Energy Investment Allowance (EIA)

The Energy Investment Allowance (EIA) is a tax incentive scheme designed to stimulate investments in energy efficient technologies, CO2 reduction measures and renewable energy assets by businesses. The EIA allows for a one-time deduction in addition to the regular depreciation of an asset of 40% of the investment amount, providing a permanent reduction in corporate income tax liability.

The maximum eligible investment amount under the EIA is capped at EUR 151 million, with a distinction made between taxpayers who (a) operate a standalone business and (b) operate a business which is part of a partnership. To prevent taxpayers from exceeding this cap by claiming EIA on energy investments made both individually and through partnerships, a new consolidation provision is being introduced. Under the proposed measure, the total amount in investments eligible for EIA cannot exceed EUR 151 million per taxpayer per year.

Energy tax

For the supply of electricity to grid connections that have a dwelling function (“verblijfsfunctie”), currently a generic energy tax deduction of EUR 524,95 applies. It is proposed to increase this deduction by EUR 9,30 as of 1 January 2026.

It has previously been suggested to limit the energy tax deduction to households only. Contrary to expectations, this suggestion has not been included in the current legislative proposals.

The energy tax contains several exemptions, including for electricity and/or gas used for metallurgical or mineralogical processes. To determine eligibility, the Standard Industrial Classification (Standaard Bedrijfsindeling, SBI) is used. This classification will be updated to ensure it remains aligned with current economic realities and is comparable across the EU. The existing SBI 2008 codes (SBI2008) will be replaced by the new SBI 2025 codes (SBI2025).

CO2-levies

The CO2 levy for industry is – in short – due for companies that fall under the ETS 1 system as well as nitrous oxide and waste disposal installations. It effectively functions as a minimum CO2 price and is only levied insofar the average EU ETS price falls under a certain price level. Each company also obtains a certain amount of free dispensation rights.

During 2025 the minimum price was EUR 87,90 per ton CO2, and it was planned to increase this rate to EUR 100,74 per ton CO2 as of 2026. In light of challenging market conditions, the government will reduce the minimum CO2 price as of next year to EUR 78,67 per ton CO2. Additionally, the number of dispensation rights will be increased to 1.023 and will remain constant beyond 2026, rather than being phased out.

Although the CO₂ levy will not be officially abolished, these adjustments are expected to result in minimal financial impact from 2026 onwards. However, if the levy rate exceeds the ETS price, some companies may still be subject to the levy.

The relief measures introduced for the CO2 levy for industry do not apply to waste incineration plants. For these installations, the levy will be tightened as part of a broader climate policy package:

- The rate will gradually increase to EUR 295 per ton of CO₂ by 2030 (baseline: EUR 152).

- The exempted emissions will remain at the baseline level (0,6 Mton fossil CO₂ emissions) until 2030, after which they will be phased out in equal steps until reaching zero by 2033.

- Trading of dispensation rights between waste incineration plants and other industrial installations will be prohibited.

Water tax

Water tax is currently due on the supply of water (at a rate of EUR 0,425 per m3), but only up to 300m3 of water supplied per year. It is proposed to increase this cap to 50.000 m3 as of 1 January 2026 and to abolish this cap as of 1 January 2027.

Water tax is currently due on all water delivered via a water grid, which includes water that is not of drinking quality (such as river water or recycled water). As of 1 January 2027, water tax will only be due on the supply of water of drinking quality.

Currently, suppliers with less than 1.000 grid connections are exempt from water tax. This exemption will be abolished as of 1 January 2027 and replaced with an exemption for supplies by a “small or very small collective water supply” as meant in the Drinking Water Act.

