The legal institution of the trust

The trust is a historically developed legal institution stemming from common law. The settlor transfers certain assets to one or more trustees with the task of managing and using these assets for the benefit of the beneficiaries – this is typically set out in the trust deed.

In contrast to the Swiss foundation, the trust does not have its own legal personality. However, the trust is also not a mere contract. Originally established by the settlor through a unilateral legal act inter vivos or upon death, the trust is at its essence a legal relationship between the trustee(s) and the beneficiaries. The settlor has only limited influence, if any.

Possible areas of use

There are many different types of trusts, with the most common being those used in connection with estate planning and for asset protection purposes. For example, trusts can be used to benefit family members beyond the settlor’s death, to secure alimony payments, or to protect assets from future creditors. Assets can also be pooled in a trust for business investment purposes or to finance investments and transactions. According to the draft bill, the establishment of commercial trusts (with designated beneficiaries) shall be allowed.

Key elements of the proposed Swiss trust

The preliminary draft bill envisages the introduction of the trust as a new legal institution in the Swiss Code of Obligations and is based on existing Swiss principles and rules. The Swiss trust essentially mirrors the trust under Anglo-Saxon law and is consistent with the definition of the Hague Trust Convention.

To avoid undermining the well-established institute of the Swiss foundation, the establishment of charitable trusts and other purpose trusts (i.e., where the assets are not allocated for the benefit of specific persons) shall not be permitted. Further, the time span of a trust is limited to 100 years.

Since the Swiss Financial Institutions Act entered into force, professional trustees are subject to supervision and require a license. The preliminary draft bill outlines comprehensive identification and documentation obligations for trustees to avoid the misuse of trusts for money laundering, terrorist financing or tax evasion.

The taxation of trusts as envisaged in the preliminary draft bill

Currently, there are no specific Swiss tax provisions governing the taxation of foreign trusts. In principle, foreign trusts are taxed in accordance with general Swiss tax principles as well as the two circular letters published by the Swiss tax conference (Circular Letter Nr. 30, dated 22 August 2007) and the Swiss federal tax administration (Circular Letter Nr. 20, dated 27 March 2008) (Circular Letters). Conversely, the preliminary draft bill will introduce explicit provisions on the taxation of trusts, which shall be applicable not only to trusts governed by Swiss law, but also to foreign trusts with a Swiss nexus (Swiss tax liability based on personal affiliation of either the settlor and/or the beneficiaries, depending on the qualification of the trust). Trusts established before the envisaged legislation enters into force that do not receive further grants from the settlor even after this date shall remain under the scope of existing practice, i.e., the aforementioned trusts will not fall under the envisaged legislation’s scope.

