1. Background: "ELTIF 1.0" – A Failed "All-Purpose" Alternative Investment Fund Vehicle

ELTIF 1.0 entered into force on 19 May 2015 with the Europe 2020 strategy in mind that saw long-term finance as a crucial enabling tool for putting the European economy on a path of smart, sustainable and inclusive growth with high employment, and competitiveness for building tomorrow’s economy in a way that is less prone to systemic risks and is more resilient.

To attain that objective, ELTIF 1.0 had been designed as an “optional specialist regime" for authorized alternative investment fund managers (AIFMs) to boost European long-term investments in the real economy. To that end, ELTIF 1.0 restricted the “ELTIF label" to EU-based alternative investment funds (AIFs) managed by authorized AIFMs. ELTIFs had been introduced as a “regulated fund product" that had to be authorized by its home state regulator and not merely registered, as is customary in the Netherlands for (unregulated) types of AIFs that are subject to supervision through their AIFM and restricted to professional investors only.

The post-global financial crisis EU regulatory objective of boosting “long-term investments" led to a ELTIF 1.0 regime that was heavily regulated in terms of, amongst others, eligible investments, diversification, concentration requirements, as well as the use of borrowing and financial derivative instruments. The ELTIF 1.0 regime applied to both professional and retail investors (in practice, rather high-net-worth individuals [HNWI]) equally. In particular, as ELTIF 1.0 also introduced a marketing passport for HNWIs, provided that a number of heavy “retail top-up restrictions" were met.

Albeit receiving a lot of attention, especially given the introduction of the “HNWI marketing passport", it became clear, over time, that the ELTIF regulation did not scale up as expected.

As per October 2021, only 57 ELTIFs had been launched with a mere EUR 2.4 billion raised and ELTIFs had for the largest part only been domiciled in four Member States (Luxembourg, France, Italy and Spain). This is extremely low. For example, the Luxembourg Reserved Alternative Investment Fund (RAIFs) had seen 1686 RAIFs being established between its launch in 2016, one year later than ELTIF 1.0, and January 2022 (read more in Luxembourg for Finance).

Article 37 ELTIF 1.0 included a review clause which required the European Commission to review ELTIF 1.0. Based on the evaluation of the functioning of ELTIF 1.0 and stakeholder feedback, the advantages of ELTIFs had been identified as being diminished by the restrictive fund rules (e.g. eligible investments, diversification and concentration rules) and barriers to entry for retail investors, the combined effect of which reduced the utility, effectiveness and attractiveness of the ELTIF 1.0 legal framework for managers and investors. These restrictions were seen as the key drivers of the ELTIFs’ failure to scale up significantly and reach their full potential to channel investments to the real economy.

This contribution continues to discuss ELTIF 2.0. Section 2 discusses how the main shortcomings of ELTIF 1.0 have been addressed. For that purpose, it discusses, amongst others, changes with respect to the scope of eligible investment assets, portfolio composition, diversification and concentration rules, as well as liquidity options and the removal of retail investor barriers. Whilst discussing these topics, it also highlights the opportunities that ELTIF 2.0 presents. Section 3 discusses the challenges ahead of ELTIF 2.0, including possible changes under AIFMD 2, the RISD and interpretations of the European Securities Markets Authority (ESMA) that is requested to develop regulatory technical standards (RTS) that may potentially prevent ELTIF 2.0 from becoming a success. It continues to explain that in the Netherlands European venture capital funds (EuVECAs) may, in some instances, be a “competing product" to the ELTIF. Section 4 concludes by noting that ELTIFs are primarily a retail vehicle.

2. ELTIF 2.0 – Gateway to Heaven?

Further to the initial ELTIF 1.0 review, a number of shortcomings have been identified that have been addressed in ELTIF 2.0 to serve as an impetus for its use. The key changes introduced by ELTIF 2.0 will be discussed in this section.

