CSRD: revision of NFRD

The CSRD revises the sections of the Accounting Directive (Directive 2013/34/EU) relating to non-financial disclosures that were introduced by the Non-Financial Reporting Directive (NFRD). After the implementation of the NFRD into national legislation, large public interest entities in the member states were required to include a non-financial statement in their management reports. The non-financial statement was to provide transparency on policies related to, inter alia, environmental, social, and personnel matters, as well as companies’ efforts to respect human rights to combat corruption and bribery, and the impact of these issues on their business operations.

The NFRD’s requirements for mandatory sustainability reporting represented a significant milestone in the field of corporate sustainability reporting. Nevertheless, the European Commission adopted a proposal in April 2021 to revise the NFRD as part of the Sustainable Finance Package under the Green Deal. To ensure a consistent and transparent approach to sustainability reporting across the European Union and to expand the scope of the NFRD and its requirements, the European Commission has adopted the CSRD

Goals of CSRD

The CSRD came into effect on 5 January 2023 as Directive (EU) 2022/2464. It must be implemented into national law within one and a half years and thus become part of the member states laws. A significant goal of the CSRD is to ensure that investors are fully informed about the sustainability of their investments, similar to one of the Sustainable Finance Disclosure Regulation goals. Furthermore, the CSRD aims to improve the quality and comparability of sustainability information, to increase transparency and accountability and, to align sustainability reporting with the EU's sustainable finance agenda.

Content of CSRD

Some of the significant changes brought about by the CSRD include:

- A significant extension of the scope of the (sustainability) reporting requirements.

- Expanding and clarifying the content of sustainability reporting.

- Introduction of a standardised reporting framework that is obligatory across the EU.

- Introduction of a limited assurance statement on the sustainability report from a statutory auditor or other independent provider of assurance services.

- Requiring the information to be prepared and available digitally in XHTML format.

The CSRD requires the inclusion of a sustainability report in the management report. This sustainability report must be included in a distinct section of the management report and clearly identified as such. The information provided in that section must cover the sustainability impacts from two perspectives, - known as the double materiality perspective. The CSRD mandates companies to report both on the effects of their operations on the environment and society, as well as on how sustainability issues impact their business. As such, the risks and impacts of the company are each considered a materiality perspective. In addition, the reporting is not limited solely to the sustainability of the company itself, but also includes the sustainability in the value chain which the company is part of.

All companies falling within the scope of the CSRD will be required to report on a broad collection of ESG topics. This includes, inter alia, providing information on policies related to ensuring equal opportunities for employees, climate protection, working conditions, human rights, business ethics and corporate culture. Regarding the reporting framework for these topics, the European Financial Reporting Advisory Group (EFRAG) has been tasked with proposing a uniform set of reporting standards known as the European Sustainability Reporting Standards (ESRSs). A first set of draft ESRSs as prepared by EFRAG and providing for certain topical standards are currently being considered by the European Commission. Once the first set of ESRSs are finalised, EFRAG will (further) develop a second set which would contain sector-specific standards.

