Following these agreements concluded with the Netherlands, Germany, Luxembourg and France, Belgian tax authorities recently published an administrative circular 2020/C/81 (dated 17 June 2020) including a ‘FAQ’ that provides more clarity on said agreements and how to interpret them.

COVID-19 agreements with border countries

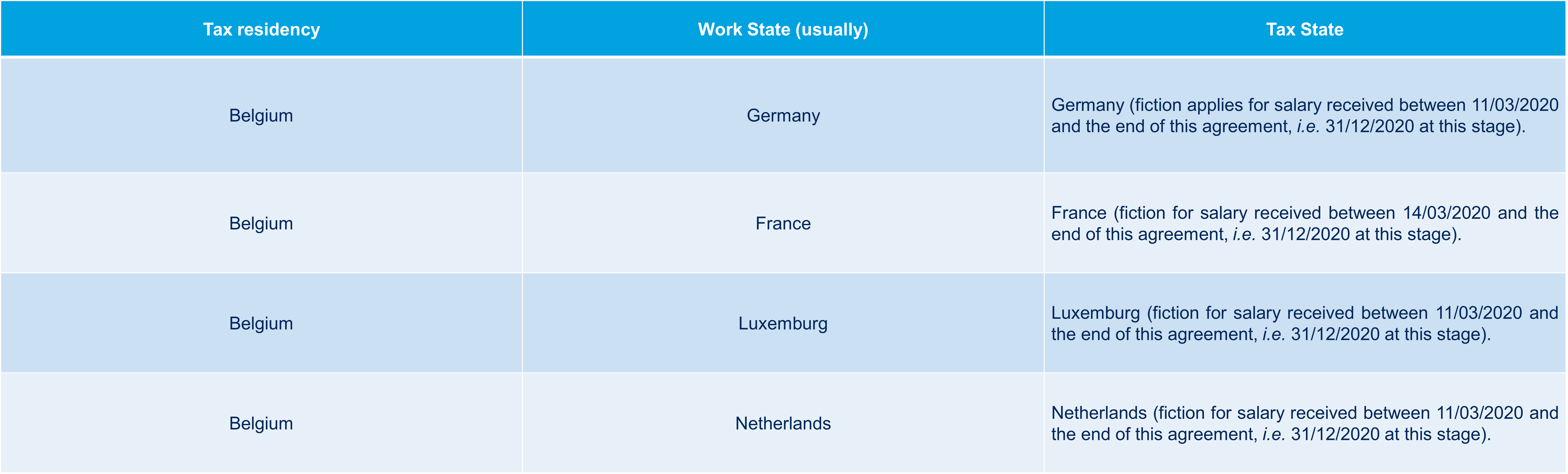

The basic idea behind the agreements as concluded with the Netherlands, Germany, France and Luxembourg lies in the fiction that salaried workers are deemed to have worked in the country where they would normally have worked on the basis of their contractual obligations, despite the fact that due to travel restrictions the employee was working from home.

The table below summarizes the conventional treatment of the incomes of the contemplated employees:

Please note that this fiction

- only applies as long as above said agreements apply. If the employer decides to continue to apply travel restrictions after these agreements have come to an end, normal application of the respective double tax treaties apply again. Hence, a Belgian tax resident working from home, even though he was supposed to work (e.g.) in France, income relating to these days will be taxable in Belgium.

- only applies with respect to the Netherlands, France, Germany and Luxemburg. Hence, with respect to any other country, Belgium will be entitled to tax the income relating to the days worked from home despite travel restrictions due to COVID-19.

- does not apply to self-employed workers (including directors)

- does not apply to secondments.

What if the employment agreement already included homeworking days in Belgium?

Days on which the employee was already allowed to work from home prior to the travel restrictions due to COVID-19 will remain taxable in Belgium (i.e. normal application of the double tax treaty). The other days on which the employee was supposed to work in one of the above countries will remain taxable in one of the respective countries on the basis of above said agreements.

A particularity though exists with respect to Luxemburg.

Insofar the number of working days during which the employee was already allowed to work from home prior to COVID-19 does not exceed 24 days during the calendar year, Luxemburg remains entitled, on the basis of the double tax treaty, to tax the income relating to these days.

What about the frontier regime?

With respect to the frontier worker, days worked from home, i.e. France, are normally considered to be days not worked in the Belgian frontier zone. A frontier worker can only leave the Belgian frontier zone during a limited period of time to avoid the non-application of the frontier regime. Due to COVID-19 and travel restrictions, it has been decided that a frontier worker can work from home between 14/03/2020 and the end of the agreement (i.e. date yet to be decided) without such days being considered as days performed outside the Belgian frontier zone, hence not triggering the loss of the frontier regime.

Hence, the remuneration remains therefore taxable in France.

Reminder of the formalities to be respected within the framework of the COVID-19 agreements

In order to support the fiction of being taxed in the country were the employee would have been taxed in absence of travel restrictions the Belgian tax authorities require

- a certificate from the employer indicating the days of homeworking linked to the measures taken to combat COVID-19; and

- proof that the corresponding income has been effectively taxed in the other country.

The certificate has to include the following information:

- identification of the employee

- the employee’s position/function

- detail of the homeworking days due to COVID-19 travel restrictions

- if applicable, the number of days the employee was contractually allowed to work from home prior to COVID-19 travel restrictions

- detail of illness days, leave and/or recovery

What about foreign executives benefiting from the special tax status?

Tax authorities stipulate in the FAQ that foreign executives are not covered by the respective double tax treaty and thus neither from the COVID-19 agreements as concluded with the Netherlands, France, Germany and Luxemburg. Hence, no travel, no travel exemption and thus taxable in Belgium.

This position however cannot to our opinion apply to foreign executives that have maintained their tax residence in either, the Netherlands, Germany, France or Luxemburg as they continue to be tax treaty protected and hence also protected by the COVID-19 agreements.

A normal application of the double tax treaty applies for foreign executives that have maintained their residency in any other country.