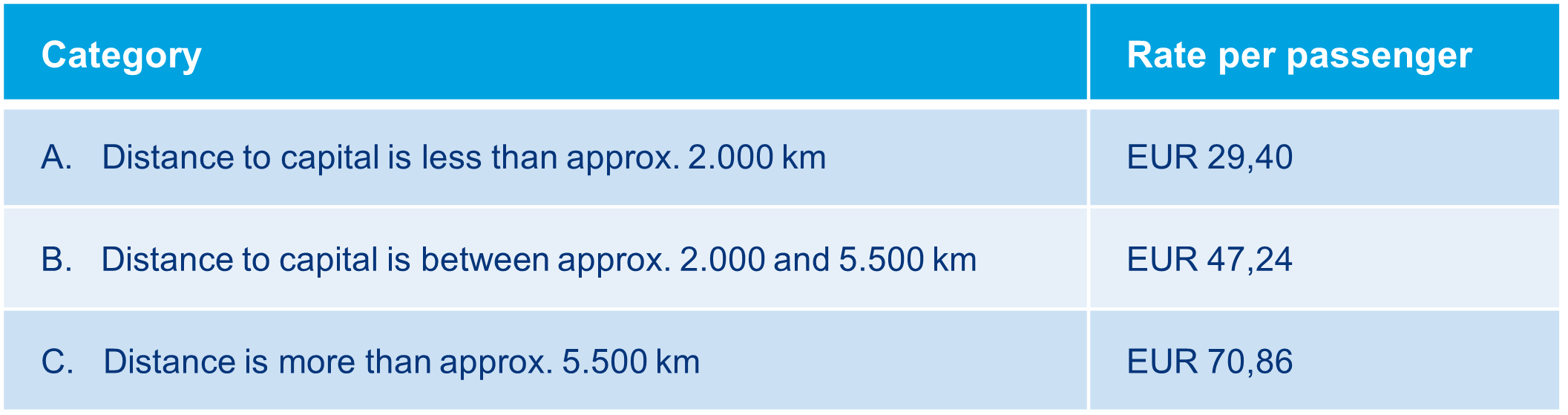

Flight tax

Currently, a fixed flight tax of EUR 29,40 per passenger that departs from the Netherlands applies (transfer passengers excluded). It is proposed to differentiate the rate per distance class as of 1 January 2027. The rates will apply per destination country (i.e., disregarding the actual flight distance), and are based on three categories that are determined based on the distance between Amsterdam and the destination country’s capital:

The law will include an exhaustive list of countries falling into category A or B. If the country is not included on the list, or if the destination country is unknown, category C will apply.

For the Caribbean countries of the Kingdom of the Netherlands, the lower rate of category A will remain applicable. Transfer passengers will also remain exempt.

Waste tax

The Dutch government initially agreed to introduce a “circular plastic levy” by 2027. However, due to expected leakage effects, it became evident that the budgetary objective could not be achieved and would only provide for a limited stimulus to the circular economy. As a result, the government decided not to introduce the plastic levy.

To cover the budgetary shortfall of EUR 567 million, three alternative measures are now being proposed. First, the waste disposal tax will be amended by abolishing the exemption for sewage sludge. Second, a specific rate will be introduced for the disposal of exempted waste. Third, the general rate of the waste disposal tax will be raised from EUR 39,70 per ton of waste to EUR 90,21 per ton in 2028, eventually reaching a structural rate of EUR 113,81 per ton from 2035 onwards (based on the 2025 price level).

Other announced changes

Certain changes have been announced in the Budget Day proposals without any specific legislative texts being available (yet). These include:

- Expansion of the ETS2 system to include the greenhouse horticulture sector, while simultaneously abolishing the CO2 levy for this sector. The portion of revenues exceeding the part used to offset the abolition of the CO2 levy will be used as additional compensation for the greenhouse horticulture sector.

- The district heating scheme within the energy tax will be revised from 1 January 2026, to ensure that heating companies experiencing a decline in the share of sustainably generated heat (due to a calamity or the improvement of the sustainability of the source of heat) remain eligible for the degressive energy tax rates during a transitional period of up to three years.

Changes as of 1 January 2026 that were introduced last year

We note that there are several changes that will enter into force as of 1 January 2026 that were part of Budget Day 2025. This includes the abolishment of the netting rule (“salderingsregeling”) and the introduction of a specific energy tax rate for hydrogen. We refer to our Budget Day Post of last year.