Given its special status, as a result of the Protocol on Ireland and Northern Ireland, we will also briefly go into the VAT regime for supplies of goods from and to Northern Ireland.

Import and export from and to UK

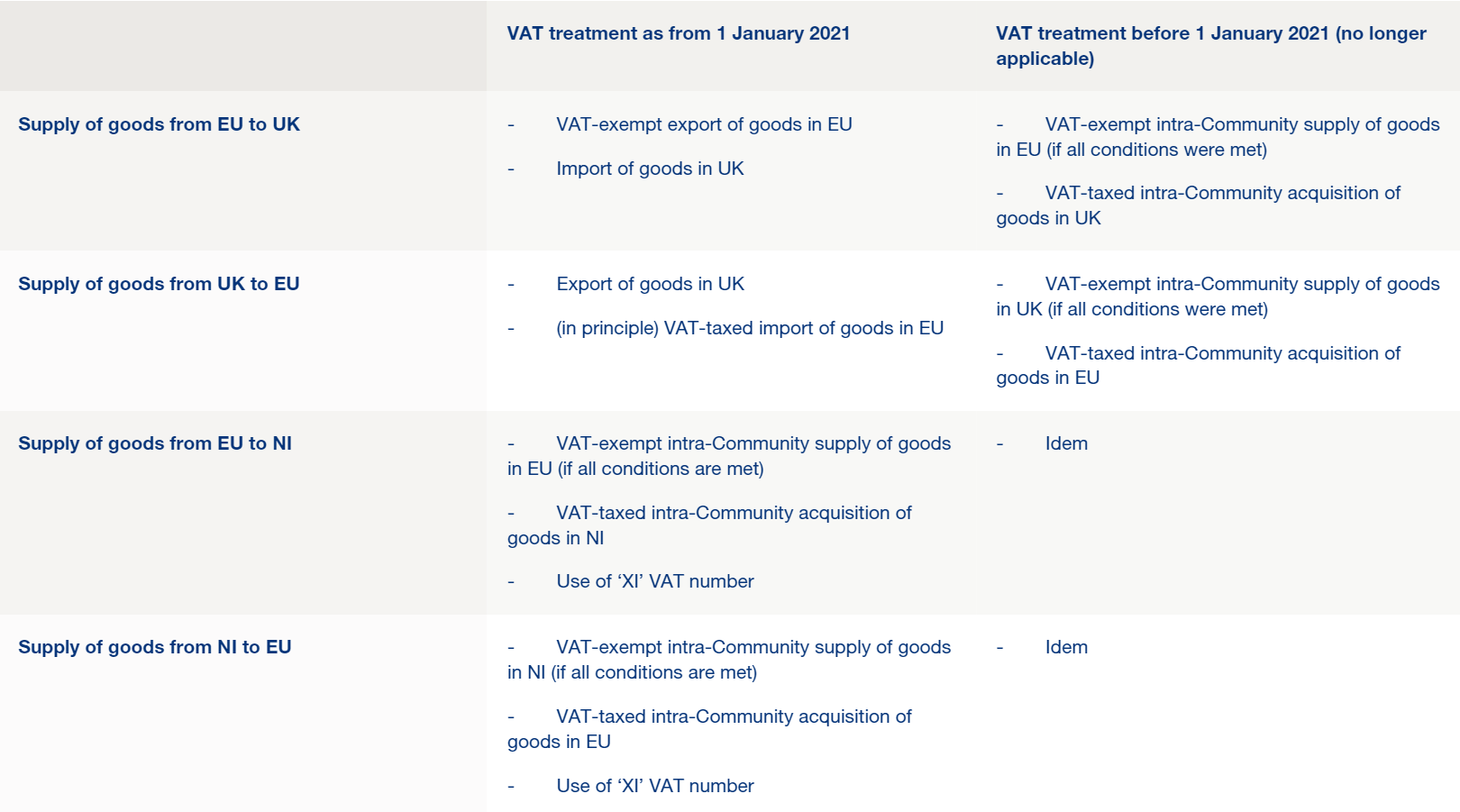

As of 1 January 2021, a supply of goods from the EU to the UK (excl. Northern Ireland) must - for VAT purposes - be treated as an exempt export of goods, and no longer as an exempt intra-Community supply of goods. Accordingly, when goods are transported from the EU to the UK, the supplier would have to issue an invoice (still) without VAT, but making reference to ‘Export of goods - art. 146 (1) (a) EU VAT Directive 2006/112/EC’. The supplier furthermore must demonstrate that the goods have left the EU as a condition for the application of the VAT exemption and keep documentary evidence. The UK recipient must consider local UK VAT rules to report the import of the goods in the UK. Note that, as a result of the UK becoming a third country, the supplier (given that the goods are transported out of Belgium) would have to report this transaction in box 47 of its Belgian VAT return (no longer in box 46 and no intra-Community listing) and comply with customs regulations (e.g. export declaration). The EU exporter should also no longer include its exports to the UK in its EU Intrastat return. However, businesses importing goods into the UK should still file UK Intrastat returns (if applicable) until 31 December 2021.

Similarly, a supply of goods from the UK (excl. Northern Ireland) to the EU must be treated as an (in principle) VAT-taxed import of goods instead of a VAT-taxed intra-Community acquisition of goods. The importer must possess an EORI number for this purpose. It must in this respect also be noted that the VAT on imported goods in principle becomes due at the moment that the goods enter the EU (unless the goods are put under a customs suspension regime) and that customs obligations must be fulfilled (e.g. import declaration). Belgian VAT law foresees however in the possibility to request for an E.T.14.000 license which allows to defer the payment of the import VAT to the Belgian periodic VAT return. As regards Intrastat obligations, imports into the EU should no longer be reported in the Intrastat return.

Since the UK has become a third country, the simplified triangulation scheme in principle could no longer be applied. Exceptionally, a UK taxable person could apply the simplified triangulation scheme for operations in the EU if he acts as intermediary and is registered in an EU Member State (other than the EU Member State of arrival). The call off-stock simplification is also no longer applicable when supplying goods to or from the UK.

