What are the new rates?

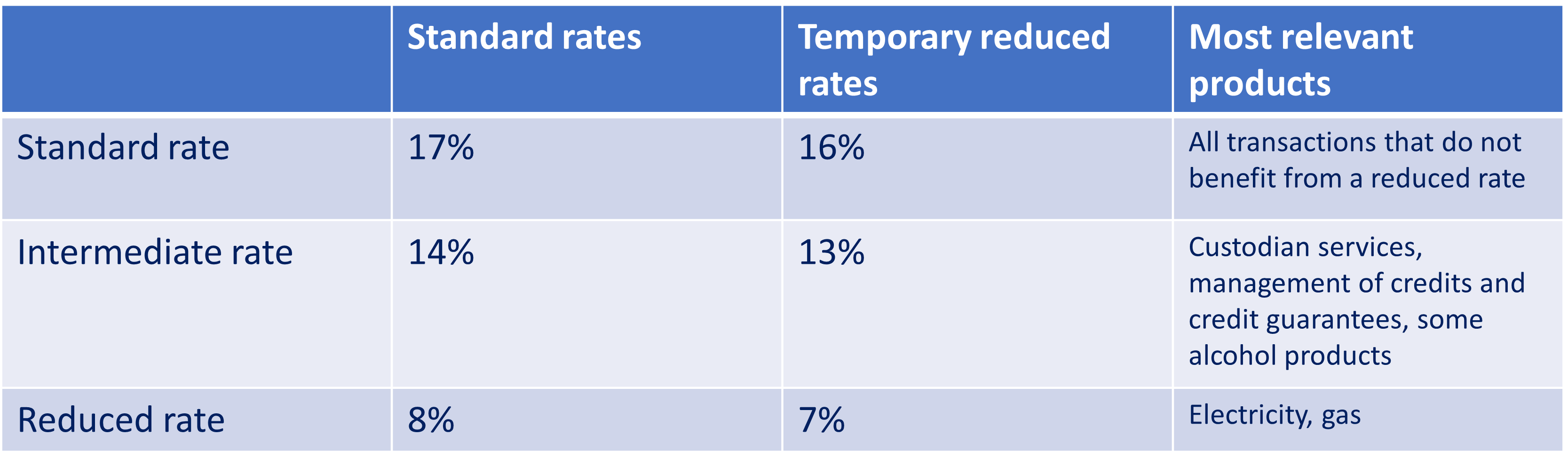

Most of the current rates will be reduced by 1%, so the temporary reduced rates will be as follows:

Note, however, that the super-reduced rate of 3% remains unchanged.

When is the entry into force?

The reduced VAT rates will be applicable during a temporary period starting on 1 January 2023 and running until 31 December 2023.

What rate should be invoiced and when?

However simple it may sound, the adoption of a temporary reduction in VAT rates can raise difficulties of practical implementation. This is especially the case for transactions that will take place straddling 2022 and 2023, and for successive or down payments and continuous supplies.

The complexity that can materialize for specific transactions calls for heightened attention and careful review of the legal position to ensure the correct application of the accurate VAT rate.

Does this mean that my charges will be reduced?

In a nutshell, in most instances yes. A decrease in VAT rate should reduce the overall price of the goods and services you purchase – this comes as good news in a context of strong inflation. However, for prices that have been negotiated all taxes included, the seller may be tempted to simply increase its profit margin, thereby depriving this measure of its practical effect.

What impact on my net margin?

Although the aim of the measure is to mitigate the effects of increased energy prices and consumer prices in general on households and businesses, the new legislation does not require that the reduction in the VAT rate be passed on to the customer. Businesses can, if they so wish, maintain their current gross prices including VAT with only an accounting adjustment to the billing to reflect the new rates. This is the case where the prices have been agreed all taxes included.

What needs to be adapted internally?

Companies are required to scrupulously apply the correct VAT rates for their activities. To this end, accounting and legal services will need to consider at least the following:

- Adapt their IT systems and templates to ensure that the invoices issued will indicate the correct VAT rates;

- Existing contracts may have to be be amended to reflect this rate change and contract templates may also have to be updated;

- The input VAT on on invoices from foreign providers will have to be self-assessed in accordance with this temporary measure. Note that eCDF – the online platform used to file VAT returns – will also be updated to reflect the new VAT rates in the 2023 VAT returns;

- E-commerce businesses that are established abroad and charge Luxembourg VAT through the OSS must adapt their systems to ensure that VAT is applied properly.

Of course, it must be borne in mind that the measure is temporary and a recovery to the current situation will therefore have to be implemented again for 2024.

What if too much VAT has been invoiced?

Any VAT mentioned on an invoice is, by law, due to be remitted to the Luxembourg Treasury. Raising an invoice with an incorrect VAT rate exposes the seller to the risk that the customer may object and not pay the total amount invoiced. In this case, the first reflex is to find out whether a corrective invoice with the proper VAT rate can still be issued to the client.

Should this not be the case because the wrongly invoiced VAT has already been paid to the Luxembourg Treasury, a refund application will have to be submitted to the tax authorities. The question of the refund by the State of an amount of VAT wrongly collected is currently undergoing some developments in case law (CJEU, Finanzamt Österreich, C-378/21). Nevertheless, besides being complex and time-consuming, the success of such an application is never guaranteed.

We can only urge companies to be cautious and well prepared with the foregoing. Your Loyens & Loeff VAT experts are more than happy to help you preparing for 2023!