Facts

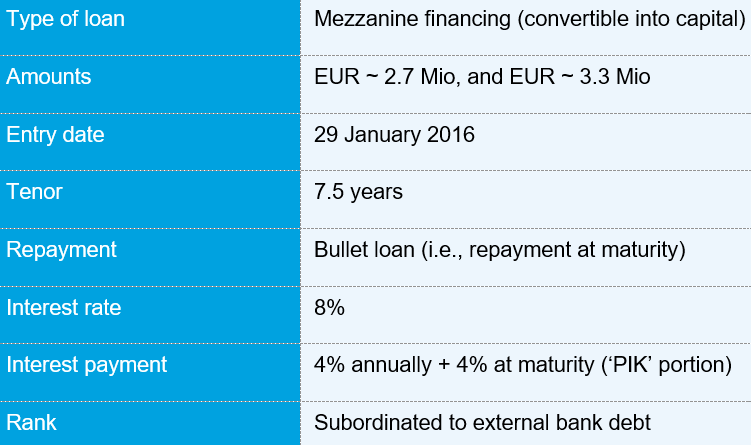

In the frame of a private equity transaction in 2016, a company (the Taxpayer) received two shareholder loans (one from an individual, another from a company) to finance the acquisition of a participation in another related company. The terms and conditions of the shareholder loans are summarized in the table below.

The 8% interest rate on the shareholder loans was determined with reference to a third-party offer made in the same period. Next to this, the Taxpayer justified the applied interest rate during the audit based on (i) a refinancing offer from a third-party received in 2021 at a rate of 9.75% and (ii) a 2015 master thesis from the University of Gent concluding that the market remuneration for mezzanine financing lies between 13% and 25%.

The Tax Administration took the view that the interest paid in 2016 and 2017 at a rate of 8% was not “at arm’s length”. Based on three methods (an internal CUP, and two searches for external CUPs in the TP Catalyst and Bloomberg databases respectively) the administration determined that the market interest rate should be no higher than 3.325%. Hence, the portion of the interest in excess of 3.325% was deemed non-deductible.

The Taxpayer brought a judicial appeal before the Court of First Instance of Leuven.

Court considerations

The interest rate applied by the Taxpayer is not at arm’s length

The Court did not accept the arguments put forward by the Taxpayer to justify the arm’s length character of the 8% interest rate:

- The Court considered that the third-party offer from 2016 was not made by an independent party. The Court’s finding is based upon the fact that the third-party made a financing offer in the framework of broader commercial negotiations for the acquisition of the related company. Hence, the Court considers that the financing offer from the third-party may have been made solely to justify a high interest rate on the shareholder loans. The circumstance that the third-party never became a shareholder does not change the Court’s view.

- The Court further rejects the comparability of the third-party offer received in 2021 with the original shareholder loans. The Court’s position in this respect is based on the evolution of the creditworthiness of the borrower in the five-year timeframe between the original shareholder loans and the third-party offer. The Court’s high-level analysis was based upon financial ratios (leverage ratio, assets to debt, return on investment, asset turnover and interest coverage) which were all worse in 2021 than in 2016. In addition, the Court found that the third-party offer did not contain a detailed calculation of the offered interest rate of 9.75%, which, according to the Court, made it impossible to rely on comparability adjustments to resolve comparability issues.

- Regarding the 2015 master thesis, the Court considered that the data contained in the thesis could not be relied upon as it was too broad and not verifiable.

The interest rate determined by the tax administration is at arm’s length

Out of the three methods used by the tax administration, two were deemed acceptable by the Court.

The Court first accepted the use of an internal CUP (a bank loan with similar characteristics to the shareholder loans) which was adjusted by the tax administration to account for the subordinated character of the shareholder loans.

The Court also accepted the use of external CUPs from the Bloomberg database where the search criteria included a notched-down credit rating to account for the subordinated character of the shareholder loans.

However, the Court did not accept external CUPs from the TP Catalyst database, which may be because the comparables found on the database were all located in the US.

Decision

The Court rejected the appeal of the Taxpayer, thus upholding the position of the Tax Administration regarding the non-deductibility of the portion of the interest in excess of the arm’s length remuneration for the shareholder loans.

Takeaways

Financial transactions have been on the radar of the Tax Administration for some time now. Although the OECD recently issued specific guidance incorporated in Chapter X of the OECD Transfer Pricing Guidelines, there is still very few case law on how to apply the arm’s length principle to intragroup financing in practice. Therefore, notwithstanding some unclear aspects regarding the facts of the case and regardless of the criticism made by practitioners on some of the Court’s reasoning, the case offers insight on the approach of the Tax Administration and Courts when it comes to the transfer pricing aspects of intra-group loans. Below are our observations and take-aways:

- The burden of proof in transfer pricing lies on the Belgian Tax Administration and is twofold: the Tax Administration should demonstrate that (i) the method applied by the Taxpayer does not lead to an arm’s length outcome (based on a specific analysis of the case at hand), and (ii) another method providing another price is appropriate. When the price applied by the Taxpayer is however mainly justified based on an ex post analysis in the framework of discussions with the Tax Administration, it appears that Courts take a more strict position when evaluating such ex post evidence in comparison with cases where the price is set based on an ex ante transfer pricing analysis. Therefore, it is highly advisable that transfer pricing documentation be prepared before entering a financial transaction, as justifying the arm’s length nature of a transaction ex post may prove more difficult;

- As recognized by the Court, using multiple transfer pricing methods to corroborate benchmark results may prove useful when faced with transactions containing clauses that are difficult to price (e.g., the conversion into equity option for mezzanine financing);

- Transfer Pricing is not only relevant in a traditional MNE context but also in a private equity & investment structuring context;

- Databases referencing debt instruments such as Bloomberg may be used to search for external CUPs even for financial transactions that have equity-like characteristics (e.g., highly subordinated mezzanine financing);

- “Offers to lend” as CUPs might not be accepted by the Tax Administration and Courts given that such offers do not represent actual transactions. The OECD Guidelines take in a similar position with respect to bank opinions which are generally considered not to reflect reliable CUPs. They further take in a strict interpretation of the notion of “independent transaction”, requiring an assessment of the wider context of the transaction (in this case, by rejecting an offer which was made in the context of wider negotiations, without any indication that the latter may have actually influenced the price);

- Comparability adjustments to account for subordination and the bullet character justifying a higher premium might be accepted by the Tax Administration. Specifically, as regards subordination, the Court refers to a credit rating adjustment of 1-2 notches in line with rating agencies guidance. On the other hand, the Court considers that in the specific context of a shareholder loan, one should not account for the absence of security (as the shareholder already has access to the subsidiary’s assets);

- A debt capacity and a credit risk analysis can be performed based on financial ratios.

It is stated in doctrine that the Taxpayer will appeal to the Court ruling. We will follow-up on this and report on subsequent developments.

Should you require any assistance in the field of transfer pricing, please contact us below.