Under the initial Luxembourg DAC 6 law, as from 1 July 2020, intermediaries and, in some cases, taxpayers with a link to Luxembourg have become subject to new reporting obligations towards the Luxembourg tax authorities. Exempt intermediaries are not subject to this reporting obligation but to a notification obligation towards other intermediaries involved and, in some cases, taxpayers. More background information is available here.

The retroactive entry into force on 30 June 2020 of the Luxembourg law implementing the optional deferral proposed by the EU means that intermediaries and taxpayers have more time to determine whether they have been involved in reportable cross-border arrangements (RCBAs), and if so, when they must comply with their reporting or notification obligation.

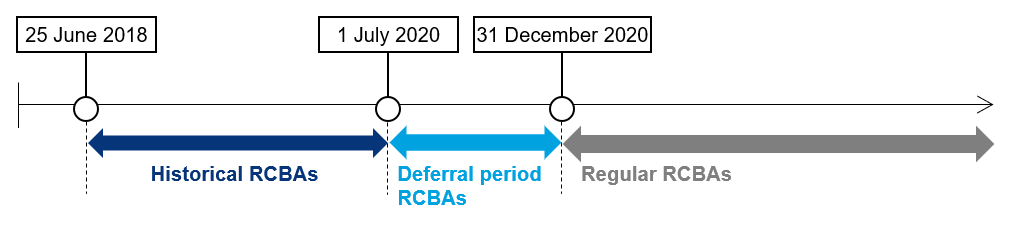

1. Three categories of RCBAs timewise

Timewise, there are now three categories of RCBAs:

- historical RCBAs – the reporting and notification trigger point occurred between 25 June 2018 and 30 June 2020;

- deferral period RCBAs – with a trigger point occurring between 1 July and 31 December 2020;

- regular RCBAs – with a trigger point occurring as from 1 January 2021.

2. New reporting deadlines

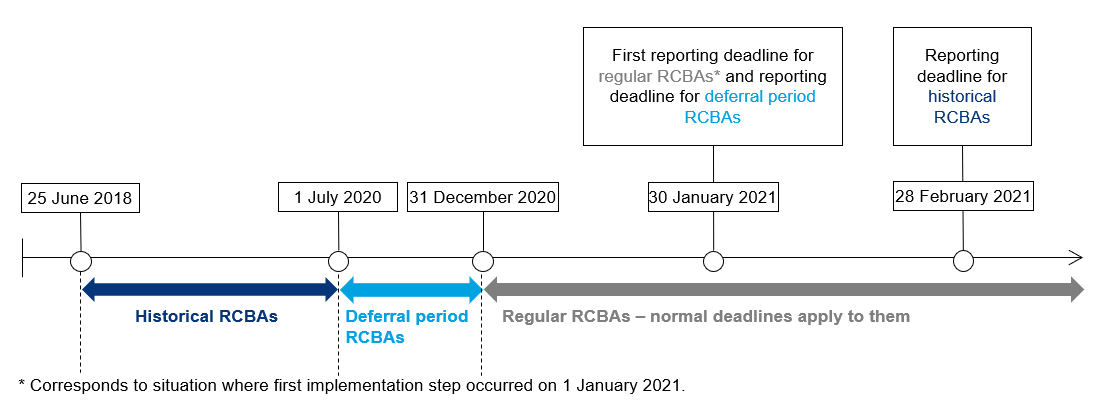

Historical RCBAs must be reported by 28 February 2021 and deferral period RCBAs by 31 January 2021. Regular RCBAs remain subject to the default rule: they must be reported within 30 days beginning either on the day after the RCBA is made available or is ready for implementation, or when the RCBA first step is implemented, whichever occurs first. The earliest reporting deadline for regular RCBAs will thus be 30 January 2021.

These deadlines apply to:

- non-exempt intermediaries; and

- taxpayers subject to a reporting obligation (either because no intermediary is involved or because the reporting obligation has shifted to them due to an intermediary being exempt).

For non-exempt intermediaries providing assistance with respect to the design, marketing or implementation of an RCBA, the deadline for reporting regular RCBAs remains 30 days after the day on which they provided such assistance. This 30-day period starts on 1 January 2021 for deferral period RCBAs. The reporting deadline for historical RCBAs is 28 February 2021.

3. New notification deadlines

Exempt intermediaries must meet their notification obligation relating to regular RCBAs within 10 days beginning either on the day after the RCBA is made available or is ready for implementation, or when the RCBA first step is implemented, whichever occurs first. The earliest notification deadline for regular RCBAs will thus be 10 January 2021. This 10-day notification period starts on 1 January 2021 for deferral period RCBAs. Although not clearly stated in the law, the notification deadline for historical RCBAs will likely be Thursday 25 February 2021 to assist non-exempt intermediaries and relevant taxpayers meeting their own reporting obligations.

4. How to prepare meeting these new obligations

The deferral of six months is a welcome development, even though some Member States (such as Germany) have opted not to allow the delay. The extra time now available for preparation should not lead to complacency. Taxpayers and their service providers should continue to review their past arrangements. Where appropriate, they should set up a tax risk governance framework enabling them to allocate responsibilities, provide adequate internal training, identify potential RCBAs, collect and store relevant data, manage reputational risks in case of leaks and (preferably) ensure a seamless coordination between taxpayers and service providers.

Loyens & Loeff can assist you with the implementation of such framework. Do not hesitate to contact one of our experts on the topic should you require any assistance.