We have listed below some high level and practical recommendations to the directors of a Belgian company in financial distress. Bear in mind that by ‘directors’, we mean not only the individuals that are formally appointed as director (either in person or via a management company), but also de facto directors being any person that has actual decision-making powers with respect to the Belgian company, through a formal mandate or otherwise. Please note that the risk assessment and adequate measures depend in large part on the factual circumstances surrounding the company and should be assessed carefully.

In a previous article we highlighted directors’ duties and liabilities in Belgium, within the context of COVID-19.

Regarding a director’s criminal liability risk, you can read more about the blind spot of directors' criminal liability as participants in offences committed by or within the company here.

Generally, directors must exercise their directorship with due care and diligence. The yardstick for this is what would be expected from a normally careful and diligent director put in the same situation. This implies that the duty of any director of a Belgian company is to always act in the best interests of the company and to comply at all times with the articles of association and the relevant legal provisions.

Unlike in other legal systems, directors are not to be considered as representatives of the shareholders by whom they were appointed. In making any decision, they must therefore act in the best interest of the company and not of a specific shareholder. The concept of corporate interest is not entirely clear under Belgian law. As a broad interpretation, it includes the interests of all stakeholders (among others; employees, customers, creditors, suppliers…). The Belgian Supreme Court appears, however, to support a more restrictive interpretation, which limits the corporate interest to the joint interest of a company’s current and future shareholders. It is unclear whether this ruling also applies in the context of assessing directors’ duties. Hence the most prudent position for the board of directors is to envisage the interest of all the stakeholders.

For the purpose of creditor protection, the Belgian Companies and Associations Code (BCAC) contains a so-called “alarm bell” procedure. In accordance with this procedure, the board is required to call a general shareholder meeting if, as a result of losses incurred, the company’s net assets have decreased below half of the share capital for public limited liability companies (naamloze vennootschappen / sociétés anonymes) or have become (or risk becoming) negative for private limited liability companies (besloten vennootschappen / sociétés à responsabilité limitée). The net assets of a company are the total sum of the assets, minus the provisions, debts and non-amortized incorporation funds, development costs and the costs for research and development.

The general meeting must be called within two months of the time at which the board is first made aware of the deteriorated net asset situation (i.e. not only on the basis of annual accounts but also of quarterly or interim accounts).

During this general meeting, the shareholders must decide whether to dissolve the company or preserve its continuity. If dissolution is not proposed by the board, this decision must be made based upon measures proposed by the board in a specific report.

The same procedure applies if the net assets of a public limited liability company have decreased below a quarter of the share capital. In such a case, however, the dissolution of the public limited liability company can be decided by only a quarter of the votes cast at the general meeting. For private limited liability companies, directors have the same obligation if it is no longer clear, in accordance with reasonable expectations, whether the company will be able to repay its debts as the fall due in the next twelve months. As this final parameter is subject to interpretation, it is advisable in situations of financial crisis to include in the board minutes any and all evidence that the latter legal condition is not met.

If the board fails to call the general meeting in any of the above situations, any damage suffered by third parties will be deemed as resulting from such a failure. In the context of an insolvency situation, the bankruptcy trustee will also immediately verify whether this obligation has been complied with.

The BCAC requires the board of directors of a Belgian company to deliberate on measures to be taken, to ensure the continuity of its economic activities for a minimum period of twelve months, if grave and consonant facts could endanger the continuity of the business.

To comply with this obligation, the company’s directors need to continuously monitor the company’s financial situation, so that, if the company’s financial situation deteriorates, it can take the necessary steps in a timely fashion.

In the event of bankruptcy and the shortfall of a company’s assets, its director, former director, managing director or any other person who had de facto authority to manage the company, can be held personally liable for all or part of the company’s debts up to the shortfall, if:

- at any given time prior to the bankruptcy, this person knew or should have known that there was manifestly no reasonable prospect of maintaining the enterprise or its activities and avoiding bankruptcy;

- this person was a director at that time; and

- this person did not act as a normally careful and reasonable director would have acted in identical circumstances.

The Court has the discretionary competence to order the directors jointly or individually to pay part or all of the company’s debts.

According to Belgian law, an enterprise which (i) faces a persistent cessation of payments and (ii) has lost the trust of its creditors, is in a state of bankruptcy. Both conditions must be met.

The cessation of payments occurs when a company can no longer repay its due and payable debts. It is not sufficient that the company cannot repay one debt, but it is also not necessary that the company has stopped all payments. Cessation of payment will occur when it becomes impossible for the debtor to pay certain important debts, such as social security or tax liabilities. The cessation must be persistent over a period of time, which cannot be derived only from a temporary liquidity problem but must be of a consistent nature.