Special status of Northern Ireland

Although Northern Ireland is part of the UK, all supplies of goods to and from Northern Ireland will, as a result of the Protocol on Ireland and Northern Ireland, remain subject to the same VAT regime that was applicable before 1 January 2021.

Accordingly, a supply of goods from the EU to Northern Ireland and vice versa would still be considered as an exempt intra-Community supply of goods (given that all conditions are met). The NI customer would have to report a VAT-taxed intra-Community acquisition in Northern Ireland. Important to note in this respect is that the newly introduced ‘XI’ VAT number should be used for these transactions in order to identify them separate from the UK VAT transactions (i.e. XI country code should be substituted in GB VAT number, e.g. XI 123456789 instead of GB 123456789).

Also intra-Community trade reporting obligations (incl. Intrastat) will continue to apply. Furthermore, the call off-stock and triangulation simplifications could still be applied, and, until the entry into force of the e-commerce VAT package on 1 July 2021, the distance sales threshold of EUR 85.000 would be maintained.

Fiscal representation for VAT purposes

Since UK taxable persons (who do not have a fixed establishment in the EU) as from 1 January 2021 must be considered as established outside of the EU for VAT purposes, this may result in the obligation to appoint a fiscal representative in some EU Member States.

In Belgium, a taxable person established outside of the EU carrying out taxable transactions in Belgium - for which he is considered to be liable for payment of the VAT (e.g. import, intra-Community acquisition) - is obliged to register for VAT purposes via the appointment of a fiscal representative. UK taxable persons with an existing so-called direct VAT registration in Belgium were in principle already notified by the Belgian VAT authorities of this new VAT obligation. These UK taxable persons have time until 31 March 2021 to file a request for a VAT registration via the appointment of a fiscal representative. Any new VAT registrations by UK taxable persons (i.e. no ‘conversion’ of a direct VAT registration) must be filed without delay once transactions are carried out in Belgium for which they are liable to pay VAT.

Overview of VAT treatment for supplies of goods