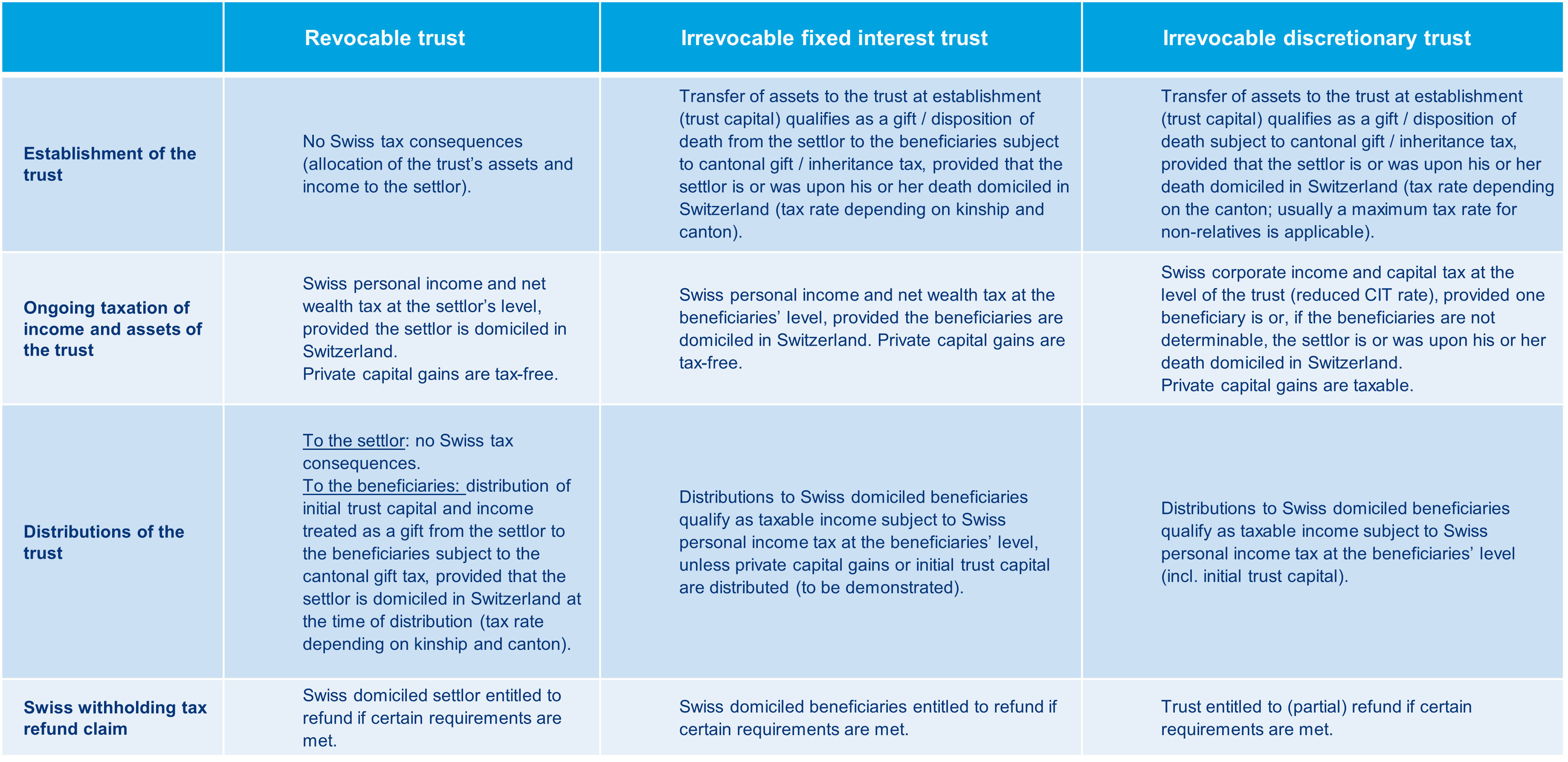

Similar to the Circular Letters, the preliminary draft bill stipulates that the taxation of trusts will mainly depend on their qualification. In other words, the first step is to determine whether a trust qualifies as a revocable trust (transparent for Swiss tax purposes) or an irrevocable trust.

- Revocable trusts (transparent for Swiss tax purposes)

In the case of revocable trusts, the settlor retains control over the trust’s assets. Consequently, the trust’s assets and income are attributed to the settlor for Swiss tax purposes, i.e., the Swiss domiciled settlor remains fully taxable on the trust’s assets and income for Swiss personal income and net wealth tax purposes. The establishment of a revocable trust and distributions thereof to the settlor have no Swiss tax consequences. However, distributions from a revocable trust to a beneficiary qualify as a gift and are thus subject to cantonal gift tax depending on the degree of kinship between the settlor and the beneficiary, given that the settlor is domiciled in Switzerland at the time of distribution. The distribution received increases the net wealth tax basis of Swiss domiciled beneficiaries. Therefore, the planned provisions on the taxation of revocable trusts embraces the current practice.

- Irrevocable trusts

On the other hand, for irrevocable trusts a second distinction is made between trust deeds in which the beneficiaries and their entitlements are specified (so-called “irrevocable fixed interest trusts”) and trust deeds in which the beneficiaries are not determined, with the beneficiaries only holding an expectative right to the trust’s assets and income (so-called “irrevocable discretionary trusts”).