Scope of CSRD

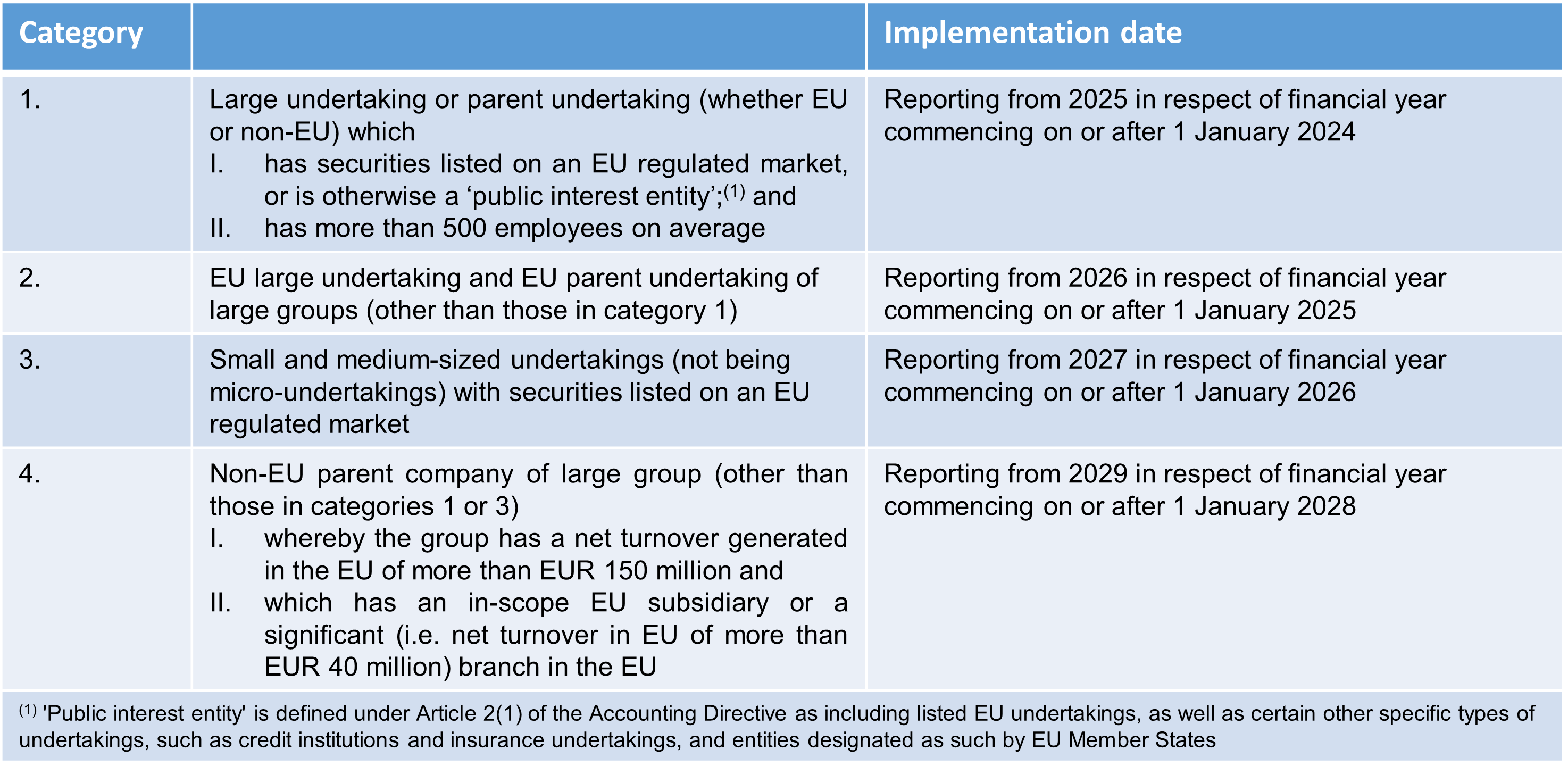

The reporting requirements introduced by the CSRD will be phased in from 2024 to 2028 along for the following categories of companies:

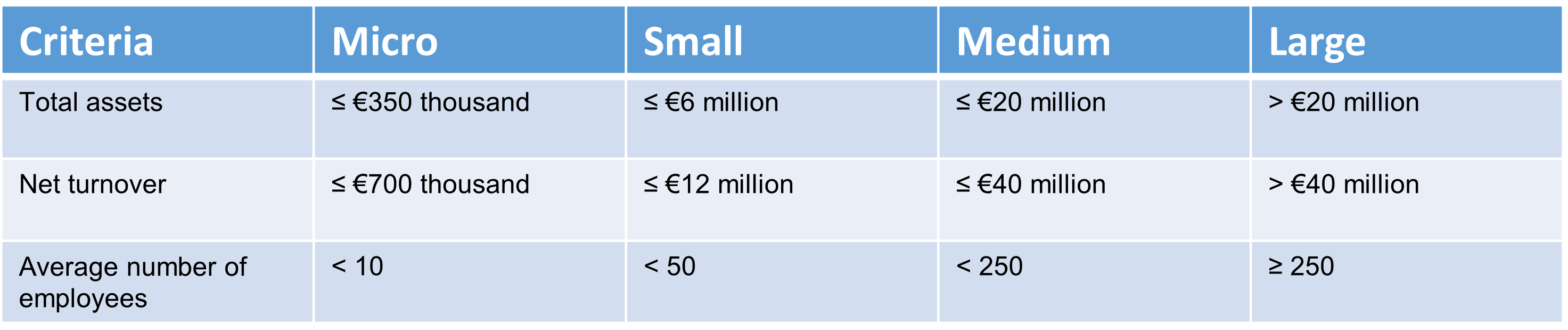

In determining whether an undertaking is ‘large’, ‘medium’, ‘small’ or ‘micro’, the following criteria under the Accounting Directive apply:

Even when not directly in scope, many companies will also be indirectly affected by the CSRD as they will have to provide various information to those CSRD-compliant companies as a subsidiary, supplier or customer.

Effects on the real estate industry

The CSRD will have significant effects on the real estate industry and real estate actors. As a sector that heavily impacts the environment and society, the CSRD will require real estate companies that fall within its scope to report on a range of ESG issues, such as energy efficiency, carbon emissions, social responsibility, diversity and inclusion. Real estate actors, such as real estate investment trusts (REITs) and developers, will have to disclose their ESG policies, targets, and performance, and provide assurance on their sustainability reports. The CSRD will no doubt increase transparency and comparability of sustainability information across the real estate industry, allowing investors, regulators, and other stakeholders to assess the sustainability risks and opportunities of different companies and assets. It may however, also pose significant compliance and reporting challenges.

Other blogs in this series

- ESG – Key criteria impacting taxonomy-alignment of real estate

- ESG - How does the SFDR impact the real estate sector?

- ESG - How does the EU Taxonomy Regulation impact the real estate sector?

- ESG - Green and sustainability-linked loans in the real estate sector

In these blogs, ESG experts from the Loyens & Loeff Real Estate and Corporate M&A practice group regularly share insights and reflect on ESG topics from a real estate perspective. Together with the ESG focus group with specialists from across our different practice groups and home markets, we combine ESG expertise, project and transactional advice, transaction and litigation experience to enable your success. For more information, please contact one of the members of our Real Estate practice group below.