To answer this question, we will comment the differences between a long-term lease (as regulated in the new Book 3) and a (retail) lease from various perspectives.

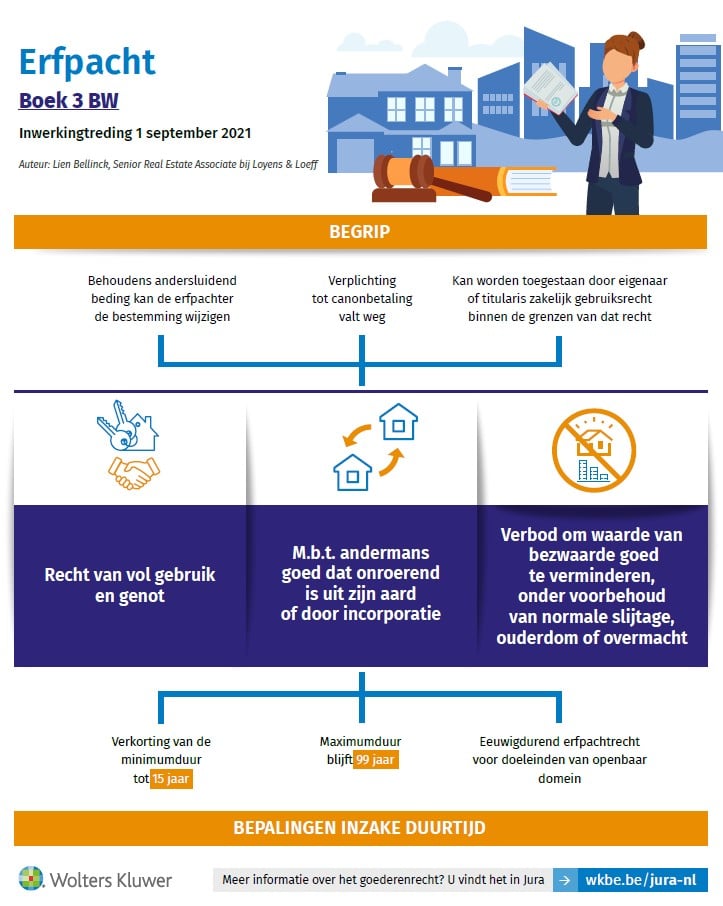

Download the presentation here. You will also find below an infographic explaining the changes to the long-term lease right as well as the recordings in French and Dutch of our webinar on the subject.

Webinar: Long-term lease vs (retail) lease in French

Watch the recording of our webinar "Long-term lease vs (retail) lease" in French by registering here.

Webinar: Long-term lease vs (retail) lease in Dutch

Watch the recording of our webinar "Long-term lease vs (retail) lease" in Dutch by registering here.