Volume 2 – Onboarding Swiss pension funds

The Swiss pension fund market ranks among the largest in Europe, with total assets under management (AUM) exceeding CHF 1.4 trillion (approximately USD 1.75 trillion). Pension funds represent the dominant share of AUM in Switzerland, positioning them as one of the most significant institutional investor bases in Europe relative to the country's size.

Swiss pension funds are increasingly pursuing international diversification strategies. While they continue to invest in traditional asset classes, there is a growing allocation toward alternative investments, including private equity, infrastructure, and private debt.

As Switzerland is not a member of the European Union, it maintains an independent regulatory framework. This framework governs both (i) the marketing of investment funds to Swiss pension fund investors and (ii) the onboarding process and associated restrictions applicable to such investors. Non-Swiss sponsors need to navigate these rules to make sure pension funds can invest in their products.

This article adopts a practical Q&A format, presented in two volumes, to guide readers through the key considerations. Volume 1: "Marketing to Swiss pension funds" outlines the steps and requirements for marketing to Swiss pension funds. This Volume 2 addresses the regulatory prerequisites for enabling Swiss pension funds to allocate capital to non-Swiss funds, with a focus on infrastructure or other alternative investments.

Can Swiss pension funds invest in non-Swiss investment funds?

Yes, under certain conditions. Swiss pension funds are regulated under the Ordinance on Occupational Retirement, Survivors’ and Disability Pension Plans (the OPP 2). OPP 2 sets out strict rules when it comes to the investment of assets that Swiss pension funds manage, including (i) general investment rules, and (ii) specific rules to invest in investment funds, as further outlined in the following sections. Swiss pension funds need to observe these requirements to determine whether they can invest in specific non-Swiss investment funds.

What are the general investment rules for Swiss pensions funds?

