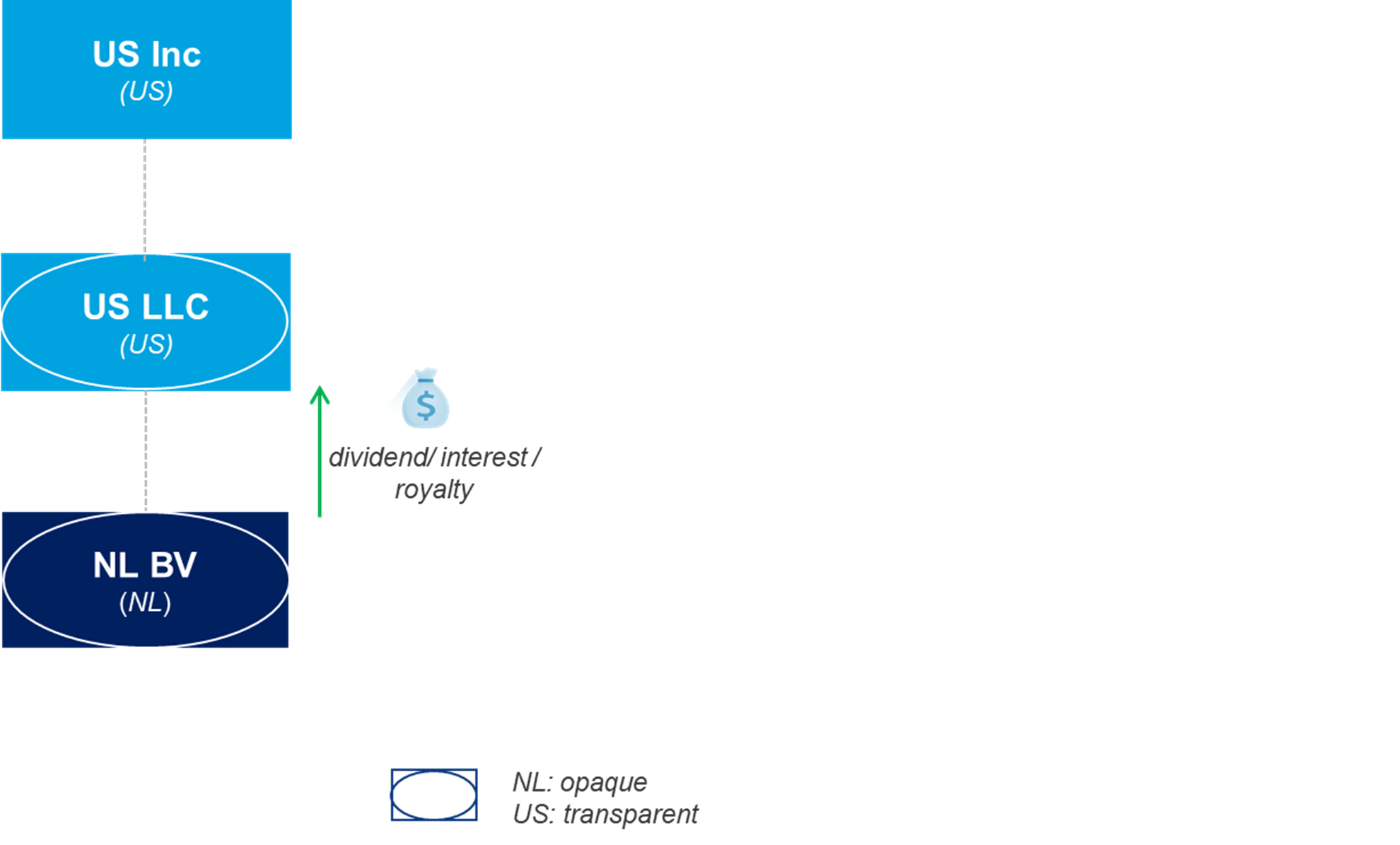

In the structure depicted below, both NL BV and US LLC are disregarded (transparent) from a US tax perspective. Previously, it was uncertain whether the non-hybrid participant in US LLC (i.e. US Inc.) could be considered the recipient of the dividend, interest or royalty payment made by NL BV under the hybrid rules of the DWT and CWT. This since such payments from NL BV to US LLC are not ‘visible’ for US tax purposes.

In the Decree, the Dutch State Secretary of Finance clarifies that in line with article 24(4) of the tax treaty between the US and the Netherlands, the non-hybrid participant in US LLC (i.e. US Inc.) can be considered the recipient of these payments under the condition that the underlying income from which the payment is made is included in the taxable basis of that participant. NL BV needs to make this plausible for example, through a US federal income tax return. Timing differences are catered for; it is not required that the underlying income is recognized at the level of the participant in the same year as the dividend, interest, or royalty payment was made. Consequently, and provided that all other conditions are met, the DWT exemption should be applicable respectively no CWT should be due.

In addition to this clarification, a 1997 Decree on tax treaty application for hybrid entities has been revoked by the Dutch Ministry of Finance. The 1997 Decree provided for unilateral relief in certain hybrid situations where the provisions of the relevant tax treaty did not provide for relief as a result of the hybrid nature of the recipient of the income. Structures which relied on the 1997 Decree must be reviewed, mainly in case relief is needed and the relevant tax treaty does not contain a provision on hybrid entities like article 1 section 2 of the OECD Model Convention.

We will keep you informed of further developments. For further information and in case you have queries, please contact your trusted advisor within Loyens & Loeff.