Background and the interpretation

The AFM's interpretation is a consequence of a judgment of the Court of Justice of the European Union (CJEU 29 September 2022, C-633/20, ECLI:EU:C:2022:733). With the interpretation, the AFM provides further guidance for practice. According to the parliamentary history of the concept of the provision of intermediary services, the term "intermediary" expresses that the intermediary does not become a party to the insurance contract. However, the CJEU does not consider it decisive whether the intermediary is itself a party to the insurance contract, what is relevant is whether a party performs similar activities for a fee.

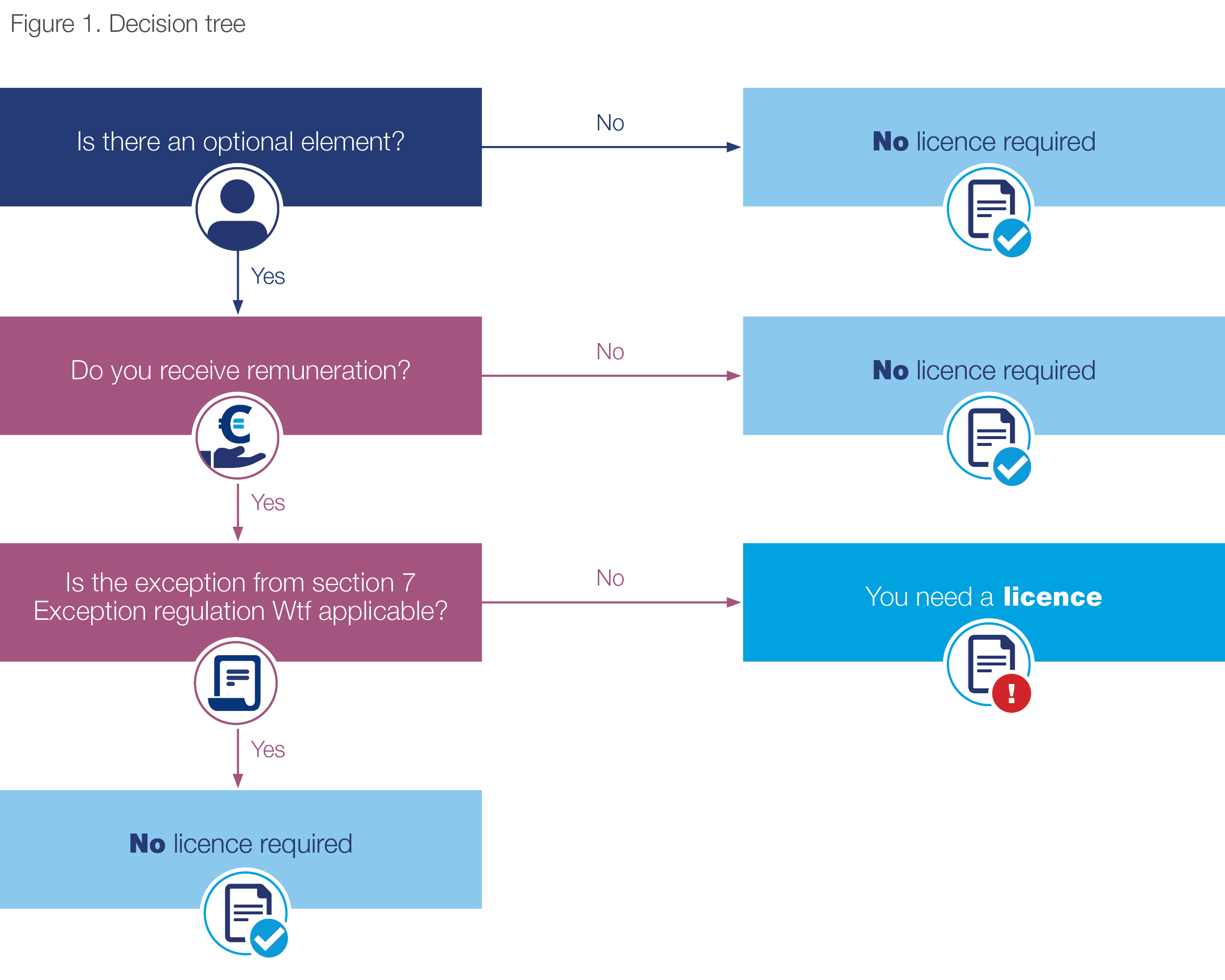

Licensing requirement for group insurances

A group insurance is an insurance contract entered into between a policyholder and insurer under which one or more third persons may be included as insured person(s) on the policy. According to the AFM's interpretation, if the following two conditions are met for group insurance, there is a licensing obligation for the provision of intermediary services:

- There is an optional element; and

- A fee is paid.

Optional element - automatic or non-automatic inclusion

If the insured is automatically added to a group insurance policy and does not have an option to do so, this does not constitute intermediary activities for which a licence is required. This could include the situation where a child is enrolled by its parents at a school, where the child is automatically added as an insured in the school's accident insurance.

It is different when the insured has the choice to join the insurance contract, which allows the insured to decide whether to take up the offer of insurance. This is non-automatic entry. The offering of certain options or the possibility of dropping certain options within the offered insurance is also seen by the AFM as an optional element. By way of illustration, this includes the situation where a moving company offers the option of taking out insurance against damage to the goods on the moving day.

Remuneration

In addition to the fact that there must be a non-automatic entry into a group insurance policy, the policyholder must receive remuneration for the service provided in order to trigger the licence requirement. The concept of remuneration should be interpreted broadly. Any (economic) benefit of any kind qualifies as a remuneration.

The AFM clarifies in its interpretation that there must be a financial benefit for the policyholder - passing on premiums and (administrative) costs is not considered as a fee by the AFM. This means that if the group insurance is offered to the customer as a 'service' without providing any financial benefit to the policyholder, there are no intermediary service provided for which a licence is required.

Secondary insurance intermediary: exception from Section 7 Exemption regulation Wft

In the situation where there is (i) freedom of choice for the customer and (ii) a remuneration for the policyholder, in principle, a licensing obligation as intermediary applies. In those cases, the exemption regulation is still relevant. Section 7 of the Exemption regulation Wft (Vrijstellingsregeling Wft) regulates that persons who mediate in insurance in addition to the supply of an item or the provision of a service are largely exempt from the Dutch Act on Financial Supervision (Wet op het financieel toezicht) under certain conditions. To qualify for this exemption, certain conditions must be met. This means that if the policyholder of a group insurance policy can demonstrate that the insurance product being offered meets the conditions set out in Section 7 of the Exemption regulation Wft, the policyholder can make use of this exemption and the licensing obligation does not apply after all. The foregoing can be depicted as follows:

Based on the interpretation of the AFM.

Next step

The AFM's interpretation may have a significant impact on market parties who currently do not have a licence for (intermediary) activities in group insurance. For each group insurance policy, it will have to be determined whether there are intermediary activities that requires a licence. The decision tree as depicted above can be helpful in this respect. If a licensing obligation arises, we recommend taking action on this quickly, as the relevant companies must have a licence no later than 1 October 2025.

Contact

Do you have questions about the AFM's interpretation, its impact on your organisation or other financial regulation topics? If so, please contact our Financial Markets & Products team.