2.1. Broader Scope of Eligible Investment Assets

ELTIF 2.0 significantly widens the scope of eligible investment assets.

2.1.1. Abolishment “EU" Location Requirement Eligible Assets

ELTIF 1.0 provided that ELTIFs mainly had to be channelled to European long-term investments. It was the practice of the CSSF (the Luxembourg regulator) to permit ELTIFs to invest up to 50% of their portfolio in non-European assets.

ELTIF 2.0 no longer includes the reference to European long-term projects to strengthen the broader scope of eligible assets, which do not necessarily need to be located in the EU and explicitly allow (a majority of) eligible assets and investments to be located in third countries. Practitioners taking a liberal view argue that promoters may under ELTIF 2.0 pursue a global investment strategy. Critics, however, argue that, by absence of specific criteria, national competent authorities may still impose restrictions in this respect. What is, however, clear is that, where ELTIF invest in qualifying portfolio undertakings that are located in a third country, such country may not be included in the list of noncooperative jurisdictions for tax purposes or be identified as per delegated acts of Directive 2015/849, as amended (AMLD IV).

2.1.2. Revised “Real Asset" Definition

Under ELTIF 2.0, the definition of “real asset" is revised. Till date, the scope of this definition is vague. The revised definition captures any asset that has intrinsic value due to its substance and properties. The purpose of this revision is to broaden the scope of the real asset investment strategies that ELTIF managers can pursue. Such real assets may but do not necessarily need to provide cash flows or investment returns, such as communication, environment, energy or transport infrastructure, as well as education, health, welfare support or industrial facilities or installations. The simplified definition of “real assets" also ensures that the broader scope of assets may include those assets that cannot be easily quantified. These are, for instance, assets that are evaluated based on a discounted cash flow or comparison valuation method. Furthermore, ELTIF 2.0 abolishes the minimum investment threshold of EUR 10M and it is also no longer required that real assets are owned directly or via “indirect holding via qualifying portfolio undertakings".

The revised “real asset" definition and the abolishment of the EUR 10M threshold contribute to flexibility for ELTIF managers and allow for a larger portfolio of individual real assets that is more diversified and enables investments by ELTIFs in asset classes of which the value decreases over the time of its life span (e.g. assets in the renewable energy space).

2.1.3. STS Securitizations & EU Green Bonds

To extend the scope of eligible assets and promote the investments of ELTIFs in securitized assets, ELTIF 2.0 introduces four categories of securitizations with a “STS-label" under Regulation (EU) 2017/2402, as amended (STSR) as eligible investments for ELTIFs. These include residential mortgage-backed securities, commercials loans backed by mortgages on commercial immovable property, corporate loans and trade receivables or other underlying exposures, provided that the proceeds are used for (re)financing long-term investments. In line with the EU’s contemporary policy to encourage private capital flows towards more environmentally sustainable investments, ELTIFs are now also allowed to invest in green bonds that are issued by “qualifying portfolio undertakings" under the EU legislation on environmentally sustainable bonds.

These provisions broaden the size and scope of eligible assets for ELTIFs, and make the ELTIF regulatory framework more appealing for both asset managers and investors.

2.1.4. Fund-of-Funds & Master-Feeder Structures

In the past two years, a number of retail feeder/fund-of-funds (FoF) AIFs have been launched in Luxembourg that are bundling commitments of HNWIs and invest them in one or more “best of class'' private market funds. Until now, ELTIF FoF strategies were, in practice, almost impossible to be structured and one ELTIF had to be set up for each fund. However, ELTIF 2.0 now introduces the possibility for ELTIFs to pursue FoF investment strategies and to grant indirect exposure to AIFs reserved to professional investors managed by the same or other AIFM(s). To that end, ELTIFs are, in addition to ELTIFs, EuVECAs and European social entrepreneurship funds (EuSEFs), also allowed to invest in EU AIFs managed by EU AIFMs, provided those ELTIFs, EuVECAs, EuSEFs¸ undertakings for collective investment in transferable securities (UCITS) and EU AIFs invest in eligible investments and have not themselves invested more than 10% of their capital in any other collective investment undertaking (Eligible CIU). FoF ELTIFs, thus, have to perform a “look-through approach", by combining the assets directly held by the ELTIF with the assets by these EU AIFs that are eligible to be ELTIF core assets. This “look-through approach" also includes the later to be discussed diversification requirements and the borrowing limits made in respect of the target funds. The “look-through" should be done on a quarterly basis. This approach is, however, not required for the purpose of compliance with the concentration limits.

