In our previous article, we reported on the leaked draft of the revised Sustainable Finance Disclosure Regulation (SFDR) – commonly referred to as SFDR 2.0 – and signalled a significant overhaul of the EU’s sustainable finance framework. Now, with the European Commission’s (EC) final proposal published on 20 November 2025, we have a definitive blueprint for SFDR 2.0. While the final proposal builds on the leaked draft, it introduces several substantive changes; not to the benefit of the industry compared to the leaked draft.

From leaked draft to final proposal, the key changes

The final proposal of 20 November 2025 largely confirms the strategic direction set. The key changes compared to the leaked draft include:

Removal of the AIF professional investor carve-out

The leaked draft allowed AIFs marketed exclusively to professional investors to opt out of the SFDR regime. The final proposal does not include this carve-out. As a result, all AIFs marketed in the EU – regardless of investor type – must comply with the new categorisation rules or adhere to the restrictions applicable to non-sustainability products (Article 6a). The removal of the opt-out introduces new challenges for fund managers only targeting professional investors. More specific, the restrictions that Article 6a would impose on the content of marketing communications make it challenging for a fund manager to explore and develop any sustainability features for that fund. This is a missed opportunity to cater for the possibility to tailor funds to professional investor needs.

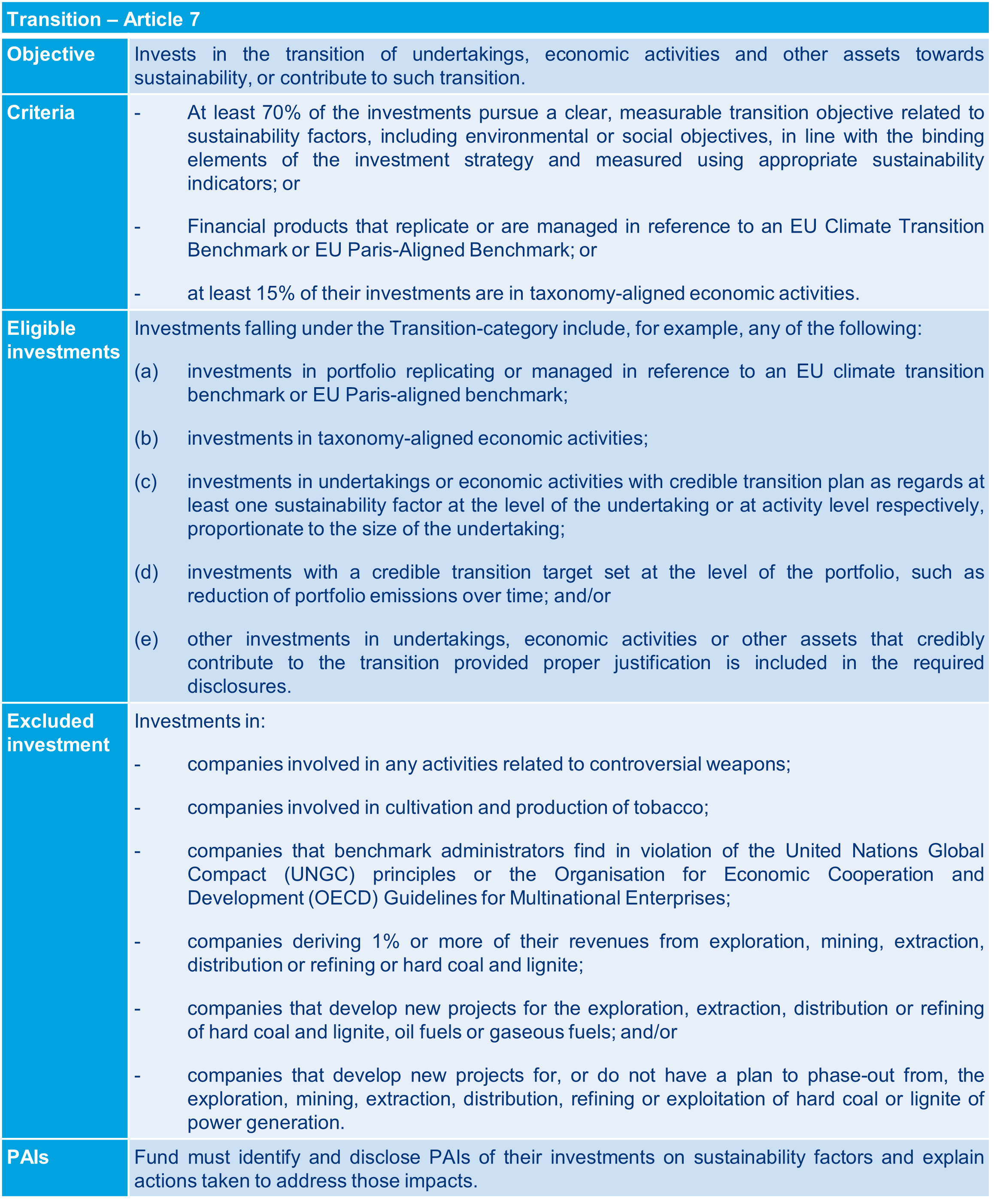

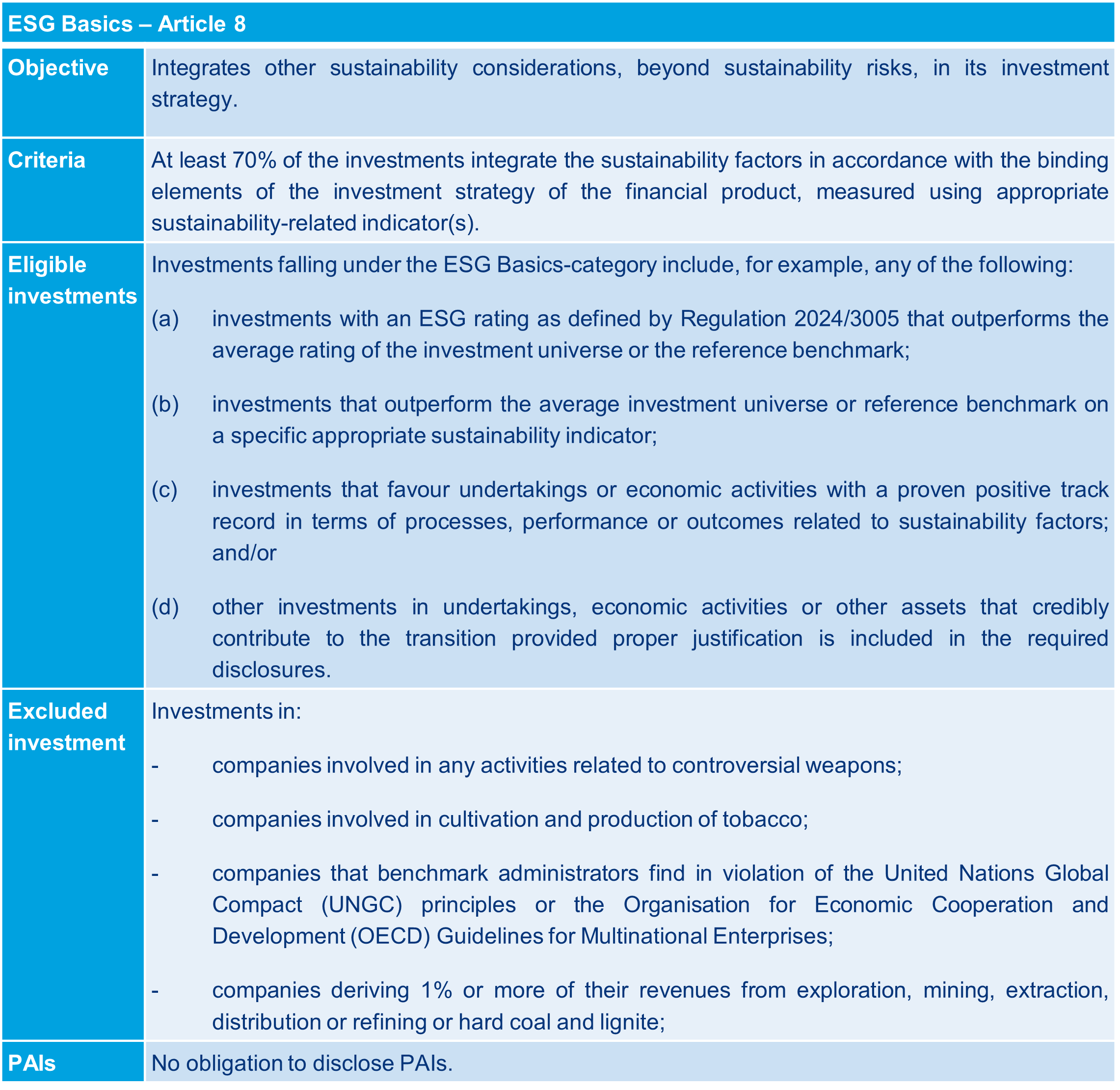

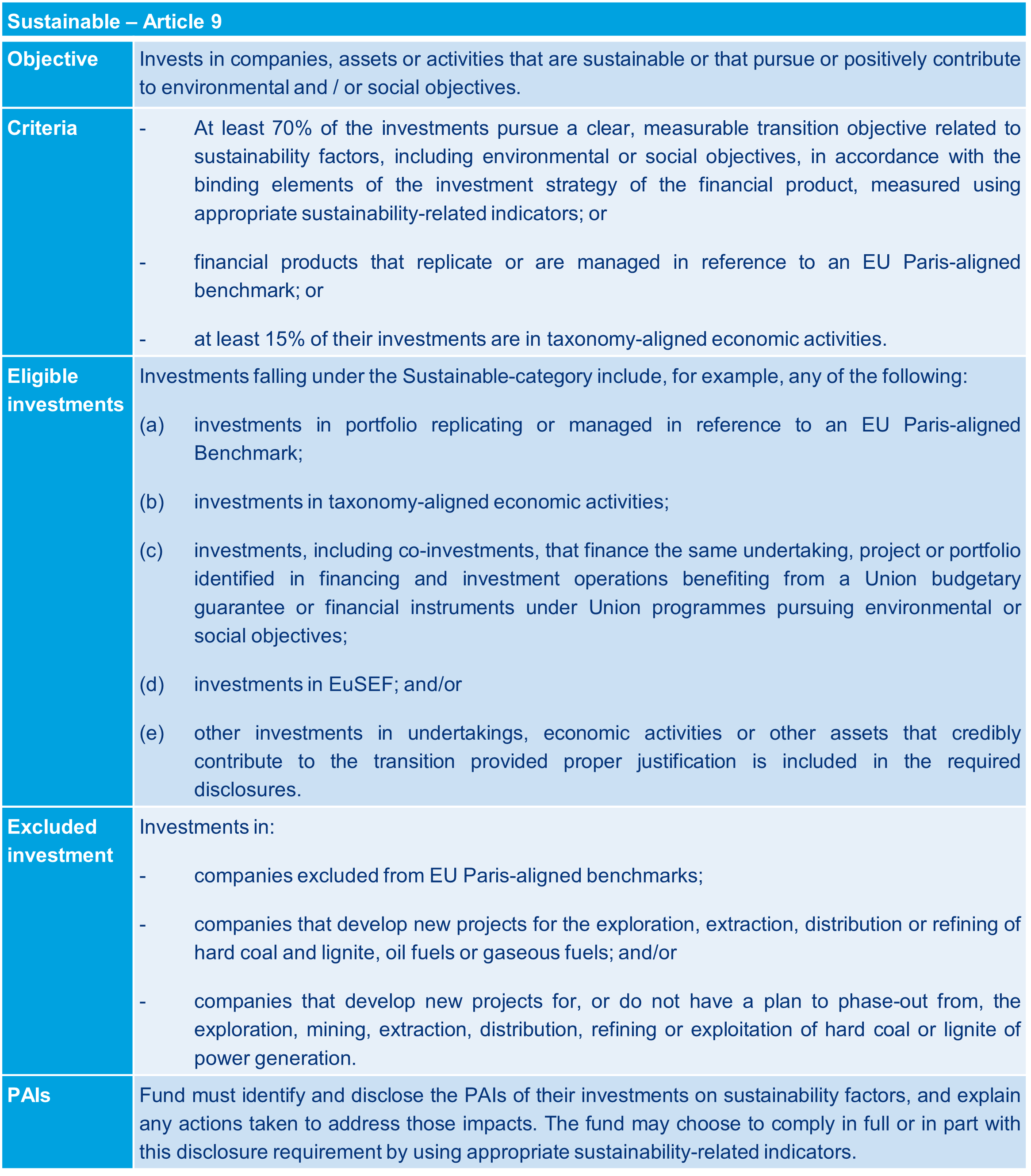

Formalisation of product category names

The final proposal establishes three categories: Transition, ESG Basics, and Sustainable. While the leaked draft anticipated similar categories, it left naming and certain criteria to future delegated acts. The final proposal now provides clarity and legal certainty on the names for these three categories.

Expanded fossil fuel exclusions

All three categories now prohibit investments in companies deriving 1% or more of revenues from hard coal or lignite. In the leaked draft, this restriction applied only to the Sustainable category (Article 9).

Principal Adverse Impact disclosures reinstated

The final proposal reinstates the mandatory disclosure of Principal Adverse Impact (PAIs) for both Transition (Article 7) and Sustainable (Article 9) products. Fund managers must identify PAIs on sustainability factors and describe mitigating measures. Although the requirements seem more flexible than the current regime (which requires "consideration" of selected PAIs), the reinstatement of the PAI disclosures is a big shift from the leaked draft in which PAI disclosures were abolished.

Changes to permitted investments and exclusions

Transition Products (Article 7): Investments based on a credible engagement strategy are permitted for the Transition Product category, to the extent they are linked to another eligible investment type. The final proposal clarifies that these transition plans or targets must align with the Paris Agreement and the EU climate neutrality framework and are prohibited from investing in companies developing new coal, oil, or gas projects or those lacking a phase-out plan for coal or lignite in power generation.