No cessation of payment will occur, as long as the debtor keeps the trust of its creditors. The company is not in a state of bankruptcy if its situation can be redressed or the company still has access to sufficient credit or to assets that can be sold in a medium or short term.. It can be argued that a creditor which: agrees on a new credit, maintains an existing credit, does not accelerate an existing credit, or does not sue the debtor to recover a debt which is due, keeps its trust to the debtor. It is recommended that the directors record in the board minutes all elements providing evidence of the trust of the company’s creditors; in particular its banks and other important creditors.

In the event of the bankruptcy of a company and a shortfall of its assets, its director, former director, managing director or any other person who had de facto authority to manage the company, can be held personally liable for all or part of the company’s debts up to the shortfall, if that person committed a gross and manifest negligence that contributed to the bankruptcy. Courts have the discretionary competence to order the directors jointly or individually to pay part or all of the company’s debts.

Gross and manifest negligence is a fault that a normally careful and reasonable director would not have committed and that violates the essential rules of the community. A clear causal relationship between the negligence and the company’s bankruptcy does not necessarily have to be proven. Any gross and manifest negligence which contributed to the bankruptcy is sufficient, such as:

- conducting a commercial activity without having the required financial means;

- selling without charging VAT, so that the book-keeping does not give a true and reliable reflection of the company’s situation;

- payments of substantial amounts to an affiliated company, without their repayment being guaranteed in any way, in breach of corporate interest, in order to benefit another company of the group;

- committing any form of gross financial fraud (whether organised or not) (Article 5, §3 of the Act of 11 January 1993).

Both the bankruptcy trustee and the creditors can bring action against the directors, based on gross and manifest negligence.

Belgian law provides for specific directors’ liability in the case of a failure to pay taxes.

Directors are jointly liable for failure to pay the company tax prepayments or VAT, if this is due to tortious negligence in the performance of their management tasks.

For company tax, there is a (rebuttable) presumption of fault if at least two quarterly or three-monthly expired prepayments per year have not been paid, depending on whether the prepayment is due to be paid quarterly or monthly.

For VAT, there is a (rebuttable) presumption of fault if at least two or three claimable debts are not paid within a period of one year, depending on whether the taxpayer must submit the VAT declaration quarterly or monthly.

There is no presumption of fault if the non-payment is due to financial difficulties that led to the procedure of judicial reorganisation, bankruptcy or dissolution.

A director can also be held liable to the National Social Security Authority for the unpaid social contributions due at the moment of opening of bankruptcy proceedings if, during a period of five years before the bankruptcy, that director held a management position in at least two other companies which were declared bankrupt or liquidated and where social security contributions were unpaid.

Directors of a Belgian company which meets the bankruptcy conditions (see 5 above) must file a bankruptcy petition within 30 days of the date of cessation of payments.

Failure to file this in a timely manner may result in the personal liability of the directors for any increase in the level of indebtedness resulting from the delay in filing the petition. It can also constitute a criminal offence if it was the directors intention to postpone bankruptcy in any way.

The obligation to file is, however, suspended in the case of a company filing for judicial reorganisation.

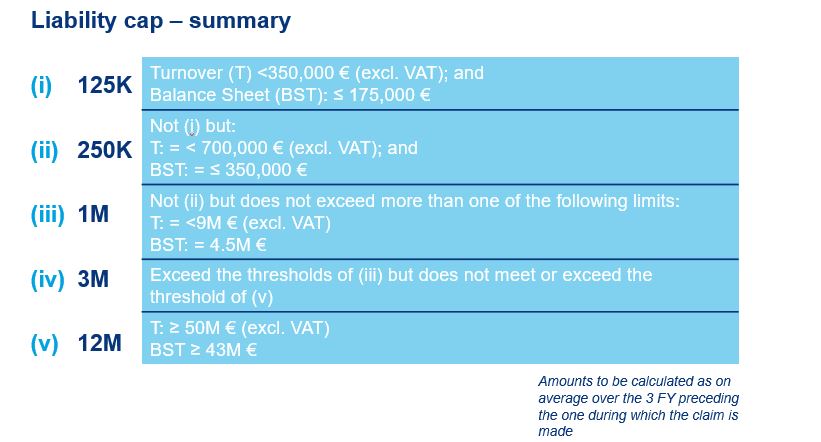

The BCAC introduced a cap on the potential liability of directors. The scope of the limitation is, however, limited, as it does not apply in cases such as:

- a recurring minor error, gross misconduct or fraudulent intent;

- the specific “guarantee liabilities” (garantieverplichtingen / obligations de garantie) as set out in the BCAC (e.g. liability for the shares for which no valid subscription has been made or liability for the actual payment of the shares for which they are considered to be the subscribers); or

- the joint and several liability resulting from the withholding of unpaid taxes; unpaid VAT; or unpaid social security contributions in the case of company bankruptcy.