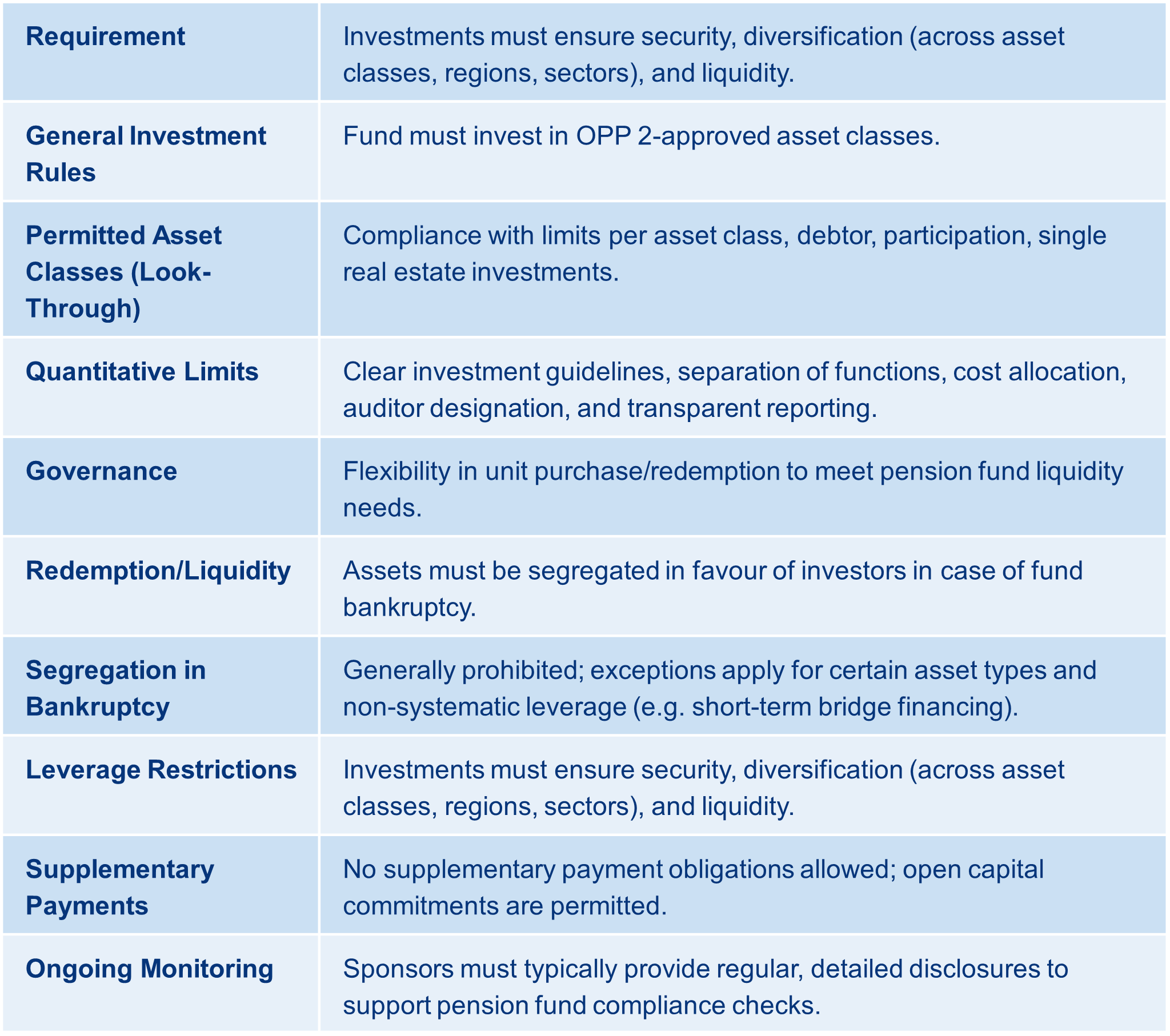

As a general rule, Swiss pension funds must guarantee the security as well as an adequate risk diversification of their investments. Accordingly, to lower overall portfolio risk, they need to select permitted asset classes with minimal or even negative correlation and distribute investments amongst such asset classes in a sensible manner. OPP 2 specifies that investments need to be allocated to different asset classes, regions and sectors.

In addition, pension fund investments are required to generate adequate returns and meet projected liquidity needs, ensuring benefits can be paid as they come due. Assets should be invested to allow for the necessary liquidity if there is a capital requirement, which is why there needs to be an allocation into short-, medium-, and long-term investments.

Finally, OPP 2 specifies permitted asset classes, including indirect investments in such asset classes via investment fund as well as derivatives. The catalogue includes such investments as cash, money market investments with duration up to 12 months, bonds, real estate, shares of listed companies as well as of Swiss operating non-listed companies, investments in infrastructure, alternative investments such as hedge funds, private equity, insurance linked securities, and commodities. Investments not listed in the catalogue are not permitted or, in some cases, qualify as alternative investments. OPP 2 also outlines quantitative restrictions on individual permissible investments, including:

-

- per asset class;

- per single debtor (10% per debtor, with exemptions);

- per participation in an entity (e.g. 5% per issuer of listed shares);

- per real estate investment (5% per property) and;

- per category (e.g. 50% shares, 30% in real estate of which one third abroad, 15% alternative investments, 10% infrastructure).

The investment activity of Swiss pension funds is supervised by cantonal authorities under the federal regulator (OAK BV), with independent auditors reviewing compliance with investment rules, diversification, and prudent management to ensure that the beneficiaries’ interests are protected. While the Swiss Financial Market Supervisory Authority (FINMA) does not directly supervise Swiss pension funds, it supervises external asset managers which manage pension fund assets.

What requirements does the non-Swiss investment fund need to meet to be eligible for investment by Swiss pension funds?

Non-Swiss investment funds qualify as "acceptable investments" for Swiss pension funds provided they meet specific statutory criteria. In addition, each Swiss pension fund must make sure that the investment complies with its internal investment directives. Pension funds are obligated to verify compliance with these standards both prior to investing and throughout the duration of the investment. Accordingly, sponsors, managers, and investment funds aiming to attract Swiss pension fund investors must proactively ensure adherence to these requirements.

Look-Through: OPP 2 requires the use of a "look-through" approach, where fund-level investments must also adhere to OPP 2 restrictions. As a result, the fund is required to make investments that align with the permitted asset classes outlined by OPP 2 which include cash, fixed income, real estate, listed equities, infrastructure, Swiss private equity/debt, and certain alternative investments.

Swiss pension funds will face monitoring costs to ensure investment fund targets comply with OPP 2. Sponsors and managers must regularly provide detailed information on investment types and volumes contained in the investment fund.

Governance: The investment fund must establish provisions governing the determination of investment guidelines, the allocation of competences, the calculation of units and the purchase and redemption of units, so that the interests of the pension funds involved are safeguarded in a transparent manner (for more details, see question below).

Segregation in Bankruptcy: The pension fund can only invest in investment funds if, in case of bankruptcy, assets can be segregated in favour of investors.

Quantitative Restrictions: The direct investments held by any fund in which the pension fund invests must be factored into the assessment of compliance with quantitative investment limits. Additionally, if a pension fund allocates 5% or more of its total assets to a single fund, that fund’s underlying investments must demonstrate adequate diversification.