Furthermore, ELTIF 2.0 allows ELTIFs to make use of master-feeder structures. However, such structures are restricted to “master ELTIFs", i.e. an ELTIF or sub-fund thereof, in which another (feeder) ELTIF invests at least 85% of its assets in units or shares, only and have to comply with a number of additional requirements with respect to, amongst others, the ELTIF authorization procedure and information to be provided in the prospectus.

From a regulatory standpoint, a few missed opportunities have already been identified, such as the possibility for FoF ELTIFs and master-feeder ELTIFs to invest in non-EU AIFs or to have masterfeeder structures that are not ELTIFs.

2.2. Qualifying Portfolio Undertakings

ELTIF 2.0 raises the market capitalization cap for listed “qualifying portfolio undertakings" from EUR 500 million to EUR 1.5 billion. The reason for this is that many listed companies with a low market capitalization have limited liquidity which prevents ELTIF managers from building, within a reasonable time, a sufficient position in such listed companies and narrows down the range of available investment targets. The revised definition, thus, provides ELTIFs with a better liquidity profile.

ELTIF 2.0 also allows investments in “FinTechs", i.e. financial undertakings, other than financial holding companies or mixed-activity holding companies, that have been authorized or registered more recently than 5 years before the date of investment.

2.3. Co-investments

Currently, ELTIFs may only invest in assets that are unrelated to the manager of the ELTIF, unless the ELTIF invests in units or shares of other Eligible CIUs that are managed by the manager of the ELTIF. Furthermore, it is not allowed that the staff of the ELTIF manager and of undertakings that belong to the same group of the ELTIF manager invests in that ELTIF or to co-invest with the ELTIF in the same asset. ELTIF 2.0 amends this. First, ELTIFs may invest in not only units or shares of other ELTIFs, EuSEFs or EuVECAs, but also of other UCITS or EU AIFs it manages. Second, ELTIF 2.0 explicitly allows (minority) co-investments by the manager and its affiliated entities that belong to the same group with that ELTIF manager, and their staff only in so far as the ELTIF manager has put in place organizational and administrative arrangements to identify, prevent, manage and monitor conflicts of interest and provided that such conflicts of interest are adequately disclosed.

