The STTR allows a source state that has ceded taxing rights on certain mobile intragroup payments under the normal allocation rules of a DTT, to reclaim taxing rights in certain circumstances where the intragroup payment is taxed at an (adjusted) nominal rate of less than 9%. The STTR would not apply if the source country can already sufficiently tax this payment under the normal allocation rules of the DTT. The STTR is a separate DTT provision that applies before the so-called GloBE Top-up Tax rules.

The STTR was originally proposed to be a withholding tax. However, because the STTR heavily relies on information that is only known after year-end, the STTR will be levied as an ex-post annualised charge.

To facilitate the implementation of the STTR in DTTs, the OECD / IF will make a multilateral instrument available for signature as from 2 October 2023.

Which payments are in scope?

The categories of income targeted by the STTR

The STTR applies to seven categories of income, which most notably include interest and royalties. Other covered income under the STTR is (i) insurance and reinsurance premiums, (ii) payments for the (right to) use of distribution rights in respect of a product or service, (iii) financial guarantees or financing fees, (iv) payments for the (right to) use of industrial, commercial or scientific equipment and (v) any income in relation to the provision of services (the latter category is particularly broad).

Specific items of income have been excluded for the shipping industry.

Exclusions based on the recipient

The STTR does not apply to payments made by individuals nor to payments made to individuals or other persons not connected to the payor. There is an anti-abuse rule that aims to tackle structures where entities are interposed to avoid the STTR.

In addition, payments made to certain entities are excluded from the scope of the rule based, for example, on their characteristics or functions. These entities often are not exposed to CIT to preserve a specific intended policy outcome, e.g., recognized pension funds, certain investment funds or non-profit organizations. The types of excluded entities are defined by the STTR model treaty provision, and the scope should therefore be reviewed carefully.

Exclusions based on the amount

Moreover, as a general rule the STTR would not apply if the gross amount of the covered income (not being interest or royalties) does not exceed a cost +8.5% remuneration of the recipient for the activity giving rise to such income, since it is considered that these items present a more limited BEPS risk.

Exclusions based on materiality threshold

Contracting states should introduce a materiality threshold below which the STTR will not apply. The materiality threshold operates by reference to the total value of payments arising in the source state and paid to connected recipients which are resident in the other contracting state. For contracting states with a GDP ≥ EUR 40 billion, the threshold of covered income in a year should be set at EUR 1 million. For contracting states with a GDP < EUR 40 billion, the threshold should be EUR 250,000. The applicable threshold is determined by reference to the size of the smallest economy of the two contracting states.

How is the amount of additional tax under the STTR computed?

The STTR allows the source state to apply additional tax on an item of covered income that is subject to an adjusted tax rate below 9% in the recipient state. When determining this additional tax, the tax rate applying in the recipient state to the covered income must be considered, as well as the tax rate that the source state is allowed to apply pursuant to the normal allocation rules of the DTT.

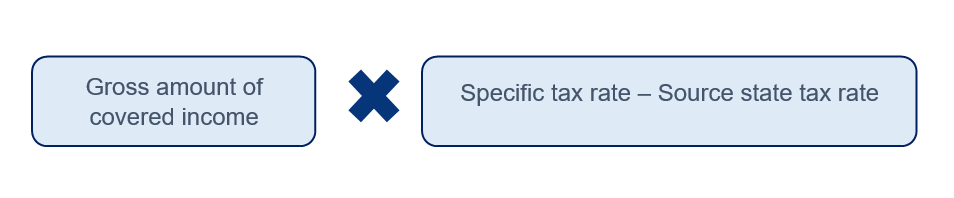

The additional tax that the source state can levy is determined as follows:

In effect, the specific tax rate that may be applied under the STTR is capped at the difference between 9% and the (adjusted) nominal rate applicable in the recipient state. Such nominal rate will in many cases be the main CIT rate.

An adjustment to the nominal rate in the recipient state must be made to take into account preferential rates applicable in that jurisdiction to the covered income, e.g., because of a permanent partial exemption or exclusion of such income from the tax base where such preferential treatment is “directly linked” to the relevant covered income or “arises from a regime that provides a tax preference for income from geographically mobile activities”. Specific rules are in place for the application of the STTR in case of payments to permanent establishments.

Because the STTR applies after other taxing rights allocated to the source state, the tax rate under the STTR is further reduced by the rate at which the source state is already allowed to tax the gross amount of covered income (regardless of whether the source state exercises that right or not). Therefore, if the DTT already allows the source state to tax the gross amount of covered income at a higher rate than under the STTR, the STTR does not apply.

How the source state levies the additional tax under its domestic tax law is not relevant, as long as the tax does not exceed the amount resulting from the above-mentioned formula.

To facilitate tax certainty, the competent authorities must notify each other of the applicable rates and other features of their tax laws that are relevant to the application of the STTR.

STTR compliance

The details of the tax compliance process, e.g., as regards certifications or deadlines, are left to the parties to each relevant DTT but conceptually the OECD / IF proposes that the STTR liability is determined by means of self-assessment through the filing of an STTR tax return in the source country only if the recipient of the payment has an STTR liability. That determination is made after the end of the fiscal year, once all financial and tax data points relevant to the computation of a potential STTR tax liability are known.

Interaction with other DTT provisions and other Pillar Two measures

The OECD / IF also proposes to amend the DTT provision on the elimination of double taxation in order to avoid that recipient states unduly grant exemptions or credits in case the source state levies tax solely based on the STTR.

The STTR should apply before the GloBE rules, i.e., any tax levied pursuant to the STTR should be taken into account when computing the GloBE effective tax rate.

Take-aways

Contrary to the GloBE rules, the STTR does not apply solely to groups that have a consolidated turnover of at least EUR 750 million. Other thresholds and exclusions (outlined above) should, however, limit the otherwise potentially very broad scope of the rule.

Moreover, the STTR does not affect every DTT. Many jurisdictions have a statutory tax rate of at least 9%, though specific adjustments (e.g., due to specific tax exemptions or reductions applicable to certain categories of covered income) need to be factored in the assessment. However, where the STTR is implemented into the DTT, the STTR appears more complex than originally expected.

As regards implementation, the OECD / IF specifically mention that members of the IF that apply nominal tax rates below 9% to the defined set of payments have committed to implementing the STTR into their DTTs with IF developing countries when requested to do so. As mentioned above, to facilitate the implementation of the STTR in DTT’s, a multilateral instrument should be available for signature as from 2 October 2023.

In parallel to the STTR model provision, the OECD also released additional administrative guidance (see our website article) and a revised GloBE Information Return for compliance with the GloBE Rules (see our website article).

We will keep you informed of further developments. In case of any question, please contact an author of this tax newsletter or your trusted Loyens & Loeff adviser.