Leverage: OPP 2 sets out a general rule prohibiting leverage, which also applies to indirect investments through investment funds. Exceptions to this rule allow leverage for (i) alternative investments, (ii) individual real estate holdings, (iii) certain regulated real estate funds, (iv) derivative investments, provided that the overall assets of the pension fund are not leveraged, and (v) infrastructure investments as well as certain private equity and private debt investments, if they are short-term bridge financing covered by capital commitments from investors or short-term, technically necessary borrowing.

Supplementary Payment Obligations: As a general rule, investments containing a supplementary payment liability, including investments in investments funds, are not permitted. A predetermined investment amount that can be called upon over a defined period of time (an open capital commitment) is not considered a supplementary payment obligation.

What governance requirements must non-Swiss investment funds meet to be eligible for investment by Swiss pension funds?

As mentioned above, OPP 2 sets out certain requirements that organisation of investment funds need to meet so that pension funds are permitted to invest in such funds.

The investment guidelines must clearly show how the pooled assets are invested, excluding any potential unclarities.

Further, the organisation of the investment fund needs to guarantee fair and efficient pooling, meaning that the rules need to contain – with respect to allocation of competences – inter alia the necessary separation of functions, the procedure in the event of a change in the investment guidelines, the allocation of costs according to the costs-by-cause principle, and the designation of the auditor.

To guarantee determination of correct market value of units, transparent accounting and efficient management reporting are required in order to assess the structure, success and risks of investments made.

There also needs to be some flexibility, in terms of purchase and redemption of investment fund units, given the ongoing liquidity requirements for pension funds.

Can Swiss pension funds invest in non-Swiss Infrastructure funds?

Yes, Swiss pension funds are permitted to invest in non-Swiss infrastructure funds, provided they comply with the general investment rules and the specific rules applicable to investments via investment funds.

Additionally, it is essential to thoroughly evaluate whether a given investment qualifies as an infrastructure investment under OPP 2 regulations. In practice, this question arises frequently. Non-Swiss sponsors of infrastructure funds intending to market to Swiss pension funds are well advised to engage legal counsel early in the structuring process to ensure compliance and avoid potential pitfalls.

Typically, infrastructure investments encompass “real assets” such as highways, airports, bridges or energy infrastructure facilities. These investments constitute a distinct asset class governed by specific regulations, including a separate category limit of 10% of total assets. Due to the look-through approach, this limitation also applies at the fund level for indirect investments via investment funds.

It is crucial to assess carefully whether an investment should be classified as (i) infrastructure or (ii) alternative investment, as alternative investments are subject to their own category limit of 15% of total assets.

For the purposes of OPP 2, infrastructure investments that employ leverage are considered alternative investments. Accordingly, if leverage is used in connection with an infrastructure investment and none of the exemptions below apply, the investment will be treated as an alternative investment.

The use of debt capital at the level of an infrastructure company does not constitute leverage within the meaning of OPP 2. If participations in such a company/project are leveraged, e.g. at fund or fund of fund level, this would be considered leverage. However, this is only the case, if with such debt financing at the level of funds or target funds a higher return is sought (so-called systematic leverage).

Short-term debt financing is not classified as systematic leverage. Such financing refers to arrangements with a term of up to six months, or up to twelve months when specific justification is provided. This applies in particular to debt financings with the purpose of general operational liquidity management, capital calls or credit lines for fund subscriptions and redemptions, and hedging transactions.

In any case, debt financing must be covered by contractual capital commitments. The deciding factor in determining whether a concrete case constitutes systematic leverage is not the mere legal admissibility of the use of debt according to the fund documentation, but the actual use of the debt.

Can Swiss Pension Funds invest in non-Swiss Alternative Investment Funds?

Yes, Swiss pension funds are permitted to invest in non-Swiss alternative investment funds, provided they comply with the general investment rules and the specific rules applicable to indirect investments via investment funds.

For purposes of OPP 2, alternative investments are non-traditional asset classes, such as receivables without a nominal amount, securitised receivables and senior secured loans.

Pension funds can only invest in diversified alternative investment funds. Leverage is permitted. A 15% quantitative limit applies to investments, including direct investments contained in alternative investment funds held by pension funds.

Summary table: Requirements for Non-Swiss fund sponsors targeting Swiss pension funds

Do you have any questions? Please do not hesitate to contact us, and make sure to also consult Volume 1 of this article: "Marketing to Swiss pension funds".