2.4. Portfolio Composition & Diversification

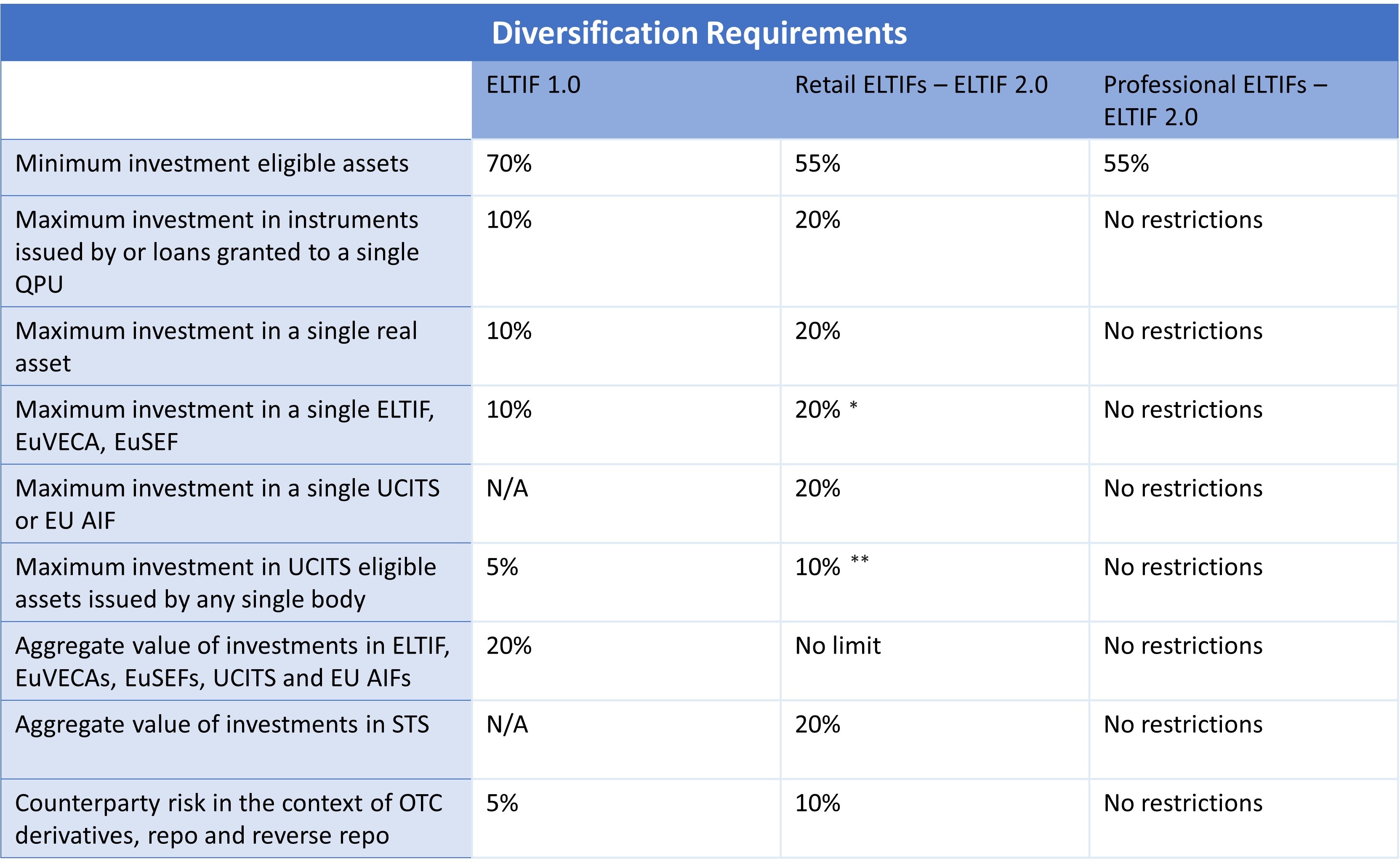

ELTIF 2.0 lowers the threshold for eligible investment assets of ELTIFs from 70% to 55%. The lowering of this threshold is designed to improve the liquidity profile of ELTIFs’ underlying portfolios and promote the flexibility of asset managers in using liquidity pockets consisting of liquid (UCITS) assets when executing their investment strategies. Critics argue that ELTIFs can now be structured that contain a high degree of “UCITS assets" at a higher cost.

Based upon: PwC, An (almost) comprehensive guide to the new ELTIF regulation

* Not applicable to ELTIFs that are structured as a feeder ELTIF.

** Lifted to 25% in some instanced, e.g. if they are issued by a Member State

Under ELTIF 2.0, the portfolio composition and diversification requirements do not longer apply if an ELTIF (or a compartment thereof) is solely marketed to professional investors. For retail investors, including HNWIs, these, however, remain to be in place. They are, however, made more flexible. ELTIF 2.0 increases the maximum retail ELTIF exposures to instruments issued by, or loans granted to, any single qualifying portfolio undertaking from 10% to 20%. The same threshold of 20% is being applied to single real assets and eligible “STS securitizations". Furthermore, the 20% threshold has also been established for “Eligible CIUs". For eligible assets under Directive 2009/65/EC, as amended (UCITSD), the threshold has been doubled to 10% per “single body".

