This article is also available in Dutch and in French.

Tax-free gifts made before a foreign notary

Belgian gift tax is a registration tax: gift tax is only due when the gift is registered in Belgium.

Article 19 of the Registration Tax Code currently only provides for a mandatory registration for Belgian notarial deeds.

This means that Belgian gift tax is always due on gifts of movable assets made before a Belgian notary.

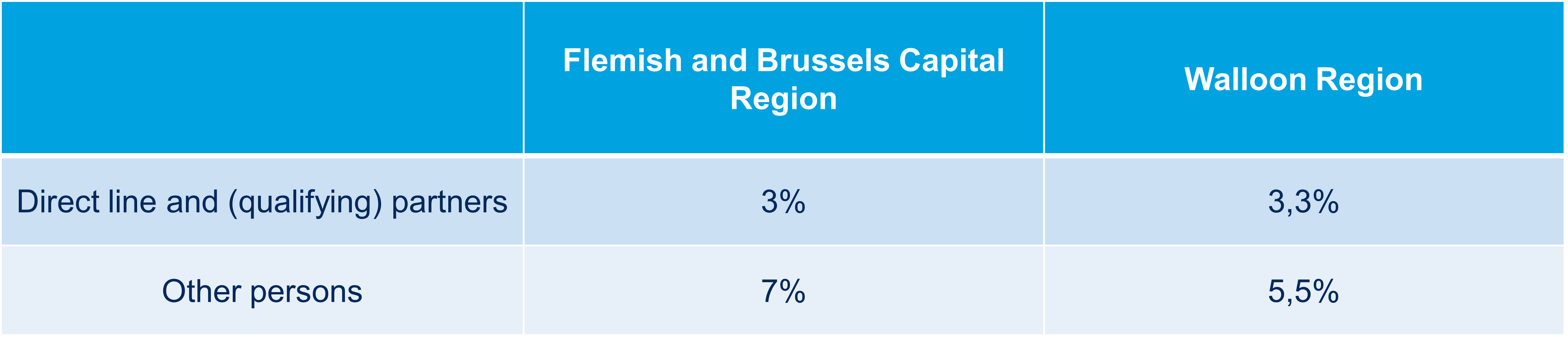

The Belgian regions determine the applicable tax rate:

Currently, foreign deeds of gift do not fall under the scope of the registration obligation included in article 19.

Making a gift of movable assets before a foreign notary is therefore very common in Belgian estate planning. If the deed of gift is not voluntarily registered, no gift tax is due in Belgium. In such case, there is however a risk of inheritance tax being due at (high) progressive tax rates. If the donor dies as a Belgian resident within 3 years after the gift was made, inheritance tax will be due in Belgium. Earlier, the Flemish Region announced that this term would be extended to 4 years. This term is already set to 7 years for gifts of qualifying family owned businesses.

Draft bill

The draft bill of 17 June intends to extend the registration obligation to foreign notarial deeds of gift.

This means that, if the draft bill is adopted, gift tax will also be due on gifts of movable assets made before a foreign notary.

The draft bill targets all gifts, i.e. both the gifts made in full ownership and the gifts made with reservation of usufruct.

Entry into force (Updated on 8 July 2020)

Initially, the draft bill provided for an entry into force 10 days after the publication of the law in the Belgian Official Gazette.

In the meantime, the entry into force is postponed to 1 December 2020 by an adjusted draft bill, allowing Belgian residents more time to make tax-free gifts in a notarial deed.

Belgian parliament has yet to adopt the draft bill.

Handsels and bank gifts remain tax-free

The draft bill does not introduce a mandatory registration for handsels and bank gifts.

Therefore, it remains possible to make a tax-free gift through a handsel or a bank gift.

In such case, the donor needs to consider that there is a risk of inheritance tax being due when he / she dies within 3 years after the gift is made.

Contact

We will follow up on the draft bill and will keep you informed. Please do not hesitate to contact your Loyens & Loeff advisor should you have any questions.