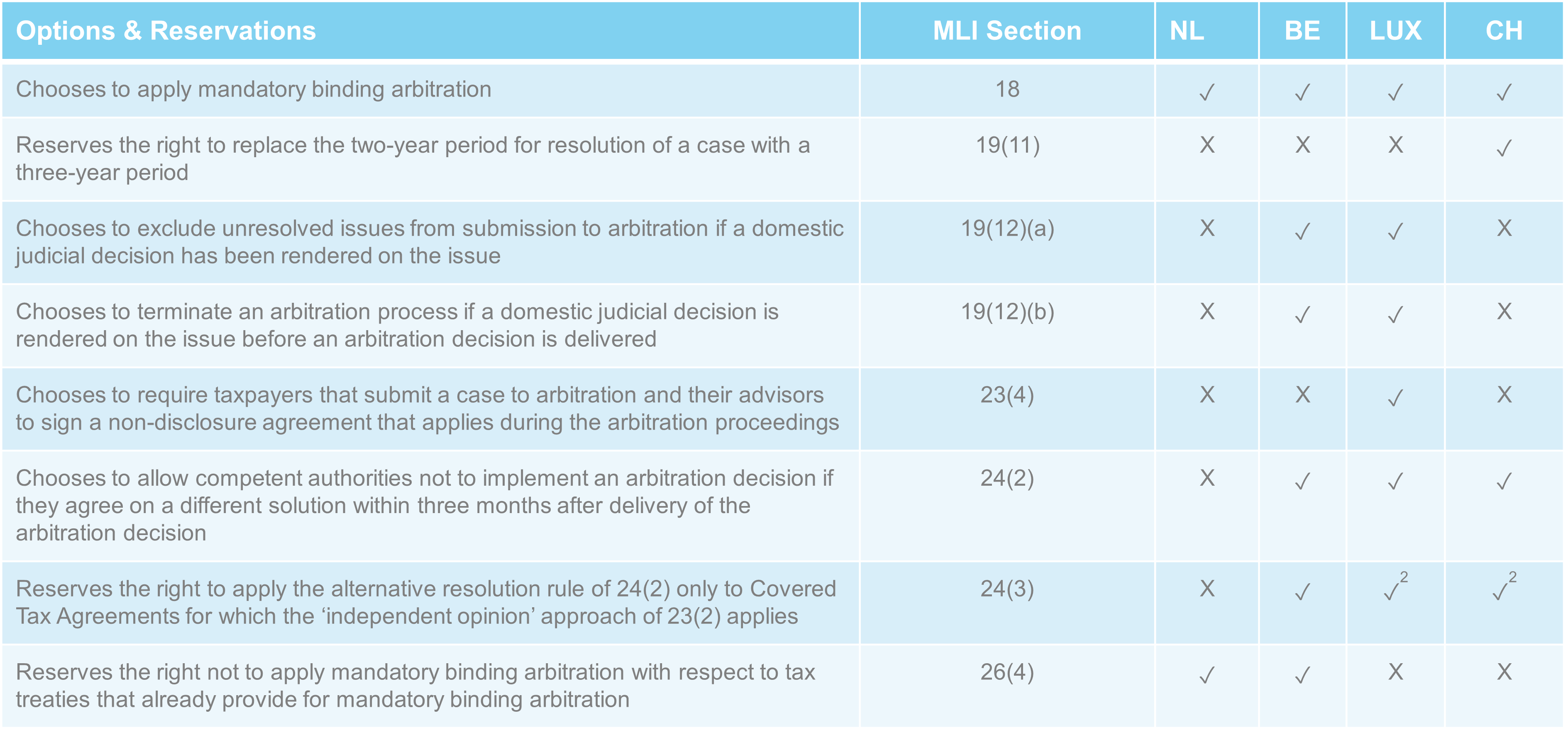

MLI Measures 18/19/23/24/26: Mandatory Binding Arbitration

Provides countries the option to implement mandatory binding arbitration in their tax treaties as a dispute resolution mechanism for disputes that prove unable to be solved through a mutual agreement procedure.

2. Luxembourg and Switzerland have stated in their provisional lists of reservations and notifications that they reserve the right not to apply the alternative resolution rule of 24(2) to Covered Tax Agreements for which the ‘independent opinion’ approach of 23(2) applies. However, this is not an option provided by the MLI. Therefore, we assume that Luxembourg and Switzerland intended to reserve the right to apply the alternative resolution rule of 24(2) only to Covered Tax Agreements for which the ‘independent opinion’ approach of 23(2) applies, in accordance with the provisions of the MLI.

MLI Measures 35/36: Entry into Effect

Contact your MLI specialist

This high level overview is provisional and cannot be seen as tax and/or legal advice. Please contact one of our MLI specialists before taking any action based on this publication.