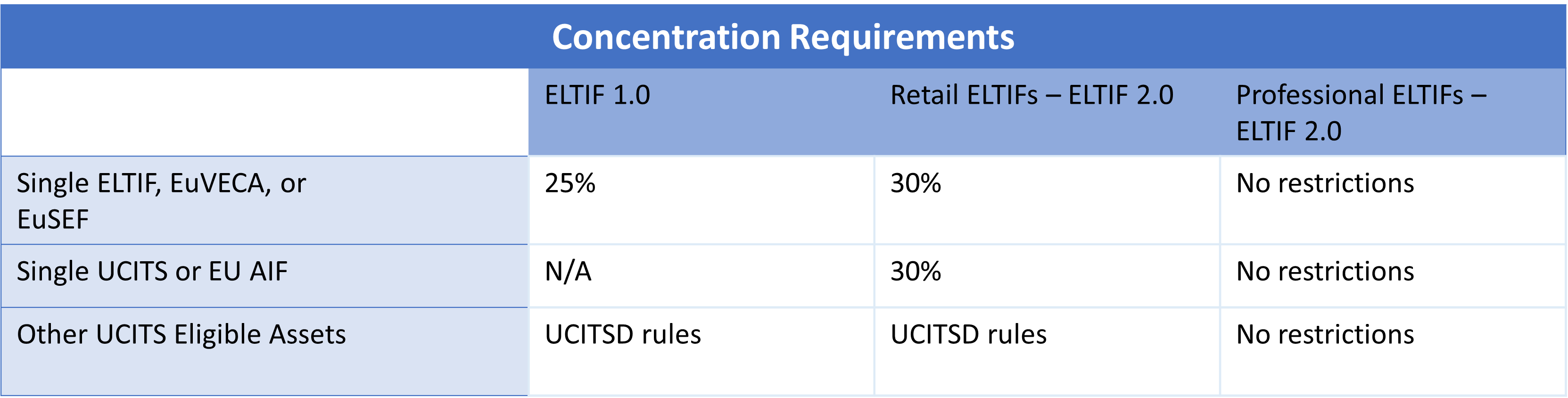

2.5. Concentration Rules

Under Article 15 ELTIF 2.0, an ELTIF may not acquire more than 30% (previously: 25%) of the units or shares of a single “Eligible CIU". Again, this concentration limit does not apply to “professional ELTIFs" nor to feeder ELTIFs, as feeder ELTIFs are allowed to invest, at least, 85% of their assets in units/shares of another ELTIF or sub-fund of an ELTIF.

Based upon: PwC ELTIF Report

2.6. Borrowing of cash

ELTIF 2.0 enables retail ELTIFs to increase their borrowing of cash up to 50% of the ELTIF’s NAV. By contrast, professional ELTIFs are permitted to leverage up to 100% of the NAV of the ELTIF, thereby making certain investment strategies, such as real estate and infrastructure, more interesting. ELTIF 2.0 also seeks to provide additional flexibility in the currency-related rules and extends the possibility of ELTIFs to contract in a currency other than the base currency. Furthermore, it is now also possible to borrow, not only for investment purposes (i.e., loans are not excluded anymore), but also for the purpose of providing liquidity and to pay costs and expenses. It has eventually been provided that encumbrance of assets can be done in that context and the 30% limit in this respect has been removed. Lastly, a clarification is included in ELTIF 2.0 that those borrowing arrangements fully covered by investors’ capital commitments would not be considered to constitute borrowing.