Sustainable Products: Permitted investments now include European social entrepreneurship funds (EuSEFs). The final proposal also clarifies that investments may target undertakings, projects, or portfolios benefiting from EU guarantees or issuance programs with environmental or social objectives – even if the investment itself does not directly participate in those programs.

Clarification of the combination category (Article 9a)

The combination category is designed for funds that combine two or more Article 7, 8 or 9 products. For example fund-of-funds. The leaked draft text did not provide any further details about the criteria for qualifying as an Article 9a fund. The final proposal now clarifies that these funds must meet a 70% investment threshold in eligible underlying products and comply with all relevant exclusions, to qualify as an Article 9a product. Fund managers may rely on disclosures from underlying products to establish this.

Clarification on EU Taxonomy reporting

The leaked draft created uncertainty by remaining silent on whether Taxonomy alignment disclosures would remain in force. The final proposal confirms that Taxonomy-related disclosures remain in force, but only for products pursuing an environmental objective (i.e. Article 7 and 9 products). ESG Basic products (Article 8) are exempt. Reporting is streamlined through simplified templates (maximum two pages) and removal of detailed website disclosures, although fund managers must still provide supplementary information upon request.

Further clarification on Article 6a

Article 6a will govern how non-categorised products may reference sustainability factors. The leaked draft already introduced the following restrictions in this respect:

- No reference to sustainability factors in the name or marketing materials of the financial product;

- No reference to sustainability factors in the KIID of the financial product;

- Not permitted to make a claim which would trigger Article 7, 8 or 9 status (i.e. cannot claim that the fund has transition objectives, integrates sustainability, has sustainability objectives, or has impact objectives).

It is permitted to include information on whether and how the product considers sustainability factors in the pre-contractual disclosures for the fund provided that it is not a “central element” of the pre-contractual disclosure. "Not a central element" means it is neutral and limited to less than 10% of all information on the product’s investment strategy.

The final proposal retains these above restrictions but introduces two changes:

- If sustainability information appears in pre-contractual documents, it must also be included – under the same constraints – in periodic reports.

- The reference to sustainability risks has been deleted in the final proposal, meaning that a fund manager could disclose information about sustainability-related risks in its pre-contractual documentation.

Elements that remain unchanged

Despite the key changes above, several elements of the leaked draft have remained unchanged in the final proposal, the most important being:

- Entity-level PAI disclosures: The deletion of entity-level disclosures under Articles 4 and 5 of SFDR remains unchanged. Fund managers will no longer be required to publish statements on the consideration of PAIs at entity level or to disclose remuneration policies in relation to sustainability risk integration. This is an important change from the current entity and product level PAI disclosure model towards a product level PAI disclosure regime only.

- Scope of SFDR 2.0: The scope continues to exclude portfolio management and investment advice on the basis that firms providing these types of services do not manufacture or manage the underlying sustainable products. This means that separately managed accounts and funds-of-one will generally fall outside SFDR 2.0, unless structured as AIFs or UCITS.

The new product categories

The main aspect of SFDR 2.0 is the new product categories, each with distinct criteria, exclusions, and disclosure requirements:

In addition to the three product categories mentioned above, SFDR 2.0 introduces two additional “categories”:

- Combination – Article 9a: Financial Products combining two or more categorised products (e.g., fund-of-funds).

- Sustainability-related financial product with impact – Article 7 or 9: Financial Products under Article 7 or 9 with a pre-defined, measurable social or environmental impact objective.

What happens to existing Article 8 and 9 funds?

Closed-ended funds that are fully raised

The final proposal provides a pragmatic exemption for closed-ended funds that are fully raised and no longer marketed at the time SFDR 2.0 enters into force. Fund managers may elect to disapply the new regime to these funds, effectively terminating all SFDR related obligations, subject to any ongoing contractual commitments with investors. This approach minimizes disruption to legacy products, where investor protection concerns are less acute.

Other funds: Absence of transitional relief

For all other funds, the final proposal is less accommodating. There is no transitional relief for open-ended funds or for closed-ended funds that are not fully raised when SFDR 2.0 becomes applicable. Managers of these products will be required to comply with the revised categorisation and disclosure regime as of the effective date.

Next steps

The final proposal is now subject to the ordinary EU law process. The Commission's proposals have been submitted to the Council of the EU and the European Parliament for scrutiny. The three of them will then hold trilogue negotiations in order to reach agreement on a final text. The agreed text will then be published in the Official Journal and will take effect 18 months thereafter. SFDR 2.0 will thus likely enter into force by 2027 or 2028.

Although SFDR 2.0 is still several years away, fund managers should make an impact assessment. This will be particularly important for current (or proposed) funds falling under the current Article 8/9 regime, to work out where they will sit in the proposed Article 7/8/9 categorisation regime.

Contact

Should you require any assistance with assessing the impact of SFDR 2.0, we are here to support you. Please contact your trusted adviser at Loyens & Loeff or one of our colleagues mentioned below.