By adopting Regulation (EU) 2019/1156 on facilitating cross-border distribution of collective investment undertakings (‘CBDF Regulation’) and Directive (EU) 2019/1160 on facilitating cross-border distribution of collective investment undertakings, the EU aims to create a level playing field for the cross border marketing and distribution of funds in the EEA, while at the same time ensuring more uniform and better protection for investors.

Following the CBDF Regulation, applicable as of 2 August 2021, AIFMs, EuVECA managers, EuSEF managers and UCITS management companies must ensure that all marketing communications addressed to investors are:

- identifiable as being marketing communications, and

- describe the risks and rewards of purchasing units or shares of an AIF/UCITS in an equally prominent manner, and

- contain information which is fair, clear and not misleading.

The ESMA guidelines on marketing communications under the Regulation on cross-border distribution of funds (‘ESMA Guidelines’) aim to further clarify the requirements that funds’ marketing communications must meet when directed at professional or retail investors.

Do not hesitate to contact the authors for more information about the marketing of funds in one of our home jurisdictions or regarding additional national requirements regarding marketing communications.

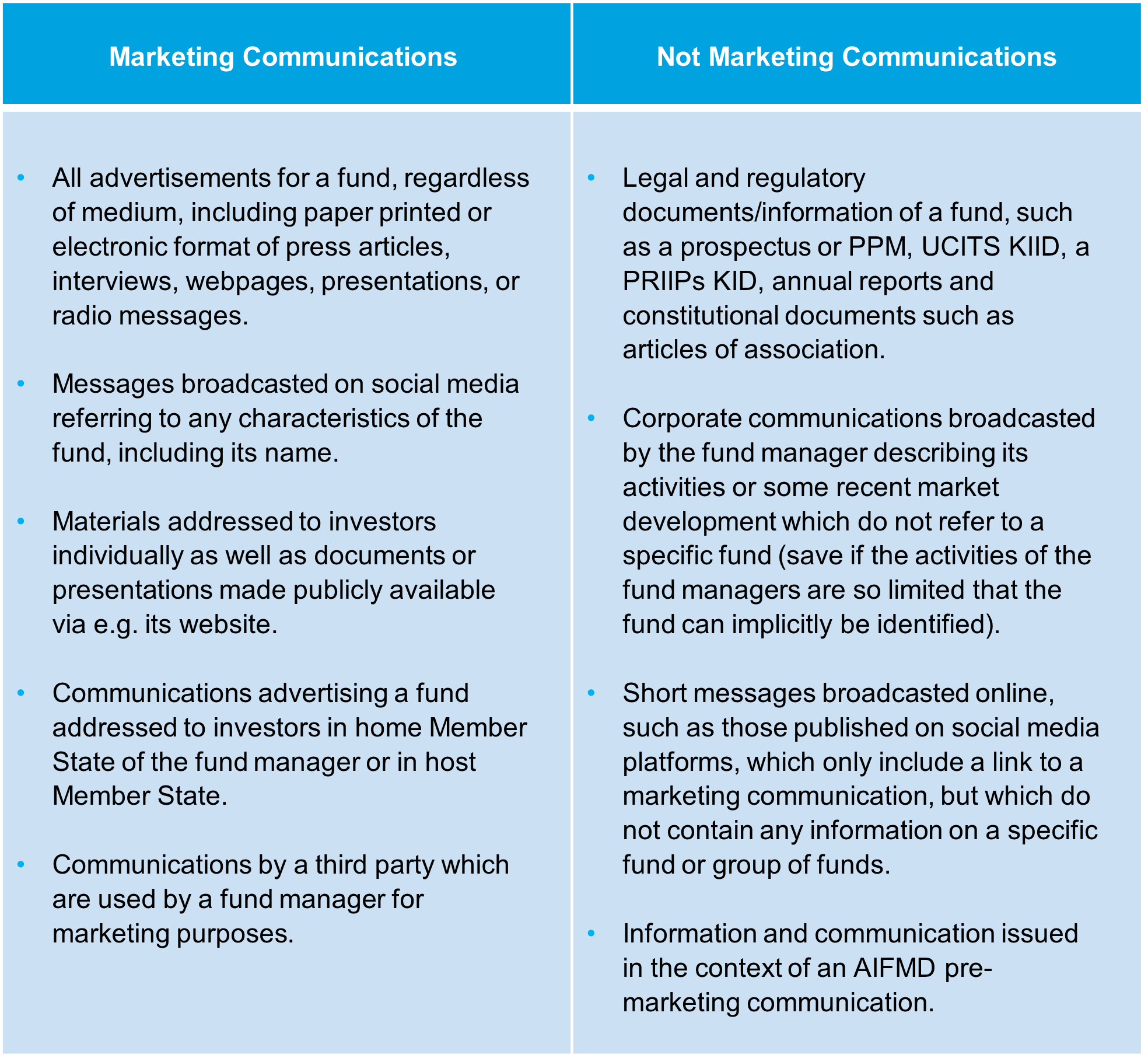

What is marketing communication?

No definition of ‘marketing communication’ can be found in the CBDF Regulation or in the ESMA Guidelines. However, the ESMA Guidelines classify a non-exhaustive list of type of communications as marketing communications (or not):

Requirements that funds’ marketing communications must meet

If a communication qualifies as a ‘marketing communications’ in the meaning of the CBDF Regulation or the ESMA Guidelines, such communications must comply with strict legal requirements.