2.7. Liquidity options: Open-end ELTIFs, “Liquidity Windows" & Listings

Contrary to the British Long Term Asset Fund (LTAF), ELTIFs can only be structured as limited-duration funds and, therefore, they cannot be “true" evergreen funds (i.e, funds with an unlimited duration). However, some ELTIFs structured under ELTIF 1.0 have been authorized in Luxembourg with a limited duration of 99 years. ELTIFs may also allow for redemptions under certain conditions. Therefore, ELTIFs can be, de facto, structured as open-ended “evergreen funds". In this respect, ELTIF 2.0 has eased the “redemption regime" for ELTIFs. So far, investors were mandatorily locked-up until the end of the ELTIF ramp-up period. Under ELTIF 2.0, the lock-up may be decoupled from the ramp-up period. Furthermore, investors may under ELTIF 2.0 not request the winding down of an ELTIF anymore if their redemptions requests have not been satisfied within one year. However, ELTIF 2.0 contains a provision in which ESMA is requested to develop RTS that will specify ELTIF redemption policies in more detail. Currently, the Draft RTS published in May 2023 in relation to redemption policies causes uncertainty in the market. While many of the proposed rules are prudent and workable, some refinement would still be helpful. For example, ESMA proposes a three year minimum holding period before any redemptions are permitted, although this is not a hard-and-fast rule and proposed to be subject to a “comply-or-explain" rule. However, if adopted in unamended form, this would cause issues for ELTIFs that are continually fundraising. Similarly, some of the rules on the portion of liquid assets (i.e. the so-called “liquidity pocket") that must be held to meet redemption requests look overly restrictive and may be an unacceptable drag on returns.

For both open- and closed-ended ELTIFs, ELTIF 2.0 provides for a mechanism to allow investors to dispose of their shares in a ELTIF before the end of the fund’s life on a “matched" secondary market basis to promote the secondary trading of ELTIF units/shares. Although ESMA published its Draft RTS with respect to the mechanism, ESMA admits that the mechanism is new and that it is not yet entirely clear how this mechanism would work in practice.

Lastly, it is also possible to improve the liquidity for investors through listings on a regulated market or multilateral trading facility (MTF). Depending on the type of listing and whether the ELTIF is a “fully" closed-ended ELTIF or not, the Regulation (EU) 2017/ 1129, as amended (Prospectus Regulation), and Directive 2004/109/EC, as amended (Transparency Directive) requirements will apply to the ELTIF.

2.8. Removal of barriers for Retail ELTIFs

Till date, the marketing to retail investors of ELTIFs was subject to strict requirements and, de facto, made the ELTIF a “HNWI-only" product that was not open to “real retail investors".

Under ELTIF 2.0, performing a suitability test, issuing a suitability statement, as well as complying with the ELTIF 2.0 product governance requirements in line with Directive 2014/59/EU, as amended (MiFID II), are sufficient to market to retail investors. This alignment with MiFID II removes the duplication of suitability tests and collection of information that existed within ELTIF 1.0. In instances where retail investors receive a negative result on the suitability assessment but still wish to proceed with the transaction, the ELTIF manager is permitted to do so provided they obtain the explicit consent of the retail investor.

The requirements to provide “appropriate investment advice", to have a “MiFID II top-up" license in place for AIFMs that directly market to retail investors, the EUR 10,000 initial minimum investment requirement and the 10% cap on a portfolio’s exposure to ELTIFs for investors with a total portfolio smaller than EUR 500,000 have, however, been abolished. In line with Directive (EU) 2019/1160, as amended (CBDD), ELTIF managers are also not required anymore to set up local facilities in each Member State where they intend to market ELTIFs to retail investors. ELTIFs under ELTIF 2.0 have, thus, become a product for all types of professional and retail investors.

2.9. Application and Transitional Phase

ELTIF 2.0 will come into effect on 10 January 2024. In this respect, ELTIF 2.0 provides for a layered transitional regime. Open-ended and closed-ended ELTIFs that are still being marketed are required to comply with ELTIF 2.0 within five years after it has officially entered into force. Closed-ended ELTIFs that do not raise additional capital are not required to comply with the ELTIF 2.0 amendments. Finally, ELTIFs authorized before the date of application may, however, voluntarily chose to comply with ELTIF 2.0, provided that the relevant competent authority is notified thereof.

