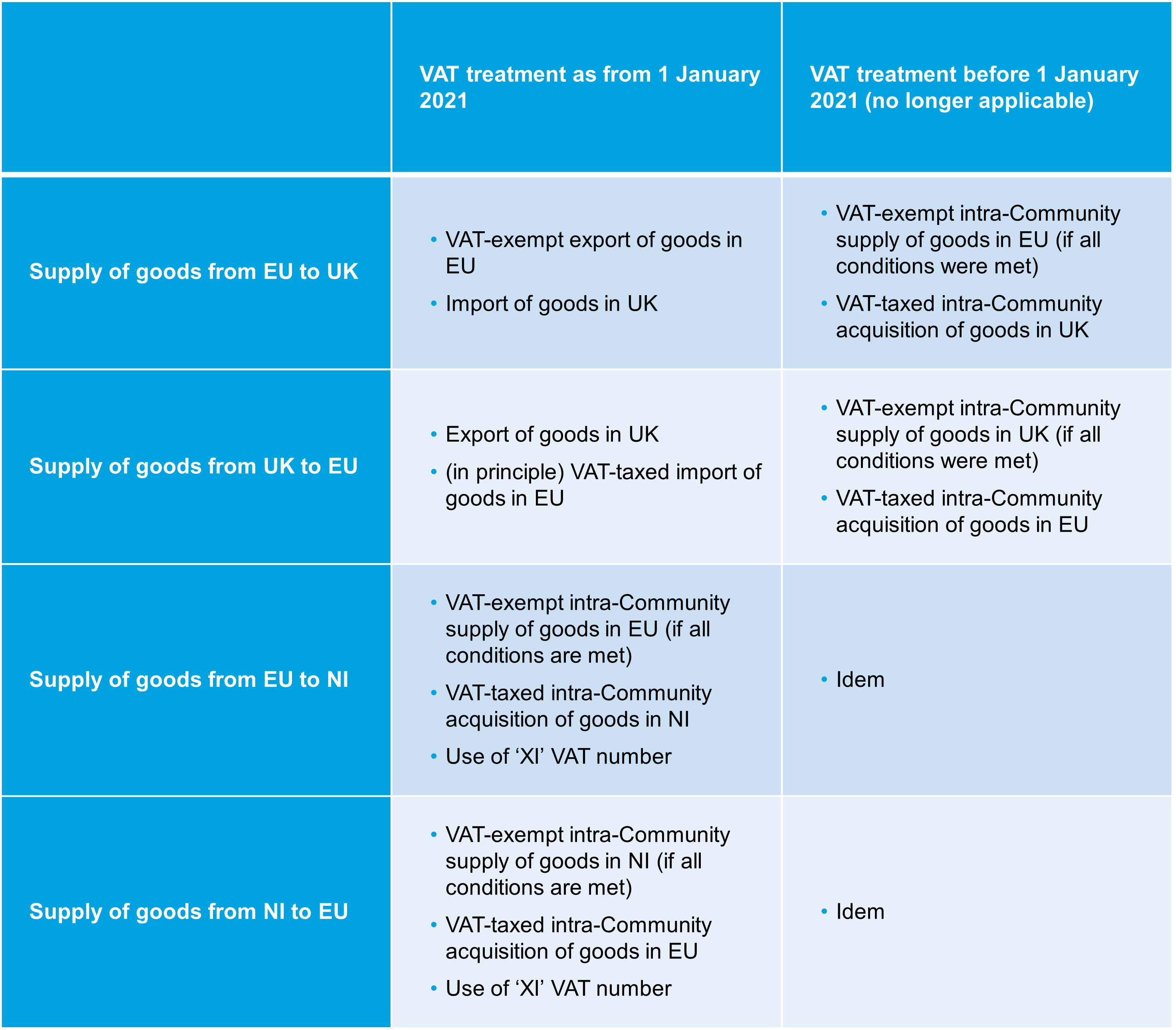

Note that these VAT treatments also apply to services supplied to Northern Ireland. Contrary to supplies of goods to Northern Ireland, there is no specific regime for supplies of services to Northern Ireland.

Supply of B2B services

Services provided by one taxable person to another taxable person (B2B) are - as a general rule - located at the place where the recipient is established (art. 44 EU VAT Directive 2006/112/EC). Accordingly, services supplied by a Belgian taxable person to a UK taxable person would still take place in the UK. The Belgian service provider would have to issue an invoice without VAT, but mentioning ‘Supply of services - VAT reverse charge - art. 44 and 196 EU VAT Directive 2006/112/EC’. The UK taxable person would have to consider local UK rules to establish the VAT treatment of the services received (but probably must, as is currently the case, still self-assess UK VAT). Note that, as a result of the UK becoming a third country, the Belgian taxable person would have to report this transaction in box 47 of its Belgian VAT return (no longer in box 44 and no intra-Community listing).

Services supplied by a UK taxable person to a Belgian taxable person on the other hand would - in accordance with EU legislation - take place in Belgium. The Belgian taxable person would have to self-assess the Belgian VAT due via its periodic VAT return.

Supply of B2C services

Where there in principle is no impact of the Brexit on the VAT treatment of B2B services, there is one for B2C services. As a general principle, the place of supply of services provided to private individuals or non-taxable persons is located at the place where the supplier is established. Accordingly, when services are provided by a Belgian taxable person to a UK private individual, the Belgian service provider would have to issue an invoice with Belgian VAT.

However, for many types of services provided to private individuals or non-taxable persons established outside the European Union (i.e. the UK after Brexit), such as advertising, consultancy and accountancy, bank, financial and insurance transactions, a different localization rule applies, indicating that those services are located in the country where the recipient is established (art. 59 EU VAT Directive 2006/112/EC). The Belgian taxable person would then have to issue an invoice without VAT, but mentioning ‘Service located in country of recipient - art. 59 EU VAT Directive 2006/112/EC’.

Exceptions to general principles

It should be noted that a derogation to these general principles could apply for specific types of services.

For example, services linked to an immovable property are deemed to take place where the immovable property is located. Consequently, when e.g. a Belgian law firm assists a UK resident (private individual or taxable person) with the drafting of a purchase-agreement for real estate in Belgium, Belgian VAT needs to be charged, since the immovable property is located in Belgium.

Another example is the supply of electronic services (telecommunication, broadcasting and other electronic services) provided to private individuals or non-taxable persons. Such services are located where the recipient is established.

VAT refund

As a result of these derogations to the general principles, it could be that Belgian VAT has been paid by a UK taxable person. To the extent that this VAT is deductible, the UK taxable person could request refund of the Belgian VAT via application of the 13th Directive (86/560/EC).

In the event that a Belgian taxable person would have paid UK VAT and qualifies for refund thereof, the Belgian taxable person would have to contact the British VAT authorities (refund of UK VAT for transactions carried out in 2020 could in principle be requested via Intervat until 31 March 2021).

Overview main EU VAT localisation rules for services after Brexit