- Irrevocable fixed interest trust

Irrevocable fixed interest trusts are characterized by the settlor’s lack of rights or obligations in relation to the trust’s assets (definitive divestment of the settlor). For Swiss personal income and net wealth tax purposes, the assets and income of the trust are attributed to the beneficiaries, i.e., the Swiss domiciled beneficiaries of a fixed interest trust are taxed in proportion to their share on the trust’s assets and their respective income in Switzerland. Provided that the settlor is domiciled in Switzerland at the time of the trust’s establishment, the transfer of assets to the trust qualifies as a gift from the settlor to the beneficiaries subject to cantonal gift or inheritance tax (the tax rate depends on the degree of kinship between the settlor and the beneficiaries as well as the canton). Unless private capital gains or initial trust capital are distributed, distributions from the trust to the beneficiaries are taxable as income at the level of the beneficiaries. Hence, the planned provisions on taxation of irrevocable fixed interest trusts are also in line with the current practice.

- Irrevocable discretionary trust

However, as for irrevocable discretionary trusts, the intention is to deviate from the current practice. When establishing an irrevocable discretionary trust, a distinction is currently made from a tax perspective between settlors domiciled in Switzerland and those domiciled abroad. If a settlor is domiciled in Switzerland, the tax consequences of the irrevocable discretionary trust are at present the same as for the revocable trust, i.e., the settlor remains fully taxable on the trust’s assets and income for Swiss personal income and net wealth tax purposes (allocation of the trust’s assets and income to the settlor).

Conversely, with irrevocable discretionary trusts established by foreign domiciled settlors, the trust’s income and assets can neither be attributed to the settlor nor to the beneficiaries. Consequently, the settlor is currently not taxable on the trust’s assets and income upon his subsequent arrival in Switzerland. Further, the trust’s assets and income escape Swiss taxes if they are not transferred to a beneficiary subject to Swiss taxation.

According to the preliminary draft bill, the trust’s income and assets will newly be attributed to the trust, which will be treated similarly to a foundation (independent taxable entity). For the trust to be subject to unlimited tax liability in Switzerland, at least one beneficiary or – if the beneficiaries cannot be determined – the settlor should be domiciled in Switzerland (Swiss tax liability based on personal affiliation).

As the preliminary draft bill currently stands, the following taxes may be due:

- upon establishment of the irrevocable discretionary trust, cantonal gift and/or inheritance tax (where applicable);

- if at least one beneficiary or, if applicable, only the settlor is (or was upon his or her death) domiciled in Switzerland, corporate income tax at a reduced rate (similar to a foundation) and capital tax at level of the irrevocable discretionary trust; and

- upon distribution of trust income and initial trust capital to Swiss domiciled beneficiaries, personal income tax.

The preliminary draft bill also contains a subsidiary rule in case the trust is resident abroad according to an applicable double tax treaty. To prevent the trust from escaping Swiss taxation in these cases, it is planned that the trust’s income should be allocated to the settlor, provided that the beneficiaries or the settlor are or were Swiss residents.

- Summary

The envisaged taxation of the Swiss trust and foreign trusts with a Swiss nexus can, in principle, be summarized as follows (note that the following chart is based on the assumption that the parties involved are natural persons domiciled in Switzerland):

Conclusion

The introduction of the Swiss trust is a welcome step. The Swiss trust would represent a new alternative to foreign legal institutions and existing structures under Swiss law, – expanding business opportunities for the trust industry and serving Swiss residents who currently lack an estate and wealth planning instrument that meets their needs.

Further developments

The consultation on the preliminary draft bill was completed at the end of June 2022. Now, the Federal Council is preparing a final draft bill and a corresponding dispatch, which will subsequently be submitted to the two chambers of parliament. If these chambers take up the matter, a detailed discussion will take place. In the end, both chambers of parliament must approve the entire bill for it to be passed. Finally, an optional referendum may be held against the bill.

It is assumed that the debate in the chambers of parliament will commence in the spring session of 2023 at the earliest. Therefore, the bill is not expected to enter into force before 2024.

Contact us

Should you require any assistance in the field of trusts and taxation in Switzerland, please contact us below.