3. ELTIF 2.0 - Storm in a Teacup?

3.1. ELTIFs – Primarily a Retail Vehicle

From the above, it is clear that ELTIF 2.0 introduces a number of changes that make the ELTIF mainly an attractive regulated European retail AIF product and a competitive alternative for fund products available under national laws.

In the first place, ELTIF 2.0 offers a “real” retail AIF marketing passport that is not merely limited to HNWIs, but available to all types of retail investors. This reduces the need to comply with various sets of national legislation containing specific requirements (the national private placement regimes or NPPRs) or to establish local feeder funds that would be required to be established on a country-by-country basis to comply with those NPPRs.

Furthermore, several barriers for marketing to retail investors are being removed and the widening of eligible investment assets, including the revised real assets and qualifying portfolio undertakings definitions, the introduction of FoF and master-feeder structures also make the ELTIF a more attractive retail AIF vehicle.

Another positive parallel development observed is that certain jurisdictions, such as Italy, provide for tax incentives for ELTIF investors, i.e., an exemption of capital gains tax, under certain conditions, for private individuals holding shares/units of ELTIFs. Other Member States, such as Belgium and Luxembourg, are (planning) to set up some tax beneficial regimes that provide tax neutrality for their ELTIFs.

Leaving future tax treatment developments aside, “professional ELTIFs" may, in some cases, also be of interest. ELTIFs may, for example, be of interest to debt fund managers. Loan-originating ELTIFs have, for example, been used by such managers to originate loans to SMEs in France without breaching local “banking monopoly rules". Furthermore, ELTIFs may also be of interest to insurance companies. Following an amendment to Directive 2009/138/EC, as amended (Solvency II) by Commission Delegated Regulation (EU) 2016/467, ELTIFs can also benefit from the same capital charges as equities traded on regulated markets which is lower than other equities. In practice, this means that insurance undertakings may invest “cheaper" through ELTIFs in certain alternatives as through “plain vanilla" (unregulated) AIFs. Despite of this, ELTIFs are mainly expected to remain a “retail vehicle".

3.2. ELTIF 2.0 is not perfect…after all

Despite these positive developments, ELTIF 2.0 might not necessarily become a huge success for a couple of reasons.

3.2.1. European Obstacles Ahead: AIFMD 2, the RISD & ESMA RTS

On the European level, AIFMD 2, as well as the RISD may in the near future offer a more flexible legal framework for “retail AIFs". Some draft versions of AIFMD 2 that have been circulated in the past year contain an amendment of the definition of “professional investors" that would include, amongst others, HNWIs with a minimum EUR 100K ticket that are self-certified. Although it is, currently, unclear whether, indeed, this definition will be amended, the European Commission recently published the RISD in which it proposes to significantly alter the client classification rules by easing the MiFID II criteria that allow clients to easily “opt-up" as a professional client. The proposed amendments include a reduction of the wealth criterion from EUR 500,000 to EUR 250,000, and the insertion of a possible fourth criterion relating to relevant education or training. The amendments also create the possibility for legal entities to qualify as professional on request by fulfilling certain balance sheet, net turnover and own funds criteria. Given that the MiFID II professional and retail client definitions are linked to the AIFMD professional and retail client definitions, it is, thus, very likely that AIFMD 2 and/or the RISD will, de facto, extend the AIFMD marketing passport to HNWIs. Furthermore, the national frameworks implementing AIFMD 2 do not necessarily require a MiFID II suitability test to be performed to market to HNWIs. AIFMD 2 nor the national frameworks of the biggest European fund jurisdictions (are likely to) contain more stringent requirements than ELTIF 2.0 in terms of, for example, eligible assets, portfolio composition, diversification and concentration requirements, as well as secondary trading mechanisms, liquidity management tools and redemption policies for open-ended AIFs. The same holds true for “classic” pure “professional investor only" AIF vehicles under national legal frameworks that have a way faster “time-to-market" than regulated structures, such as ELTIFs.