The cap varies depending on the size of the company and applies as an aggregate for all directors, managing directors and members of an executive committee concerned, as well as for claims based on the same fact(s) regardless of the number of plaintiffs. The liability cap applies both vis-à-vis the company and third parties, and is irrespective of the grounds or basis of the liability claim (contractual or non-contractual).

Indemnity (hold harmless) clauses (which aim to transfer the financial consequences of the liability to another party) and exoneration clauses in favour of the director, cannot be granted (up front) by the company (or by one of its subsidiaries). The BCAC does not prohibit such clauses granted by a shareholder or other entity higher up within the group.

Directors can also insure their contractual and tort liability through a D&O insurance. The company (or group) will pay the insurance premium; the director is the beneficiary. The director thus does not escape liability as such, but only the financial consequences thereof.

A director can never be indemnified for criminal penalties, or for wilful intent or fraud under an indemnity clause or a D&O insurance.

In principle, a director would only not be jointly and severally liable if he or she can establish that he or she (i) did not participate in committing the violation, and (ii) reported the alleged misconduct to all other members of the board.

With respect to the criminal offence committed by the director in the execution of his/her function, the prosecutor must prove that the director can be blamed personally and individually for the offence. In a distressed company, the risk of directors committing a criminal offence is heightened. Examples of grounds for criminal liability include:

- falsifying documents;

- obscuring the assets of a company;

- abuse of confidence;

- misusing company goods;

- private bribery;

- money laundering;

- specific criminal provisions in the BCAC:

- failure to present the special report required by law for a capital increase through a contribution in kind, during the shareholders’ meeting;

- failure to submit the accounts to the general shareholders’ meeting within six months following the closing of the financial year;

- failure to deposit with the National Bank the annual accounts and the annual Board report within 30 days of approval. In the case of fraudulent intent, more severe sanctions apply;

- failure to call a shareholders’ meeting within the three weeks following a special request to do so;

- payment of an interim dividend in disregard of Article 7:213 of the BCAC;

- the drafting of false annual accounts with fraudulent intent or with the intention to cause damage.

When there are several directors and/or officers, it can be difficult to establish who exactly committed the criminal offence. The court will determine the responsible persons, after thoroughly analysing the facts and circumstances of the criminal offence. The concrete assignment of duties will be decisive, rather than the legal division of tasks.

In practice, directors and/or officers are often held liable for acts they ordered, without being the material author of the criminal offence themselves. This rule also applies in situations in which it was the director’s task to ensure that certain legal obligations were respected.

Directors can resign by means of a notification to the company (preferably by registered letter). Resignation is a unilateral act and therefore does not have to be accepted by the company. The company can, however, request that the director remain in office, in order to allow the company time to find a replacement.

The articles of association may contain a notice period and/or compensation provision.

If a director commits an error in relation to his/her resignation, his/her liability can be brought to court.

Resignation does not make a director exempt from liability. Directors can still be held liable for faults committed during the period before their resignation. The statute of limitations of all claims against directors originating in their function (including those based on tort) expire five years after the date of the opposed actions or, if they have been concealed on purpose, starting from the date of discovery of these actions.

For civil claims based on a criminal offence (e.g. the delayed declaration of bankruptcy) specific rules apply.

For a resignation to be enforceable against third parties, it must be published in the Annexes of the Belgian Gazette. If not, the director concerned can still be held jointly liable, even after the date of his/her resignation, vis-à-vis third parties, for the breach by other directors of the BCAC or the articles of association.

The annual shareholders’ meeting will decide on the discharge of the directors through a separate vote, after the approval of the annual accounts. A valid discharge means that the company can no longer sue the directors for past conduct covered by the discharge. However, the aforementioned discharge is not binding to third parties and minority shareholders who did not approve it.

The validity of the discharge is subject to the condition that the true financial situation of the company was not obscured by any omissions or incorrect statements in the accounts. Whether the omission or incorrect statement is caused by directors' wrongful intent or by ordinary fault is irrelevant. Inaccuracies in the accounts do not invalidate the discharge if the annual shareholders’ meeting has been otherwise informed of the company's true financial situation.

Transactions which violate the articles of association or the BCAC require a special discharge, as they have to be specifically mentioned in the agenda of the shareholders’ meeting, which then will decide upon the discharge.

A settlement can terminate the directors' liability towards parties to the settlement (other than the company or the shareholders). Since only the general shareholders’ meeting has the power to grant a discharge, such a settlement will only be valid (towards the company) if approved by the relevant shareholders.