In line with this, the AIFMD 2 reform the regime applicable to “loan originating funds" and the potential possibility to passport the “loan origination" activity by AIFMs across the EU could reduce the attractiveness of the ELTIF vehicle for debt fund managers. The reason for this is that such a “lending passport" would be available to regulated and non-regulated AIFs alike. ELTIFs, being a regulated product having to comply with, amongst others, stringent portfolio composition, diversification and concentration requirements, would be put at a disadvantage compared to unregulated AIFs to which comparable restrictions on the product level would not apply.

Furthermore, as discussed above, ELTIF 2.0 contains two important provisions that may affect the success of ELTIF 2.0 in which ESMA is mandated to adopt RTS, namely with respect to liquidity management tools (LMTs) and the “liquidity window" for secondary market trading. If the (Draft) RTS adopted by ESMA are proven to be too much “off market", it is not unlikely that AIFMs may opt to continue to use fund products under national laws that will be offered under existing NPPR. In particular, if an open-ended (retail) ELTIF, the “default-type" of retail ELTIF, will be severally restricted that leaves retail investors without liquidity for a substantial amount of time, the NPPR route with the use of “local vehicles" may be chosen over the use of the ELTIF retail marketing passport.

3.2.2. EuVECA as “Competing Product" & Dutch Goldplating

From a pure Dutch perspective, the ELTIF is not likely to gain a lot of traction for a variety of reasons. In the first place, the Netherlands has many subthreshold AIFMs and the ELTIF is limited to authorized AIFMs only. For sub-threshold AIFMs, indeed, the EuVECA label has proven to be quite successful in the Netherlands. Managers that are registered under the Regulation (EU) 345/2013, as amended (Eu-VECA regulation) already have a marketing passport through which they can directly/indirectly market their products to semi-professional investors on a cross-border basis in the EU. Sub-threshold AIFMs have proven to be able to successfully do this without having the need to use complex (and heavily regulated) distribution networks.

Indeed, the ELTIF label allows for more investment strategies than the EuVECA label. However, Dutch fund promoters wiling to use the ELTIF label likely will want to have a “tested" regulated product that is commercially accepted by both retail investors and distributors throughout Europe, such as the Part II UCI in Luxembourg. The Dutch regulator also has limited experience with ELTIFs and, therefore, it is currently not to be anticipated by fund promoters how efficient the product approval for ELTIFs will be in the Netherlands.

Lastly, the so-called “Dutch AIFMD retail top-up" applies to all types of authorized AIFMs marketing to retail investors with tickets smaller than EUR 100K, including those AIFMs managing ELTIFs. ELTIF 2.0 does not allow for "goldplating". However, so far the Dutch regulator has not made any statement whether these requirements will be disapplied in the ELTIF context.

4. Outlook – ELTIFs as pan-European Retail Product

ELTIF 2.0 is currently attracting a lot of interest from fund promoters as a lot of the growth in AIF investments is to be unlocked from HNWIs in the forthcoming years. In this respect, ELTIF 2.0 also provides retail investors with an opportunity to invest in assets other than UCITS or listed assets, in general, thereby increasing diversification and risk spreading, while at the same time maintaining a sufficient degree of (retail) investor protection.

In short, it can be concluded that fund sponsors who wish to access retail capital will find it much easier to do so under ELTIF 2.0. However, AIFMD 2, RISD, the ESMA RTS with respect to LMTs and the liquidity window, as well as the EuVECA label and “AIFMD retail top-up" may pose challenges for this vehicle to become a success in the Dutch fund landscape.

This article was first published by the Tijdschrift voor Financieel Recht, and the original is available in PDF